The Russians are back buying luxury properties in central London and beyond. Favourable exchange rates and a rise in the price of oil mean that international buyers, particularly those from the Middle East and Russia, are spending millions on large homes in high-end neighbourhoods.

Camilla Dell, the managing partner at Black Brick Property Solutions, says her buying agency has had a 22 per cent increase in the number of Russians buying in central London this year compared with last. This includes a family who bought a large detached house in the heart of Kensington for £37 million and another who bought an apartment in a Mayfair development for £21 million. “The Russians have been our biggest spenders, paying an average of £18.5 million for their properties. They have been buying homes in prime central London, with a preference for Mayfair and Kensington. Their reasons for buying are relocating to London for family, better quality of life, safety and education. Brexit has not been a factor, although currency has,” Dell says.

The main nationalities buying in prime central London last year, according to the Mayfair-based agency, were British, Indian and Middle Eastern. This year the balance has shifted to Russian, French and Middle Eastern. Dell’s biggest sale this year was a £55 million house in Belgravia to a Saudi Arabian family. Savills also reports that super-prime sales, properties worth more than £10 million, are robust.

The estate agency reports there were 120 sales last year of properties in London worth more than £10 million.

While transactions were down a little on the previous year, slightly more was spent. In total about £2.5 billion of property worth more than £10 million sold last year, of which £1.5 billion was invested in properties worth more than £20 million, according to a report, Spotlight: Prime London & Country 2017, by Savills.

The agency also reports an increase in high-end sales in the home counties. There were four sales of more than £10 million in St George’s Hill in Surrey. High-spending buyers came from Europe, the Middle East, the Far East and Russia.

According to data from Hamptons International, the strengthening of the rouble against the pound means that property is 45 per cent cheaper than it was in January 2016 for Russian buyers. It also shows that international buyers accounted for one third of sales in London in the first three months of this year, up from 22 per cent in the last three months of last year, with the proportion of overseas buyers in the most expensive London neighbourhoods totalling 49 per cent. However, this is well below the peak of 60 per cent, achieved right after the European referendum when the pound was weak.

The proportion of EU buyers in prime central London has fallen from 33 per cent last spring to 8 per cent at the start of this year. It is the first time that European buyers are not the largest group of overseas buyers — overtaken by those from the Middle East, who accounted for 10 per cent of all purchases in prime central London. However, sales to European buyers in affluent London suburbs are rising; from 6 per cent at the end of last year to 10 per cent of all sales this year.

Johnny Morris, the research and analytics director for Countrywide, says: “Europeans are attracted to wealthy suburbs such as Wandsworth, Richmond and Wimbledon — driven by the exchange rate and market sentiment.”

The spike in international homeowners selling property in London, which occurred just after the Brexit vote — in London 46 per cent of sales were by foreign owners; in prime central areas the figure was 68 per cent — appears to have eased; now foreign owners selling accounts for 20 per cent of sales across the city, and 40 per cent in the centre. However, Morris says that a weak euro and Brexit uncertainty has contributed to an increase in sales by EU owners in prime central London.

Estate agents are investing in headsets, but not everyone is convinced.

Estate agencies are spending tens of thousands of pounds developing virtual-reality tours of high-end properties, so buyers can privately gaze at the interior of immaculate homes, including those yet to be built, in their own time.

JLL, the property consultant, is working with a virtual-reality company to offer virtual tours of properties for sale, or to let. It says the tours, available this spring, will be “fully immersive and as close to reality as possible”.

“The benefits include saving time,” Tim des Forges, a director at JLL, says. “Rather than the buyer being taken to see 20 flats, they can view them virtually and perhaps opt to see only their top three in person. Some may buy or rent only after seeing the virtual tour.”

The estate agency Carter Jonas is going one better. Using new technology, it has launched what it believes is the first virtual-reality tour to include an estate agent — viewers can follow an agent through a house, yet virtually look around and turn away from them. Carter Jonas says you would not let a buyer wander round your home without guidance, so why would you do so virtually?

The prototype is being used for a development in Leinster Square, in Notting Hill, west London, and is expected to be offered at two other central London developments, and one outside the capital. “The difference [with our technology] is that I’m in the video speaking,” says Amelia Blake, a London residential sales specialist at Carter Jonas.

Virtual-reality technology has been around for decades, but has not yet been good enough, nor cost-effective, for general use. Yet it has made big leaps in portraying spatial depth, which buyers can’t gauge from a floor plan or pictures.

Tours typically will be offered through an app downloaded on to a smartphone and viewed through a headset.

In Asia, however, tours are often viewed on tablets.

“Some clients do not want to put goggles on their head,” says Alex Newall, the managing director and founder of Hanover Private Office, a property consultancy.

The technology is often aimed at overseas investors. “In the prime central London market, international buyers are crucial to the business so we do what we can to accommodate their needs,” Blake says. Virtual reality has been vital for developers selling off-plan apartments, says Newall, and at a time when high-end property sales have slowed, estate agents might consider investment in virtual reality money well spent.

However, not all experts are convinced that virtual-reality viewings, however high-tech, are going to catch on for properties already built. “They are fun gimmicks, but anyone who is going to buy a house will visit it,” says Newall. “It doesn’t sell the house.”

He says that investment in drone photography has been more revolutionary for marketing properties.

Camilla Dell, the founder of Black Brick Property Solutions, an independent buying consultancy, says: “I have seen very little evidence of high-net-worth clients using this sort of technology. When people are spending millions, 99.9 per cent of the time they will get on a plane and see it, and we would be worried if they did not.” At best it may help clients to draw up a shortlist, but ultimately the virtual-reality experience cannot replicate being in a property and seeing the neighbourhood, and older buyers see it as a faff rather than helpful, Dell says.

Nonetheless, sellers yet to be convinced of the usefulness of virtual reality should perhaps keep the faith; it will provide them with useful analytics, including “how long buyers spend in each room, what they look at and what’s important to them,” says des Forges. “Sellers can take this information to maximise the potential of their property, and agents will be able to use it for future instructions, for example, by telling you that 60 per cent of virtual reality viewing was spent looking in the kitchen — so it’s good to place an emphasis on it.”

As property advisers, we are often asked what is the best kind of investment in London – a new build property or an older style or period property?

New build developments certainly have a natural appeal in that everything is brand new, which means buyers can put their own stamp on the property and maintenance should be low. People also like the concept of buying off plan, on the basis that prices will rise as the development nears completion. What’s more, off-plan developments often offer more flexible payment options.

When buying off plan, there are a number of things to be wary of. The biggest risk is that you can’t actually inspect the property. You need to be able to read the floor plan and visualise how the flat will look and what the outlook will be like, which can be challenging for the untrained eye. Swanky marketing suites can also often be very misleading.

You also need to take into account things like service charges, as many developers now calculate service charge on price per square foot basis, which can be confusing, and can significantly add to your annual expenditure, an important factor to consider particularly if you plan on renting the property out.

It is also important to consider the potential for capital growth. Many new builds can be priced as much as 30 per cent higher than surrounding re-sale properties, and as a buyer, you need to ask yourself whether that premium is justified. Looking back over the boom and bust periods of London’s property market, it is the older, period style properties which have tended to appreciate most over time.

New builds usually appreciate far slower, especially as they are often located in ‘up and coming’ areas, where supply outstrips demand. When the market drops, these developments tend to take a much bigger hit due to a combination of location and the fact that there is a higher density of similar properties in the area, with prices falling up to 20 per cent in some cases.

We recommend taking into consideration the location, as well as the “rarity” factor of the building. For example, we have purchased several apartments in the former BBC Television Centre development in White City for clients. This is a particularly interesting new development thanks in part to its history, its proximity to transport links, as well as Westfield shopping centre.

Clients of ours who bought into the scheme in early 2015 have already seen a 10 per cent uplift in the value, and we are encouraged by the fact that there is very little evidence of buyers trying to sell on their contracts before completion.

Another consideration when buying new is that there are deals to be had. Developers with completing stock are more able to play with their margins and are able to give ‘deals’ to their buyers. Buyers should be wary of developer incentives, such as offering to pay stamp duty, though – the cost is often made up in the asking price of these so-called “incentives”.

When weighing up the options, the key to buying new build property is to do your homework; seek impartial advice on the developer, the area – check the local council’s housing policy for further developments – and the property itself.

A dedicated space for doing hair, nails and make-up is becoming a must-have in high-end homes

Donald and Melania Trump have been handed the keys to the White House. This means that, in keeping with tradition, the Trumps are allowed to make changes to the property to meet their family’s needs.

While Michelle Obama spent her early days as first lady focusing on cultivating the vegetable garden so her family could eat fresh vegetables, this week we discovered that Melania’s priority is to add a “glam room”.

“There will absolutely be a room designated for hair, make-up and wardrobe,” says her make-up artist, Nicole Bryl, reassuring those who were worried there wasn’t going to be.

It is in this room that Bryl will toil for the 75 minutes of “uninterrupted focus” it takes to do the first lady’s make-up each time. “Melania wants a room with the perfect lighting scenario, which will make our jobs as a creative team that much more efficient,” Bryl adds.

Yet Mrs Trump is not the only woman who takes her beauty routine so seriously that it warrants its own room. Glam rooms are a feature in the most expensive homes in this country — and may become more popular among women who hope to copy Melania’s über-groomed approach to life.

So what is a glam room? It’s a glorified dressing room — a room with good lighting and space for a hairdresser and make-up artist to work their magic, possibly with a hair-washing station. Above all, it is somewhere with eye-wateringly expensive shelving, with compartments for belts, rings, watches and handbags. One central London glam room even features a cosmetics fridge designed to keep the owner’s make-up at the optimum temperature.

Camilla Dell, a buying agent, reports that she has viewed homes with not only glam rooms, but glam suites, where a separate lounge area containing a minibar and TV is located off a dressing room, so “all the girls can discuss and debate outfits”, Dell says.

Carrie Bradshaw would approve; Emmeline Pankhurst, not so much. Penny Mosgrove, the chief executive of Quintessentially Estates, a company that sells houses starting at £3 million and rising to £20 million, says that among her clients glam rooms are a must-have. If one doesn’t exist, some wealthy buyers will sacrifice a bedroom to create one.

The estate agent Charlie Gibson, who works in the Mayfair office of Carter Jonas, reports that he has also seen properties with a male equivalent, called grooming rooms. “I have seen a barber shop set-up within a very expensive property, where the Mayfair barber Geo F Trumper visits for a grooming appointment,” Gibson says.

It is common for the incoming president and the first lady to redecorate parts of the 132-room political mansion. The Obamas filled the property with contemporary art and replaced a bust of Churchill with that of Martin Luther King; Laura Bush faithfully restored the Green Room, used for small receptions and teas.

As with the presidential campaign, the Trumps may do things differently. Based on the interiors in the family’s New York home, the glam room — possibly like the rest of the house — will feature a 1980s aesthetic, with lots of gold, ostentatious chandeliers and pictures of Donald Trump in manly poses.

The interior designer Mhairi Coyle says: “It is like the interior design you see in casinos: the more detail, the more pattern, the more colour you can put in the place, the better. With a personality like Donald Trump’s, he’d want everything over the top.

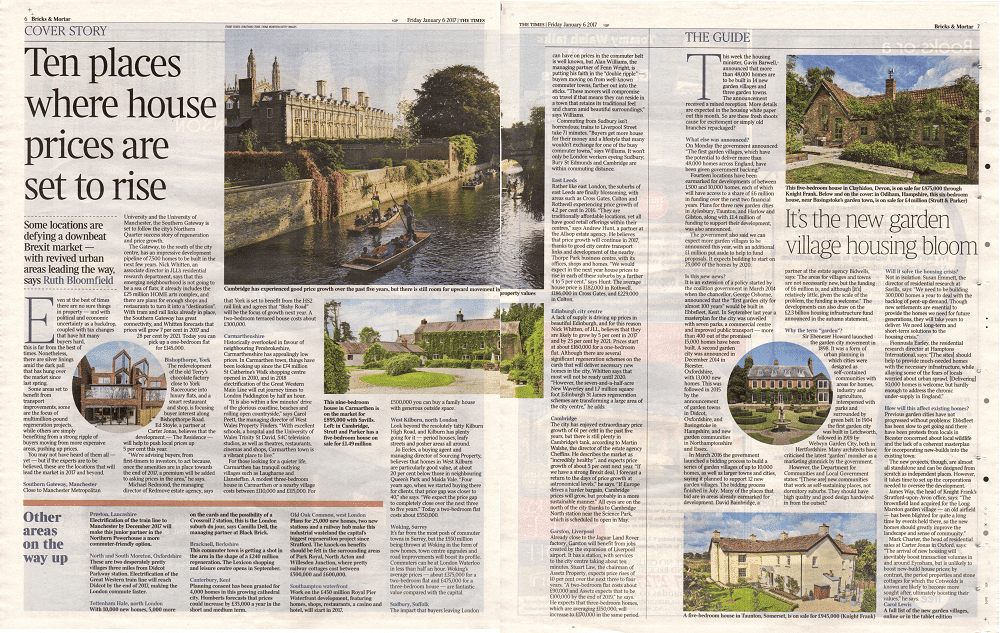

Some locations are defying a downbeat Brexit market — with revived urban areas leading the way even at the best of times there are no sure things in property — and with political and economic uncertainty as a backdrop, coupled with tax changes that have hit many buyers hard, this is far from the best of times. Nonetheless, there are silver linings amid the dark pall that has hung over the market since last spring.

Some areas set to benefit from transport improvements, some are the focus of multimillion-pound regeneration projects, while others are simply benefiting from a strong ripple of buyers moving from more expensive areas, pushing up prices.

You may not have heard of them all — yet — but if the experts are to be believed, these are the locations that will lead the market in 2017 and beyond.

Southern Gateway, Manchester

Close to Manchester Metropolitan University and the University of Manchester, the Southern Gateway is set to follow the city’s Northern Quarter success story of regeneration and price growth.

The Gateway, to the south of the city centre, has an impressive development pipeline of 7,500 homes to be built in the next few years. Nick Whitten, an associate director in JLL’s residential research department, says that this emerging neighbourhood is not going to be a sea of flats; it already includes the £25 million HOME arts complex, and there are plans for enough shops and restaurants to turn it into a “destination”. With tram and rail links already in place, the Southern Gateway has great connectivity, and Whitten forecasts that prices will grow 7 per cent in 2017 and 28 per cent by 2021. Today you can pick up a one-bedroom flat for £145,000.

Bishopthorpe, York

The redevelopment of the old Terry’s chocolate factory close to York Racecourse into luxury flats, and a smart restaurant and shop, is focusing buyer interest along Bishopthorpe Road.

Ed Stoyle, a partner at Carter Jonas, believes that the development — The Residence — will help to push local prices up 5 per cent this year.

“We’re advising buyers, from first-timers to investors, to act because, once the amenities are in place towards the end of 2017, a premium will be added to asking prices in the area,” he says.

Michael Redmond, the managing director of Redmove estate agency, says that York is set to benefit from the HS2 rail link and agrees that “Bishy Road” will be the focus of growth next year. A two-bedroom terraced house costs about £300,000.

Carmarthenshire

Historically overlooked in favour of neighbouring Pembrokeshire, Carmarthenshire has appealingly low prices. In Carmarthen town, things have been looking up since the £74 million St Catherine’s Walk shopping centre opened in 2010, and in 2018 electrification of the Great Western Main Line will cut journey times to London Paddington by half an hour.

“It is also within a few minutes’ drive of the glorious coastline, beaches and rolling open countryside,” says Carol Peett, the managing director of West Wales Property Finders. “With excellent schools, a hospital and the University of Wales Trinity St David, S4C television studios, as well as theatres, restaurants, cinemas and shops, Carmarthen town is a vibrant place to live.”

For those looking for a quieter life, Carmarthen has tranquil outlying villages such as Laugharne and Llansteffan. A modest three-bedroom house in Carmarthen or a nearby village costs between £110,000 and £115,000. For £500,000 you can buy a family house with generous outside space.

West Kilburn, north London

Look beyond the resolutely tatty Kilburn High Road, and Kilburn has plenty going for it — period houses, leafy streets and posher areas all around.

Jo Eccles, a buying agent and managing director of Sourcing Property, believes that homes in West Kilburn are particularly good value, at about 20 per cent below those in neighbouring Queen’s Park and Maida Vale. “Four years ago, when we started buying there for clients, that price gap was closer to 40,” she says. “We expect the price gap to completely close over the next three to five years.” Today a two-bedroom flat costs about £550,000.

Woking, Surrey

It’s far from the most posh of commuter towns in Surrey, but the £550 million being thrown at Woking in the form of new homes, town centre upgrades and road improvements will boost its profile. Commuters can be at London Waterloo in less than half an hour. Woking’s average prices — about £375,000 for a two-bedroom flat and £475,000 for a three-bedroom house — are fantastic value compared with the capital.

Sudbury, Suffolk

The impact that buyers leaving London can have on prices in the commuter belt is well known, but Alan Williams, the managing partner of Fenn Wright, is putting his faith in the “double ripple” — buyers moving on from well-known commuter towns, farther out into the sticks. “These movers will compromise on travel if that means they can reside in a town that retains its traditional feel and charm amid beautiful surroundings,” says Williams.

Commuting from Sudbury isn’t horrendous; trains to Liverpool Street take 71 minutes. “Buyers get more house for their money and a lifestyle that many wouldn’t exchange for one of the busy commuter towns,” says Williams. It won’t only be London workers eyeing Sudbury; Bury St Edmunds and Cambridge are within commuting distance.

East Leeds

Rather like east London, the suburbs of east Leeds are finally blossoming, with areas such as Cross Gates, Colton and Rothwell experiencing price growth of 4.2 per cent in 2016. “They are traditionally affordable locations, yet all have good retail offerings within their centres,” says Andrew Hunt, a partner at the Allsop estate agency. He believes that price growth will continue in 2017, thanks to good city centre transport links and development of the nearby Thorpe Park business centre, with its offices, shops and homes. “We would expect in the next year house prices to rise in each of these suburbs by a further 4 to 5 per cent,” says Hunt. The average house price is £182,000 in Rothwell, £186,000 in Cross Gates, and £229,000 in Colton.

Edinburgh city centre

A lack of supply is driving up prices in beautiful Edinburgh, and for this reason Nick Whitten, of JLL, believes that they are likely to grow by 5 per cent in 2017 and by 23 per cent by 2021. Prices start at about £160,000 for a one-bedroom flat. Although there are several significant regeneration schemes on the cards that will deliver necessary new homes in the city, Whitten says that most will not be ready until 2020. “However, the seven-and-a-half-acre New Waverley and 1.7 million square foot Edinburgh St James regeneration schemes are transforming a large area of the city centre,” he adds.

Cambridge

The city has enjoyed extraordinary price growth of 61 per cent in the past five years, but there is still plenty in Cambridge’s tank, according to Martin Walshe, the director of the estate agency Cheffins. He describes the market as “incredibly healthy”, and expects price growth of about 5 per cent next year. “If we have a strong Brexit deal, I forecast a return to the days of price growth at astronomical levels,” he says. “If Europe drives a harder bargain, Cambridge prices will grow, but probably in a more sustainable manner.” All eyes are on the north of the city thanks to Cambridge North station near the Science Park, which is scheduled to open in May.

Garston, Liverpool

Already close to the Jaguar Land Rover factory, Garston will benefit from jobs created by the expansion of Liverpool airport. It has a station, with services to the city centre taking about ten minutes. Stuart Law, the chairman of Assetz Property, expects price rises of 10 per cent over the next three to four years. “A two-bedroom flat costs about £90,000 and Assetz expects that to be £100,000 by the end of 2019,” he says. He expects that three-bedroom homes, which are averaging £150,000, will increase to £170,000 in the same period.

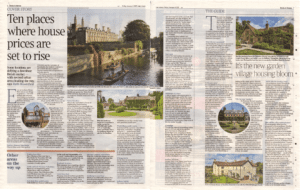

Other areas on the way up

Preston, Lancashire

Electrification of the train line to Manchester by December 2017 will make this junior partner in the Northern Powerhouse a more commuter-friendly option.

North and South Moreton, Oxfordshire

These are two desperately pretty villages three miles from Didcot Parkway station. Electrification of the Great Western train line will reach Didcot by the end of 2017, making the London commute faster.

Tottenham Hale, north London

With 10,000 new homes, 5,000 more on the cards and the possibility of a Crossrail 2 station, this is the London suburb du jour, says Camilla Dell, the managing partner at Black Brick.

Bracknell, Berkshire

This commuter town is getting a shot in the arm in the shape of a £240 million regeneration. The Lexicon shopping and leisure centre opens in September.

Canterbury, Kent

Planning consent has been granted for 4,000 homes in this growing cathedral city. Humberts forecasts that prices could increase by £35,000 a year in the short and medium term.

Old Oak Common, west London

Plans for 25,000 new homes, two new stations and a railway hub make this industrial wasteland the capital’s biggest regeneration project since Stratford. The knock-on benefits should be felt in the surrounding areas of Park Royal, North Acton and Willesden Junction, where pretty railway cottages cost between £500,000 and £600,000.

Southampton waterfront

Work on the £450 million Royal Pier Waterfront development, featuring homes, shops, restaurants, a casino and hotel, will start in 2017.

We look at the surprisingly prosaic features that add the most value to a house in a village or in the city

How much is your home worth? It’s not a simple question to answer. If you go on Zoopla or Rightmove, you will get one figure based on asking prices. Invite an estate agent round and they will give you another based on the deals they have in the pipeline. Pay for a surveyor, who will be looking for comparable properties that have sold, and it is likely that you’ll get a different value again.

Valuing a home is tricky. Finding out the average price per square foot for the area and multiplying that number by the size of your home might seem like a good way to get an exact answer — only the value of a home isn’t dictated by size alone. It is also affected by individuals, their motivations and the property itself: how badly does a vendor want to sell? What condition is the property in? How long has it been on the market? What makes a person desperate to buy one home and not another?

In recognition of this, Savills has surveyed its agents and asked them which features add value and which don’t. If you think that a home packed with original features in London will sell for more than one without, for example, you might be surprised to find out the facts.

Off-street parking ■ Value added in a £1.25 million London home 3-7 per cent ■ Value added in a £750,000 regional home 0-6 per cent In London, off-street parking is a big advantage. It saves you the stress of trying to reverse a Volvo into a space that is really fit only for a Mini. In a village outside the capital it is considered essential, according to Tom Orford, the director of the Ipswich branch of Savills. Without parking, the value of a home could be reduced by as much as 25 to 30 per cent, he says.

South/southwest-facing garden ■ Value added in a £1.25 million London home 1-4 per cent ■ Value added in a £750,000 regional home 2-5 per cent Although a south or southwest-facing garden is a preference, it won’t always swing a sale because the majority of gardens still get sunshine in the summer no matter what their orientation. The consensus among agents is that while a south-facing garden does improve the saleability of a home — the extra light it brings makes the home more inviting — it doesn’t particularly bump up the price. Garden size is much more likely to add a premium — anything over 60ft is especially prized.

That said, a big garden isn’t always desirable: the buying agent Nicholas Ayre reports that clients of his were recently put off buying a home in London because it had a 100ft garden and they were worried about maintaining it.

A good view ■ Value added in a £1.25 million London home up to 10 per cent ■ Value added in a £750,000 regional home 5-9 per cent Up to 10 per cent seems conservative if anything — agents often put the value of a river view at up to 20 per cent. Robin Chatwin, the head of Savills southwest London, says that for some retirees who are downsizing, a good view can make up for living in a smaller home.

In Cambridge, Ed Meyer, also from Savills, adds that “people don’t necessarily have it on their wish list, but it can be a deal-clincher”.

Low EPC rating/energy efficiency ■ Value added in a £1.25 million London home 0-2 per cent ■ Value added in a £750,000 regional home 0 per cent A report published by the Department of Energy & Climate Change in 2013 stated that nearly 93 per cent of homes sold are in EPC bands C, D and E, with 45.5 per cent in band D. This means that almost all homes have a poor EPC rating. This could explain why, despite our concerns about climate change, a low EPC rating still doesn’t seem to matter. “Have I ever had a client pull a deal because of the EPC rating? No, never. People never look at them,” says Ayre.

Historical or architectural significance ■ Value added in a £1.25 million London home 0-5 per cent ■ Value added in a £750,000 regional home 0-4 per cent “We don’t come across blue plaques very often — they are still pretty rare,” says Caspar Harvard-Walls, a partner at Black Brick. “It’s something that will assist in getting viewings but not necessarily add value unless it’s someone very famous. In terms of architectural significance, the Barbican, in the City of London, has an incredible following from people who like that brutalist architecture. The Barbican has its own market — there is nothing like it — and as a result achieves values in excess of the local market.”

An annexe (secondary accommodation) ■ Value added in a £1.25 million London home 5-10 per cent ■ Value added in a £750,000 regional home 10-25 per cent Increasingly, buyers are looking to live with two or three generations in the same house, or are looking for an investment. As a result, secondary accommodation is creeping up buyers’ wish lists. This is popular with people who work from home, people who want a granny flat and people who are looking to rent out the accommodation. “We have found that more and more buyers are looking for secondary accommodation,” says Orford. “Our last three buyers wanted this.”

Original period features ■ Value added in a £1.25 million London home 1 per cent or less ■ Value added in a £750,000 regional home 5-15 per cent The reason for the low London figure is that while original features are sought after in period property, buyers are aware that they can easily restore period features at a small cost and are no longer willing to pay a premium for them.

Not everyone shares this viewpoint. “When features are gone, sometimes these properties lack character. They become bland white boxes and it doesn’t help them to sell,” says Harvard-Walls.

Technology and gadgets ■ Value added in a £1.25 million London home 2-8 per cent ■ Value added in a £750,000 regional home 5-10 per cent Good technology and a Miele or Gaggenau appliance suggests that a homeowner has invested in a good boiler too. It reassures buyers of a level of maintenance, which explains why this is one of the features that adds significant value in and outside London.

“Lots of technology can be a bad thing if you are an investor,” says Ayre. “It will mean endless calls from your tenant saying: ‘I can’t get the blinds to go up.’ “

Planning ready ■ Value added in a £1.25 million London home up to 4 per cent ■ Value added in a £750,000 regional home 1 per cent or less “Increasingly, we are seeing buyers preparing their properties with planning in place,” says Jo-Anne Neighbour, of the Islington office of Savills. “Often they will submit a planning application, which does not cost a lot, and look to sell for an added premium.”

Outside London, particularly in more rural locations, space is usually not an issue. Planning permission for barn conversions does not usually add a premium.

There is no mistaking South Kensington for any other part of prime central London. Where else has so many museums, so many wide, leafy streets and so much French chatter coming from the children on their way to and from school? Right now, however, it shares one overriding similarity with its neighbours — a depressed housing market.

Transactions in 2015 across all price ranges in South Kensington — an area of London famed for its French buyers — were down 17.4 per cent compared with the previous year, according to property data company LonRes. The number of £5m-plus sales in the area dropped 45 per cent over the same period.

It is the same story as in the rest of prime central London. Higher stamp duty on homes priced above £937,500 coupled with economic jitters over oil price falls and slowing economic growth in China have undermined confidence and, with it, the number of transactions.

That malaise has hit prices. Knight Frank says the SW7 postcode has seen prices drop 3.3 per cent in the year to January 2016, making it the worst performing central London location aside from Knightsbridge. The buying agency Black Brick, for example, has just negotiated the purchase of a South Kensington flat for £545,000 below asking price — a 15 per cent reduction.

If that sounds like a bargain, don’t feel too sorry for local owners: they have done rather better over the longer term. Not only have they seen substantial capital appreciation — 45 per cent over the past five years and a remarkable 155 per cent since 2006, says LonRes — but they also enjoy what some describe as the prettiest parts of central London.

Estate agents regard Onslow Square and Onslow Gardens as the most desirable addresses in South Kensington, with their white-stucco period buildings and attractive gardens. Nearby Tregunter Road, The Boltons, The Little Boltons, Pelham Crescent, Rose Square and Harley Gardens are also popular. A few houses are split into flats but most remain family homes overlooking pretty squares.

“South Kensington has a very European feel, complete with a French lycée, good restaurants, the French market and European-inspired architecture,” says property consultant Charles McDowell — who specialises in buying and selling £5m-plus homes in the area.

French buyers remain a significant group, he says, despite the opening of French schools in less expensive areas such as Battersea and Wembley. “Since 2010, there’s been an increase of 40 per cent in the number of French moving to SW7 and it’s going up,” says Amy Rogers of the Carter Jonas estate agency.

Other agents say Italians and Greeks are buying too, adding to the area’s European feel. “It typically attracts fewer Middle Eastern or Russian buyers who prefer modern apartments and houses found in Belgravia,” says Charlie Bubear of Savills.

In fact, the lack of new, premium-priced pads is cited by some local agents as the reason prices have fallen more in South Kensington than in most neighbouring areas.

The dominance of renovated period properties has advantages, though. “South Kensington can offer substantial lateral space not often found in other prime central London districts. Large family-friendly flats offer a natural alternative to traditional Chelsea town houses arranged over five or six floors,” says Simon Rose of Strutt & Parker.

With demand sluggish, there is no shortage of stock. Savills is selling a recently refurbished, three-bedroom apartment in Onslow Gardens for £4.95m. It has 2,214 sq ft of internal space set within a grade II-listed period house. A four-bedroom house — small by the area’s standards at 3,100 sq ft — on Clareville Street is on sale for £6.5m through Lurot Brand estate agents.

At nearby Queen’s Gate, Knight Frank is selling a four-bedroom, 3,000 sq ft apartment for £6.5m, while on Hereford Square, a short walk from Gloucester Road Tube station, a six-bedroom family house is available through Aylesford International for £12m.

Soon on the doorstep of these period properties will be one of London’s biggest residential new-build quarters — and it might just help revive the flagging property market. “Earls Court’s regeneration, just 10 minutes’ walk from South Kensington, will have a huge impact,” says Robin Paterson of Sotheby’s International Realty. “At 80 acres it will be the same size as Soho.”

Rather than tempt buyers away from South Kensington, Paterson says the new district’s high-end retail and restaurants will bolster the area’s appeal. “South Kensington will benefit from being close to a regeneration area,” he says. “And, [in turn], Earls Court will benefit from being so close to one of London’s most prestigious locations.”

Buying guide

South Kensington is home to the Victoria and Albert Museum, Science Museum and Natural History Museum

Average house prices near the Tube stations of South Kensington and Gloucester Road are £2.29m, according to online estate agency eMoov

In December 2015, the crime rate in the Courtfield ward, which covers much of South Kensington, was 9.53 per 1,000 residents, which is less than the borough average of 10.82 per 1,000 residents

What you can buy for . . .

£1m A one-bedroom, ground-floor flat with access to a communal garden

£5m A three-bedroom duplex apartment

£10m A semi-detached family house with four bedrooms

According to the old adage: “When the United States sneezes, the world economy catches a cold.” Recent events have taught us that it is not only American snuffles that can spread far and wide. The Chinese economy has stalled, its stock market has faltered and there is panicky talk of a global slowdown.

Several large commercial property deals that hinged on Chinese investment have fallen through, and in residential property markets there are rumours of several investors pulling out or rapidly flipping properties in redevelopment areas such as Nine Elms.

Aberdeen Asset Management recently stated: “Correlations between the London property market and flows of Asian investment are remarkably high, suggesting that if China’s economy keeps faltering, London property markets could be in for a tough time.”

Data from the estate agency Strutt and Parker on where the money for residential property investment in London orginates supports this view. Asian buyers of resale properties fell from 6.6 per cent of the agency’s sales at the end of 2014 to 4.9 per cent last year.

However, a closer look shows that all nationalities have backed off, including northern Europeans, who have fallen from 7.7 per cent in 2014 to 1.6 per cent in 2015, with the growth coming from British domestic (64.8 per cent of buyers in 2015) and expat buyers (8.2 per cent).

So it seems the speculation might be right and that Chinese money is flowing out of London. This month the luxury developer Banda said its search team had noticed that “the prime central London property market is undergoing a shift in the dynamic of overseas investors as Russian and Chinese buyers seemingly withdraw and Iranians and Europeans seek to invest”.

Louisa Brodie, the head of search and acquisitions at Banda, says: “Despite general scaremongering, we are seeing little evidence of a waning in London’s popularity among overseas property investors. It is still the No 1 destination globally, and where Russians and Chinese buyers are withdrawing as a result of external forces, other investors are quickly plugging the gap.

“Many wealthy Iranian families have strong connections with London, so it feels familiar to them. There are concerns that the recent lifting of UN sanctions could be reversed, so we are likely to see people looking to move their money out [of Iran] fairly quickly.”

Dominic Grace, the head of London residential development at Savills, says: “The number of actual mainland Chinese who buy in London is very small — they still find it difficult to get their money out of China.”

He adds that Chinese purchasers tend to favour new-build properties. Savills figures show that last year 23 per cent of purchasers of new-build properties were from China or Pacific Asia (compared with 53 per cent from the UK); for resale properties in prime London it was 3 per cent (compared with 68 per cent from the UK).

The majority of Chinese money in London comes via Hong Kong and Singapore — countries that have, as Grace puts it “poured buckets of cold water over any froth in their own property markets”. This cold water is primarily in the form of punitive taxes. A Knight Frank study shows that, on a $1 million property, buyers would pay 22.4 per cent tax in Hong Kong and 19 per cent in Singapore, enticing investors to look elsewhere, including London, where, in 2015, they would pay 9.7 per cent in taxes. However, London isn’t the only strong property market catching their eyes. Closer to Asia is Australia, whose housing market has been showing strong capital growth (9.8 per cent last year, with house prices 48 per cent above its financial-crisis low), particularly in Melbourne and Perth, Grace says.

Camilla Dell, the managing partner at Black Brick, an independent property buying agency, predicted in September: “The falls in China’s stock market appear dramatic but it is worth bearing in mind that the country’s equity market is less closely linked to the underlying economy than is the case in most developed economies. Recent years have seen enormous wealth built up in China’s ‘real’ economy and that wealth will become an increasingly important factor in markets around the world in coming decades — including London’s property market.”

However, last week she admitted that she has yet to see “huge numbers of Chinese buyers come our way”.

Sungwei Huang, an agent with Felicity J Lord in Canary Wharf, says the Chinese haven’t lost their appetite for British property but that the government’s changes to capital gains tax and stamp duty, including the forthcoming 3 per cent levy on buy-to-let and second homes, have made buyers hesitant.

Huang is hopeful that measures to make it easier to get money out of China will help. The Qualified Domestic Individual Investor programme, which is set for trial in six Chinese cities, including Shanghai, will enable people with at least one million yuan in assets to buy shares in New York, London or Paris. This could lead to more Chinese money being invested in British property.

However, a similar scheme by the Bank of China was closed, less than a year after it started, because demand proved too high.

Huang says there are two distinct types of Chinese buyers in London: those who are looking at expensive high-end prime central London properties, and a much more active lower tier who are interested in buying two-bedroom apartments for between £450,000 and £650,000 as buy-to-let investments or to use while their children study here.

However, some commentators are already turning their attention away from China and towards the Middle East, where political unrest means that investors are searching for a safe haven.

Dell says: “There is plenty of appetite in Dubai, Jordan and Saudi Arabia, where there is political and economic uncertainty. It is perhaps too early to tell whether Iranian money will land in London; at the moment there are some issues with the banking system and getting money out is difficult, but Iran is definitely one to watch.”

Secret owners

There are about 4,000 owner-occupied homes in England and Wales held in corporate envelopes, according to data from the tax office. Corporate envelopes are where a property is bought under a company name rather than an individual’s name and are often associated with mansion-buying oligarchs seeking anonymity.

It was hoped that the introduction of the Annual Tax on Enveloped Dwelling in April 2013 would raise substantial amounts for the treasury.

Analysis of the latest data by London Central Portfolio (LCP), a residential fund and asset management company, shows that 3,990 properties (0.02 per cent of the UK’s total housing stock) were held in corporate envelopes nationwide in 2015.

The owners of these properties paid £116 million to the treasury last year. The majority of the tax was paid on properties in London (£103 million), while £11 million came from homes in southeast England and the remaining £2 million from properties elsewhere in the UK. “These statistics show that numbers are less than a fifth of previous estimates. While the official numbers will increase when the tax bands extend to lower-value properties [the tax applies to properties worth from £500,000 from April 2016], this is unlikely to be significant as such properties are not usually bought in corporate wrappers,” according to LCP.

Climbing the property ladder and moving into ever-bigger homes was once the path for those with a growing family, but now homeowners have a new mantra — renovate, don’t relocate.

Some simply can’t reach the next rung thanks to relentless house price rises, but for many it’s an active choice, and the case for staying put became even more compelling last year when stamp duty was reformed. This made anyone spending more than £938,000 on a home worse off, and left those buying a £2 million house facing a tax bill of £153,750. That buys a lot of home improvement, so it’s little wonder that the top of the market has cooled.

Someone who has chosen to invest in their existing house rather than give the taxman an early Christmas gift is Camilla Dell, of Black Brick Property Solutions, a London buying agent. Dell, who has been finding homes for well-heeled buyers since 2002, might have exploited her insider knowledge to find a bigger home, but instead she opted to stay put. Dell recently completed a renovation and found that it was a better option than buying another property, especially given the changes to the tax regime.

“When you take into account the costs of moving and the stamp duty, I paid less on the refurbishment than I would have done on the tax bill,” she says. “Also, I love where I live and I love the house. I wouldn’t have wanted to move even if money weren’t an issue.”

When Dell bought the Victorian terraced house in West Hampstead 12 years ago the property was divided into two parts. There was a lower ground two-bedroom flat, which was tenanted, and she lived in the upper section of the house. “I set my business up in the loft and then made the lower floors an office as it became more succesful and the tenants moved out,” she says. “That involved knocking down some walls and making it open plan. When the business expanded I rented an office in Mayfair and we converted the house back into one unit and added an extension. The lower ground floor became a dining room and kitchen leading into a sitting room with bifold doors out to the garden. One big family living space. It completely transformed the house and moving the kitchen meant we gained a formal reception room. I had my first daughter and we were very happy, but a year ago we decided to refurbish the house because it was looking very tired — and I had another baby on the way.” Dell hired an architecture company, dMFK, and the builders set to work.

The plan involved replacing the floors, staircase and bannisters, repainting the house, renovating the master bedroom and its bathroom, and replacing the sash windows to put in double glazing. Two bedrooms with lots of storage were created upstairs for the children, a new office was added, and their live-in nanny’s bedroom was moved so that she had her own space and bathroom.

Even though she knew that she wasn’t planning on moving, Dell couldn’t help thinking like a buying agent and remained conscious of future saleability. “Even if you’re not planning to sell immediately you’ve always got in the back of your mind not to do anything too garish. It’s best to keep things neutral — my clients are put off by bold colour schemes. I’ve seen deals fall through because of poor decor choices.”

She couldn’t resist some personal flourishes though. “My daughter loves dinosaurs so we put in silver and white dinosaur print wallpaper, and another with butterflies in the baby’s room,” she says. “It’s very cute.”

Dell rented a temporary home in her dream area and lived there while the house was renovated. “We took a flat in St John’s Wood,” she says. “I’ve always wanted to live there so I thought I’d rent and see what life was like. It was OK, but it was noisy. After six months we were dying to get back.” Having moved out in October last year they thought the work would take three or four months, but this turned into six. “We should perhaps have been better organised and started the work a bit earlier, but we’re very happy now. It’s a great home. Staying put was the right thing to do.”

It is undoubtedly a First World problem, up there with agonising over whether to plump for Waitrose or Marks & Spencer smoked salmon this Christmas, to go tall or grande with your decaf soy latte with caramel drizzle, or to tip the builders who have been using a portable loo in your front garden for six months while you are mid-extension. But there is a new property quandary, following last month’s revamp to stamp duty. Do you rush to buy that dream holiday cottage or pension-boosting buy-to-let before the tax rises on April 1, or wait to see if prices drop next spring in response to George Osborne’s latest property manoeuvre?

The announcement last month of an additional 3% rate on the purchase of any second home costing more than £40,000 is a measure designed to keep property values in check and make the market more accessible to first-time buyers. The 2011 census revealed that 1.57m people in England and Wales had an additional property that they used for 30 days or more each year. Yet, as with many government policies, there may be unintended consequences.

Estate agents and other property professionals are split in their predictions about how the housing market will respond. In one corner sit those who believe a stampede is on the way. “The changes could create a surge in demand, as landlords look to beat the implementation date,” says Rory O’Neill, head of residential at Carter Jonas estate agency. Camilla Dell, managing partner at the London buying agency Black Brick, agrees: “We’ve taken several new inquiries from buyers who want to crack on.”

Adrian Gill, director of the Reeds Rains and Your Move agencies, talks about “a scramble for second-home purchases” leading to higher prices during winter, when values typically take a dip. Savills estate agency’s head of residential research, Lucian Cook, also anticipates a rush to complete deals by the end of March — perhaps pushing prices up in the short term. From April, he says, demand for holiday homes may dip, “with a consequential impact on pricing”.

Yet is at this point, after the new tax comes into effect, that many agents and analysts suggest canny buyers should pounce. Anyone purchasing now will probably pay over the odds, they argue, even when you take the lower stamp duty into account. “This will adversely affect the holiday-home market in the short term, with demand falling after April next year, resulting in a downward pressure on prices,” says Miles Kevin, director of Chartsedge, a Devon estate agency specialising in second homes.

For those who do wait, one thing looks certain — it will be difficult to beat the 3% surcharge. Although buy-to-let purchasers can offset it against capital gains tax when they eventually sell, they must pay upfront. Owners letting out holiday homes may still enjoy some of the mortgage-interest tax breaks recently removed from buy-to-let landlords, but they will have to pay the extra 3% if their second home is in England, Wales and Northern Ireland.

Otherwise, it appears that the well-publicised trio of houseboats, caravans and Scottish homes — the last of which are subject to Scotland’s Land and Buildings Transaction Tax, with a £300,000 cottage, for example, attracting a £4,600 tax bill — are the only sales to be exempt from the new duty surcharge.

Buy-to-let has boomed in the past year, in part because those aged over 60 have been able to access their pension pots and release cash, much of which has been invested in property. One of the biggest specialist mortgage firms, Paragon Group, last month reported a 102% increase in the volume of lending, up from £656.6m in 2013-14 to £1.33bn in the year to September 2015.

How will the higher stamp duty affect this? The impact will be felt in different ways across the country. The biggest ripples will be in areas where there are substantial buy-to-let sectors, which have been highlighted by research compiled for The Sunday Times by Countrywide, Britain’s largest estate and letting agency.

“The new rates of duty will effectively increase the price investors pay, and hence reduce the yield they achieve,” says Fionnuala Earley, Countrywide’s chief economist. “New landlords must do their sums more carefully to make sure returns on their investment add up.”

In the year to October, Countrywide’s offices in the West Midlands sold 16.7% of their homes to buy-to-letters, the largest proportion of any region in England. Yet some individual hotspots, all outside that region — Guildford, in Surrey, for example, and Doncaster, in South Yorkshire — saw much larger shares of their sale stock snapped up by investors. These are the type of places that are likely to see their markets affected more significantly if the hike in stamp duty deters buyers.

In Leeds, for example, no fewer than 41% of Countrywide’s sales in the year to October were to BTL landlords. In Southampton, the proportion was 38% and in Harrow, northwest London, 35%. Plymouth and Calderdale, in the foothills of the Pennines, were close behind on 34%. “While the region with the highest proportion of investors is the West Midlands, the highest concentrations of investors are spread more widely across the country,” Earley says.

The same principle applies to local housing markets where a high proportion of buyers are looking for second homes, either as pieds-à-terre or holiday properties. Figures from the review website TripAdvisor show that the greatest demand for rentals of holiday homes — a good indication of where they exist in large numbers — is, after London, in Cornwall, Yorkshire, Devon, Wales, Dorset and the Cotswolds.

There’s every sign that in many of these areas, the rush of buyers keen to avoid Osborne’s new levy has started. In north Cornwall, where almost half of the properties in some villages are holiday homes, the telephones started ringing as soon as the chancellor stepped down from the dispatch box.

“Sellers planning to launch in the spring were saying, ‘Get it on the market now’,” reports Jo Ashby, a partner at John Bray and Partners, a local estate agency. “The more serious buyers are aiming to exchange over the winter. This injection of energy — albeit a bit of frenzy — has changed the market, at least until April.”

According to Ashby, good-quality houses that had come off the market for the winter are going back on sale now ahead of Christmas. Yet she sounds a note of caution: while Rock, Port Isaac, Newquay and other long-standing locations will probably bounce back quickly, it may not be the same everywhere. “This is going to make a bigger dent on those less-well-known or emerging holiday-market areas.”

So, the choice is yours. You can sit tight, enjoy the mince pies and gamble on prices falling in April. Or you can take the plunge and buy now — though working to such a short deadline is not for the faint-hearted, and means Christmas may be even more fraught than usual. It takes an average of 12 working weeks to buy a property. In the 17 weeksbefore April 1, we have both Christmas and Easter, when pivotal figures in the buying process — agents, surveyors and lawyers — shut up shop for several days.

“Waste no time in speaking to your solicitor and financial adviser — don’t wait until you’ve found a suitable property,” says James Greenwood, director of Stacks Property Search & Acquisition, a nationwide buying agency. “If you get a mortgage offer, make sure you know its limitations. It may exclude properties that are listed, have some commercial aspect or are leasehold.”

He also recommends avoiding any property being sold by a vendor who may change their mind. “Careful questioning will give you an idea of the motives for selling,” he says.

Harpal Singh, managing director of the comparison website Broker Conveyancing, predicts “serious resource issues” for lawyers handling sales. “It seems almost certain that buy-to-let conveyancing fees will rise to cope with the workload,” he warns.

There is one further complication. A government-led consultation process is considering what stamp duty should be paid by people who temporarily own two homes — for example, “accidental landlords” who are stuck between sales, or those who inherit a house — and whether loopholes might exist if, for instance, you split ownership between spouses. We may have to wait until spring for these answers, too.

A million pounds may not seem to go very far in the property market these days, but if you look in the right places you can make it stretch to a lovely family home- particularly if you are happy to leave the capital in your wake.

1.) There is intense competition for homes priced between £1 million and £2 million in London, according to Camilla Dell, the managing partner of the Black Brick buying agency. She says: “The market is busy with domestic owner-occupiers who have been frustrated at the difficulty in finding, and successfully bidding on, family homes in the capital. Additionally, the uncertainty in global stock markets is encouraging investors to move assets into London property. We are also representing cash buyers and those aiming to ‘future buy’ property for their children.”

2.) Robin Chatwin, of Savills, says that the farther you move from London, the more you can get for £1 million. However, this does not mean that buyers become less fussy when offered a spacious property outside London. Quite the reverse. It seems that people are more likely to shrug their shoulders when told what a property in the capital will cost. Chatwin comments: “The closer you are to London, the more vibrant the market becomes at this level as buyers largely accept the premiums you pay to be in close proximity to the capital.”

3.) The key reason for the demand for homes priced below £2 million is stamp duty. A £1 million home now attracts a stamp duty bill of £43,750. The bill for a £2 million home is £153,750; the reason for the increase is the 12 per cent rate payable on the portion of the value between £1.5 million and £2 million. A rate of 10 per cent applies to the portion between £925,000 and £1.5 million.

4.) There are more than over 4,000 properties on the market around the £1 million mark, according to Rightmove. During the past five years there has been an 80 per cent rise in homes available at this price. In the past 12 months, growth has been recorded at 18 per cent. The largest number of £1 million properties are in London, unsurprisingly.

5.) With ultra-low interest rates, £1 million mortgages have become cheaper for high earners, who still need to meet strict affordability criteria. Wealthier borrowers might also be more likely to get an interest-only mortgage approved. It can help those with, say, hefty school fees to pay which means they need to manage cash flow in the short term, but longer term will have more disposable income with which to clear the mortgage.

6.) Aaron Strutt at Trinity Financial, a mortgage broker, says: “It wasn’t that long ago the high-street lenders pretty much stopped offering £1 million-plus mortgages and if you wanted a larger loan you needed to speak to one of the private banks. But times have changed and the high street lenders are actively competing with the private banks to target wealthier borrowers like bankers, footballers and entrepreneurs. They are tempting them in with some incredibly cheap rates, low arrangement fees and the promise of faster mortgage offers.”

7.) Strutt says that more high street lenders are setting up departments to manage larger mortgage applications and they are giving their underwriters more flexibility to get the deals through. “Lenders are also pushing to supply £1 million-plus mortgages because they think it is easier to provide one larger loan rather than four or five smaller ones,” he says. “The compliance is roughly the same, there is less risk and the lenders spend less time processing applications.” Banks including Barclays, NatWest, Santander, Metro Bank, Coutts and Halifax offer £1 million-plus mortgages.

8.) Brokers report that Barclays has got some of the most competitive rates in the market and its cheapest deals are often available up to £3 million, while NatWest has a specialist large-loan team. However, Virgin Money has a fairly strict policy of lending up to £1 million. If you are looking for a £1 million-plus mortgage, there are cheap loans available. HSBC has a 2.19 per cent five-year fixed rate for mortgages up to £3 million. There is also a three-year tracker rate at 1.65 per cent from Woolwich, but there is a £1,999 arrangement fee and borrowers will need a 35 per cent deposit to qualify. As the mortgage doesn’t have early repayment charges, borrowers can switch to a fixed deal when the base rate finally increases.

9.) The process for taking out a large mortgage is similar to that for a smaller mortgage, with the lender having to assess overall affordability. However, for £1 million-plus mortgages this process can sometimes take longer. Adrian Anderson, director of mortgage broker Anderson Harris, says: “Some of the very high earners may have very high outgoings. For example, higher earners with families may have large private school fees, nannies and housekeepers, as well as extravagant annual family holidays to Saint Tropez in the summer and Verbier in the winter. These all have to be factored into affordability.”

10.) Yet in some scenarios the affordability of a £1 million mortgage can be more straightforward. Harris adds: “One of my City clients borrowed in excess of £1 million. His income multiple was circa two times the mortgage and he worked 12 hours a day, so had no time to spend any of his vast income.” Harris highlights that many people applying for £1 million-plus mortgages have the ability to purchase the property outright but are choosing to borrow to take advantage of low interest rates. He says: “Why use your own money when you can use someone else’s — and at such cheap rates?”

Estate agents will often wax lyrical about the so-called kerb appeal of a property. They might effusively flag up the elegant steps leading to a generously proportioned portico. Or the buffed front door flanked by symmetrical bay trees. The first impressions of guests or passers-by really are the barometer of the level of style or opulence within. Or are they?

What if a property looks pretty uninviting at the first glance but hides a surprisingly awe-inspiring or capacious interior, a bit like the Tardis in Dr Who or the magical doorway of Alice in Wonderland? Some artistic-minded owners revel in misleading first-time visitors by presenting a home that is not quite what it seems. No, a bland exterior or unobtrusive entrance is not always bad news for owners and agents, especially if the property is well located, and there may be benefits that are not obvious at first glance.

In fact, some buyers prefer an anonymous, unprepossessing entrance, suggests Michelle van Vuuren, of the UK’s arm of Sotheby’s International Realty. “There’s been a real step change away from overt symbols of wealth — like One Hyde Park — to very discreet and private homes,” she says. “It’s not a case of purposeful neglect of kerb appeal but a deliberate choice of nondescript doorways in the style that private members clubs such as Soho House and Blacks Club in Dean Street. The new 300 Vauxhall Bridge Road development has plain black doors with no names — ideal for those individuals who prefer to keep their assets well hidden.”

Another example is a three-bedroom penthouse in a rather utilitarian-style but sought-after block of apartments in St John’s Wood, north London. Accessed by a simple black door, the property is priced at £2.865 million through Hunters Estate Agents.

Van Vuuren adds that privacy is one of the biggest demands of wealthy buyers in crowded cities, and sometimes the conversion of non-residential buildings offers the best chances of neither seeing nor hearing your neighbours. A good example of this is a former tram shed in Camden, north London, behind whose ugly industrial metal façade hides a beautifully styled 5,000 sq ft open-plan loft conversion with four bedrooms, for sale for £4.85 million through Sotheby’s.

Camilla Dell, of Black Brick buying agents, also sells to high net worth individuals who prefer to stay under the radar. “I recently found a £12.5 million house in Chelsea for an Egyptian buyer who loved the fact that a tiny grey door opens into 8,000 sq ft of high-spec living space. Nobody passing would know the house exists which is perfect,” she says.

Of course, an unassuming home is also good for security reasons — they don’t attract the interest of opportunist burglars and they conceal what is hidden within.

That said, it might have been difficult to sell that Chelsea home to Italian buyers, however much they love the area. “They tend to be very conscious about what the property looks like from the outside, much more than what it looks like inside,” says Jo Eccles, of the buying agency Sourcing Property. “An unattractive property can certainly put off certain nationalities and minimise your audience if you are selling.”

Ah, so here comes the rub: how easy (or hard) is it to sell a property lacking kerb appeal?

A property with kerb appeal will always attract viewings, so those that don’t have it can certbe a challenge to market. “I would advise the estate agent not to show any external photos of the property so that you don’t put people off actually getting through the [ugly] front door,” says Eccles.

Charles Curran, of Maskells estate agent in Chelsea, agrees that agents have to work far harder to sell such homes. It took more than 50 viewings to sell an ex-local authority flat that was immaculately finished with a bespoke kitchen, wood floors and high-tech lighting. “Even with a wonderful interior, a series of concerns pass through an applicant’s mind about a poor exterior — how much is this going to cost to renovate, if I can’t renovate what will my friends and family think? Will I be too embarrassed entertain? People fundamentally like to have their decisions reinforced by others,” he says.

However, he adds that kerb appeal is also about the location of a property. “A tired wall surrounding a house on a prime site can be remedied by the buyer. But if there is a train behind the house or troublesome and untidy neighbours, this is not in control of the owner — either way, having realistic price expectations is the key to selling the property.”

James Robinson, of agent Lurot Brand, says that he has achieved impressive prices from buyers of unusual properties, such as converted garages, where other agents have failed — and apart from applying lots of enthusiasm, it’s about flagging up the hidden values. This especially applies to mews properties in sought-after areas of west London that were historically utilitarian service entrances to large properties and where coachmen or ostlers used to doss down. One for sale in Queen’s Gate Mews in South Kensington opens out on to a vast three-bedroom house with double-height ceilings.

“My mother taught me always to look at the ugly homes for five reasons,” says Robinson. “They are invariably better in the flesh than they are in pictures on property portals; if the location is good you can always change the house; no one else goes to see them so there is less competition; you also get better space for your money; and, finally, there is that old truism that states, ‘Always buy the worst home in the best location you can afford’.”

The property market bounced back with a 3 per cent rise in prices in the past month taking the average house value to £294,351. Alternatively, the market is growing at its slowest for two years with prices in the past month falling by 1.3 per cent to take the average price of a house to £271,000.

Two seemingly contradictory statements about the property market published this week. So which is correct? The first statement is based on Rightmove’s figures, published last Monday, and the second comes from the Office for National Statistics (ONS), published on Tuesday.

Rightmove’s figures for England and Wales are based on the asking — not sale — prices of property listings on its website; these are not seasonally adjusted, but they are up to date. The ONS data is based on UK mortgage data provided by the Council of Mortgage Lenders, so it does not take account of cash buyers. However, the figures are seasonally adjusted, although there is a two-month delay between data compilation and publication — the latest figures are for April while Rightmove’s are for June.

So both are correct althought they measure different things. And each analysis has its merits.

James Butterfill, a global equity strategist at Coutts Bank, says: “The Rightmove data is very up to date but because it is based on asking prices it can be quite volatile. The Halifax house price index has a long history but lacks a detailed regional breakdown, the Nationwide and ONS data has a shorter history but has a more thorough methodology. What is interesting, though, is that if you plot them on a graph they mirror each other — they show the same trends.”

Charlie Wells, the managing director at the Prime Purchase buying agency, says: “The house price indices are well worth reading. I look at all the indices that the various bodies put out. For property with land, I look at the land sales indices by Savills, Knight Frank and Strutt & Parker. For other residential, I look at RICS [the Royal Institution of Chartered Surveyors], because it is a fully regulated body and the advice is measured.”

The indices can provide useful general information on the trends in the property market but they do have limitations, not least because they are not comparing like with like. You also need to bear in mind where the indices originate and what exactly they measure because a slight change in the data measured can have a stark affect on the outcome.

For instance, Butterfill finds that the price to earnings ratio — a measure of the affordability of property — is a good indicator, for his investment clients, of value for money in different areas. However, the standard Halifax ratio is based solely on male earnings, so Butterfill and his colleagues have devised their own based on total household income. By the Halifax measurement, house prices are 5.16 times average earnings but based on Coutts’ calculations that falls to 4.19 times.

It is also important to take note of where the data orginates. Camilla Dell, the managing partner at buying agency Black Brick Property Solutions, says: “Do we look at house price indices when chatting to clients? Yes. Halifax and Land Registry for UK-wide statistics and Knight Frank and Savills for prime London.”

Dell adds: “It’s not like the stock market where all shares are equal. In the property market, no two houses are the same. Trying to come up with the perfect index and judge where prices are going is virtually impossible.”

Wells says: “You have to take each [index] with a degree of sceptism, after all it only takes three facts to make a stat.”

Nonetheless, such is our national obsession with house prices that — rather like weather forecasts — they become something more than guides to general trends. In our minds, they somehow become solid facts that pertain to us personally.

Rob Weaver, the director of investments at property crowdfunding platform Property Partner and a former property valuer, says: “People can put too much store in them. They are a guide showing the trajectory and velocity of the market, but they are not a lot of use for determining value.”

When Weaver is valuing property for his investors he commissions an initial full valuation, this is revised on a monthly basis against the Land Registry data which is, in turn, regularly backed up by an independent desk-top valuation by a property valuer — in which data is gathered on sales of comparable properties.

One of the problems, explains Weaver, is that indices don’t take account of investments made: you may own a house worth £100,000 and by adding a £20,000 conservatory increase the value when you sell it to £125,000. The indices might record a move from £100,000 to £125,000 but won’t record the £20,000 invested giving a false impression of what is happening in the market.

Jo Eccles, the managing director of the Sourcing Property buying agency, says: “I don’t ever look at indices when bidding on a property. It doesn’t matter what the ONS says, the only thing that is meaningful is what similar houses on that street have sold for.”

Eccles prefers to look at trade statistics such as LonRes for recent comparable sale prices and calls local estate agents to gather data on recent sales. She says that those not using a buying agent should look up similar properties on the market and call the estate agents for properties sold subject to contract to find out the most up-to-date prices and ask for details — for instance, if a similar property has sold for £650 per sq ft and it has a large southwest-facing garden and yours has a small north-facing garden maybe a sale price of £600 per sq ft is reasonable.

Neither do the indices take account of the premiums that people are prepared to pay to secure the house they want, says Wells, maybe because they want to be in a particular school catchment area or because they want to buy the neighbouring house to knock through or it is close to a relative. As Weaver points out, the compilation of indices is purely mathematical while house buying tends to be an emotionally led decision.

The cost of deals is falling but lenders are the most generous to new landlords with substantial deposits, says Melanie Wright

Falling buy-to-let mortgage rates combined with higher rents mean that if you’re considering becoming a landlord, now could be the time to act.

According to the latest HomeLet Rental Index, released last week, rents rose in 11 out of 12 regions across the UK in the first three months of the year. The average monthly rent in the UK is now £902, or £270 if you exclude the Greater London area, and last month the estate agent Barnard Marcus reported that the average rent in the capital was £1507. While this may be bad news for tenants, it means landlords are benefitting from higher returns.

Martin Totty, chief executive at Barbon Insurance Group, parent company of HomeLet says: “With average rents for new tenancies across the UK now more than 10 per cent higher than a year ago, what we are seeing is a market that is experiencing sustained demand from increasing numbers of people requiring privately rented properly.”

Research for The Times Money by Moneyfacts.co.uk reveals that the average buy-to-let two year fixed rate is currently 3.36 per cent, compared with 3.94 per cent a year ago. The average buy-to-let five-year fixed rate is 4.26 per cent, down from 4.66 per cent a year ago. Several lenders have reduced their buy-to-let mortgage rates in recent weeks. Natwest for example, has cut some rates by up to 0.55 per cent. It is now offering a two-year fixed deal at 2.25 per cent, although there is a hefty £1,995 arrangement fee. This mortgage is available to first time buyers, second time buyers and those mortgaging with a 40 per cent deposit.

Although low buy-to-let rates might be tempting, the best deals are reserved for those with substantial deposits. For example, Santander offers a two-year fixed buy-to-let rate at 2.35 per cent with a £1,995 fee if you have a 40 per cent deposit, but its two-year rate if you have only a 25 per cent deposit is 2.79 per cent, again with a £1.995 fee.

Simon Tyler, of Tyler Mortgage Management, says: “Lenders can be very fussy about by-to-lets and probably the biggest differentiating factor is the size of deposit you have to put down.”

“If you only have a 20 per cent deposit, hardly anybody will want to lend and the deals that are available are relatively expensive with big fees. For example Aldermore Bank offers an 80 per cent buy-to-let deal with a variable rate of 4.48 per cent and a fee of 3 per cent of the loan amount. So if you are borrowing £20,000, that’s a £6,000 fee.

“Some people may think these sorts of fees are worth paying in order to get on the property ladder but the fact is that it is very difficult to meet other criteria, such as receiving enough rent to cover the mortgage interest by a sufficient margin to qualify, let alone make a profit.”

Another potential pitfall is void periods. While landlords must be prepared for times when their rental property is empty, what kills an investment is lengthy void periods, warns Camilla Dell, managing partner of Black Brick, a property buying agency. “Generally speaking, flats are a better investment because the void periods tend to be smaller. Even if you’ve got a lot of money to invest it’s better to spread it out over lots of units than buy one large one.”

Yields are likely to be greater too. “A really good one or two bed-flat should be getting a yield of at least 3 to 3.5 per cent. With a much larger home that could drop to 2 per cent or under.”

Age matters

Your age is determining whether your application for a buy-to-let mortgage will be accepted. Many lenders impose a maximum age cap of 70 or 75 at the end of the mortgage term although others are less strict.

David Hollingworth of London and Country mortgage brokers, says “For example, Kent Reliance can lend to a maximum age of 85, and lenders such as National Counties Building Society will assess on a case by case basis rather than impose a strict cap.

“The Mortgage Works has changed its approach to a maximum age of 70 at application and a borrower could take out a 35- year mortgage term. This recognises that some investors will be considering buy-to-let as part of their strategy to generate income in retirement, especially given the introduction of more flexible pension rules.”

If you’re a younger borrower, lenders will generally want you to be at least 21 years old and an existing property owner.

Mr Tyler say as: “Lenders are very wary of first-time buyers applying for buy-to-let loans because they are available on an interest-only basis with far fewer affordability checks, but then living in them themselves.”

The rent on the property you plan to buy must cover 125 per cent of the mortgage payment, and many lenders require that you have a minimum annual income. For example, Coventry BS, Santander and Accord require all buy-to-let borrowers have a minimum annual income of £25,000. Mr Hollingworth says “The minimum income requirement can be different depending on whether you’re applying on your own or with someone else. For example, Coventry wants at least £30,000 for joint applicants, although some lenders don’t distinguish between single and joint.”

Location, location, location