Prices for prime homes in the capital have slumped, with supply soaring and fewer buyers around.

Prices of London’s most expensive homes are at the lowest level in seven years, with some buyers able to strike bargains not seen since the financial crisis.

In October values of property sold in the priciest postcodes of the capital fell by 3.3pc compared with the same month last year, according to LonRes, a data provider. This means that prices per square foot for the capital’s most exclusive homes are now the lowest they have been since 2013.

The number of properties on the market in prime central London is up by 68pc compared with last year, LonRes found. However, sales agreed have not risen in tandem, as international buyers have been unable to visit during the pandemic.

As a result, bargains are available the likes of which have not been seen since the financial crisis, said Camilla Dell of Black Brick, a buying agent. “This time, it’s even better because there are fewer buyers around to compete with. There are not many moments I’ve seen where you can get these kinds of deals. ”

It is in the city’s “golden postcodes” – traditionally prized spots such as South Kensington, Knightsbridge and Belgravia – where you can find the best bargains, she added.

“These areas have been hard hit by coronavirus. Firstly because they’re traditionally dominated by overseas buyers.

“Secondly because properties here are mostly flats without outdoor space, which is not what domestic buyers are after at the moment,” she added. “One agent who is trying to sell a £40m home in Belgravia said it was like tumbleweed.”

In Knightsbridge and Belgravia, prime property prices are currently 16pc lower than they were at their peak in 2014, according to private bank Coutts’ London luxury property index. It uses data from LonRes, which found that the cost of property in the area is now £1,886 per sq ft – the lowest it has been since 2011.

In South Kensington prices are down by 16pc from their peak, the lowest they have been since 2012.

“Fulham and Earl’s Court have been particularly hard hit this year because they have lots of new-builds, which traditionally get snapped up by international buyers,” Ms Dell said. Prices here are down by 19.2pc compared with peak levels.

London’s leafy suburbs have fared better thanks to their larger homes and bigger gardens. In Wimbledon, Richmond, Putney and Barnes prime property prices have risen by about 4pc in the past year, according to Coutts. Homes in these areas take on average 135 days to sell – a month faster than the rest of the prime London market. As a result the premium buyers pay for a luxury property in the city centre compared with its outskirts has dropped from 91pc in 2019 to 82pc this year.

Falling demand in SW and W postcodes has opened the way for bargains. Ms Dell recently secured a two-bedroom apartment in Ebury Square, Belgravia, for a client for £3.32m – with a discount of £1m (22pc) off its original asking price.

Jeremy Gee of Beauchamp Estates, a property firm, said he was currently trying to find a buyer for an off-market property in central London that had a £10m discount. “It is 16,000sq ft and would normally cost about £40m but the buyer is only asking £30m,” he said.

Savills, the estate agency, has predicted that prime property values in the capital will jump 17.5pc by 2024, ending a long downward trend.

The firm’s Lucian Cook said: “The data suggests that the top end of the market remains poised for recovery as soon as international travel resumes and London’s streets regain their normal buzz. The successful development and distribution of a vaccine against Covid-19 is an important part of this.”

While some are worried that the city will lose some of its shine following Brexit and the introduction of an extra 2pc stamp duty surcharge for overseas buyers in April, others are more confident.

“London isn’t the cheapest city for property taxes, but it’s far from the most expensive either,” Mr Gee said. Buyers in London do not have to pay holding taxes on their properties, as they do in New York, Madrid or Paris. “There’s a lot of pent-up demand from international buyers, and extra stamp duty won’t put them off,” he added.

Premiership players with budgets of £15,000 per month are finding it difficult to rent in the footballer zone south-west of London

Footballers in the Home Counties are having to move into hotels ahead of the new season as the supply of high-end rental homes has dried up.

Alex McLean, head of the sports team at Knight Frank’s relocation services business, said that a lack of pricey properties to rent along the A3 corridor out of south-west London means “a lot of players are ending up in hotels”.

Accommodation budgets of Premiership players, who often opt to rent, especially at the start of their club contracts, often exceed £15,000 a month, said Mr McLean. But the pandemic has shrunk local supply in their favoured towns, which include Oxshott, Esher and Cobham in Surrey.

This means that newly-signed players, such as Thiago Silva and Ben Chilwell who are moving to Chelsea, may find it difficult to rent a property near the club’s training ground in Cobham.

James Dodds of Grosvenor Billinghurst, a Surrey estate agent, said: “I can’t remember a time when there was this much movement in the super high-end rental market.” Footballers in these areas also have to compete with wealthy workers at nearby tech firms.

The post-lockdown property “mini-boom”, driven by Chancellor Rishi Sunak’s stamp duty holiday and a shift to working from home, means that many high-end homeowners are taking the opportunity to sell their homes now while prices are high, and renting until prices fall when the impact of the recession bites. The sales market had been sluggish for several years before the pandemic.

In the three months to August, the number of homes worth more than £5m for sale outside central London doubled compared to the same period in 2019, according to Knight Frank.

Meanwhile, between April and August in the south-west corridor, which includes areas such as Ascot and Cobham, the number of high-end rental properties coming to the market fell by 20pc compared to the same period in 2019. For homes renting for more than £15,000 per month, the number fell by 55pc.

The footballer zone along the A3 is an anomaly: across London and the Home Counties, over the same period, the number of overall rental listings jumped by 28pc year-on-year.

Within the capital, the contrast is even more stark. Camilla Dell, of Black Brick, a buying agency, said landlords who have recently renewed tenancy agreements in London have had to accept 10pc and 20pc rent reductions. “Flats without outside space are faring the worst,” she added.

There is more demand than usual from footballers to rent big homes in this area, and some are moving there because they want more green space after lockdown. “Chelsea has spent a lot of money on new players, but there are also footballers for the London clubs who have decided to move out this way,” said Mr Dodds.

There is new demand for pricey rental homes in this area from footballers at south London clubs such as Crystal Palace and Millwall as well as Chelsea, Fulham and south coast teams such as Bournemouth and Southampton, said Mr Dodds.

The footballers looking to rent now are late to the trend. When the pandemic started, “there was a snap reaction from some very, very wealthy Londoners to rent a Surrey mansion,” said Mr Dodds.

“We had a chap where there wasn’t a figure for a budget, we were trying to negotiate him renting a whole hotel and its cottage in the grounds. The deal was going into a couple of hundred thousand pounds a month,” said Mr Dodds.

But while demand for luxury rentals has spiked, supply has dropped.

Agents are reporting a sales surge, while analysts are forecasting imminent price falls. Is there a way to make the most of the difference?

The property market is on a rollercoaster: while agents have reported a surge of demand and deals since restrictions were lifted in England, analysts have forecast deep price falls this year.

So is there a way to take advantage of these peaks and troughs?

One way to do that is sell up now, while the market is in a frenzy, then rent while biding time as prices fall – and then snap up a bargain.

This is what Theo Taylor, 71, plans to do. He has lived in Hemel Hampstead, Hertfordshire, for 20 years with his daughter and his wife, who passed away last year. Before coronavirus hit, he was preparing to downsize to Wiltshire with his dog, Pebbles.

“Now, I’m thinking of selling this year as planned, trousering the cash, renting in Wiltshire and then buying over the next year with the added leverage of being a cash buyer,” he said.

e is about to put his house on the market for £765,000, and intends to move west with a budget of £600,000 to £650,000. He wants to wait until he finds a home that he really wants, and then will be able to move quickly.

But he could benefit from falling house prices, too. “I think prices are going to fall,” said Mr Taylor. “The furlough scheme will end soon, and when it does I think there will be significant redundancies and business closures, and when that happens I think the property market will go down.”

Is now the best time to sell?

Buyers have rushed back into the market in England since the restrictions were lifted. Agreed sales are nearly at pre-lockdown levels and sellers are so optimistic that in May, asking prices were 1.9pc higher than in March, according to property portal Rightmove.

David Ruddock, of estate agents Carter Jonas, said that while pent-up demand is driving the recovery, it is not just rooted in lockdown. “It has been building since the middle of last year, long before the pandemic began,” he said. Buyers had been holding off since the June 2016 referendum to see what would happen with Brexit and were just starting to return to the market after the decisive Tory election victory brought more clarity in December.

There is also a new group of buyers who have become dissatisfied with their homes during lockdown, said Mr Ruddock.

But the effects of the coming recession have not yet filtered into the market. Nine million people currently have their wages supported by the government and one in seven mortgaged households are currently protected by a mortgage holiday. When these measures end in the autumn, there could be a spike in forced sellers, and a major hit to buying power.

Lenders are certainly expecting the recovery to have a short life expectancy. The building society Nationwide has forecast a 13.8pc drop in house prices and has withdrawn mortgages to buyers with less than a 15pc deposit accordingly.

The current huge level of demand and the pessimistic outlook suggest that now may be the best time to sell for some time.

How will price falls vary across the market?

These forecasts are largely for the UK as a whole, but there will be major differences in house price changes across the country and at each stage of the property market.

The entry-level section of the market will likely be worst hit, said Mr Ruddock. First-time buyers are most likely to be affected by redundancies. They are also most reliant on the availability of lending, and mortgages for those with small deposits are scarce. The number of agreed sales at the lower end of the market is not recovering at the same rate as those of prime homes.

Meanwhile, values in rural areas are more likely to hold their value. The markets here are less vulnerable to changes that affect buy-to-let investors and overseas buyers, who are currently held back by travel restrictions and face a new stamp duty charge. Affordability here is already better than in the cities, and rural markets will benefit from new demand for homes with outdoor space.

Camilla Dell of Black Brick, a buying agency, said: “A lot of people want to move out of London now that they can work from home.”

In the capital, “the market has already dropped,” she added. “The deals we had agreed pre-Covid have been renegotiated by about 5pc.” Large-scale new build developments will be particularly vulnerable to further falls.

When will price falls bottom out?

“Playing the market is a risky strategy, as timing the bottom of the market is something nobody can predict,” said Ms Dell. “I think we are looking at a few months.”

Estate agents Savills and Knight Frank have both forecast that house prices will return to growth in 2021.

The housing market’s recovery will be closely tied to the UK’s economic strength. But the relationship between the two is not necessarily always one of cause and effect. Analysis by Deutsche Bank showed that during the global financial crisis, GDP started to fall in March 2008 and bottomed out in June 2009 – a gap of 15 months. Meanwhile, house price falls started earlier in September 2007 and lasted for a longer period of 18 months.

In this case, however, GDP has fallen first, with a plunge of 20pc in April; perhaps this time around, an eventual rise in GDP could be a precursor to a house price recovery.

But even if a buyer calls the market right, they could be held up by a lack of available homes, said Ms Dell. When a market is falling, sellers are also less keen to list their properties, meaning that pickings are slim.

“It is a bit like going to the Harrods sale,” said Ms Dell. “Yes, the discounts are bigger, but is there anything you want to buy?”

Many buyers are worried about getting into negative equity as soon as they have purchased their homes. This means that you own a property that is worth less than what you borrowed to pay for it.

Buyers who have purchased with high loan-to-value mortgages are most at risk. If you have purchased just 5 per cent of your property with cash, for example, you will quickly be in negative equity if house prices fall by 13 per cent, as forecast by the Centre for Economics and Business Research (CEBR).

But that would not mean that you have to immediately sell your house at a loss. Here, we look at your options, and what buyers can do to protect themselves.

What happens if you get into negative equity?

“The biggest misconception about negative equity is that people think they’re suddenly going to be repossessed,” says Nick Morrey, of John Charcol, an independent mortgage broker. “That couldn’t be further from the truth.”

If you are able to wait out the market until prices climb, you should be fine. “Over every five year period, prices have ended up higher, even if there is a crash in the middle,” says Morrey.

Most analysts are predicting a “V-shape” economic recovery after lockdown is lifted, and both Capital Economics and Knight Frank expect house prices to return to growth in 2021. “If you do get into negative equity, hold on,” says Tim Hyatt, of Knight Frank.

Most lenders have removed high loan-to-value mortgages for new purchases, says Morrey, but it is still possible to find options for transfers, as these don’t require the lender to send a valuer to the property. If your mortgage deal is coming to an end, talk to your lender about what options you have for switching.

If you’re not able to transfer, you will be moved to a standard variable rate mortgage when your current deal ends. While the costs could be higher than what you were paying before, the difference will be mitigated by the fact that the Bank of England base rate is currently at a historic low of 0.1 per cent.

What if you have to move house?

If you’re in negative equity and you can’t sit tight, your situation is more problematic. You will need permission from your lender to sell if the sale price is likely to be less than the remaining value of the mortgage. And you will be personally responsible for making up the difference in value.

A better option is to contact your lender and ask for consent to let out the property, says Morrey. In other words, you can become an accidental landlord.

Be wary that rental values are likely to take a hit, particularly with the expected influx of stock from the short-term lettings market with the collapse of the travel industry. But hopefully, the rental income can cover your mortgage payments and free up your disposable income so that you can rent elsewhere while you wait for property prices to recover.

Is now a good time to negotiate a deal?

The Government has issued strong guidance against all but essential house moves during lockdown. While sales can still technically proceed, the market is a minefield. Many chains are falling through and some buyers can’t meet their completion dates.

When lockdown lifts, however, some buyers might consider the market an opportunity. If house prices are falling, “you’re likely to be able to make a cheeky offer,” says Morrey.

There just might not be much stock to take a punt at. After a crisis, “we will always see a bit of distressed selling,” says Camilla Dell, founder of the London buying agency Black Brick. “There will be some undoubtedly, but I think it will be few and far between.” The Government’s measures to protect earnings, mortgage holidays, and low interest rates will mean fewer sellers will be forced to take big price cuts.

If you are trying to negotiate, “the key to success is understanding your seller”, says Dell. If you know why, or how urgently they need to sell, you have more bargaining power.

You will also have an advantage if you “can demonstrate that you can move quicker, and anyone sitting on cash is in a great position”.

For those that aren’t may find that they simply can’t buy. Lenders have withdrawn high LTV mortgages from the market en masse. The available mortgage offering has shrunk by nearly a third and you will likely need a deposit of at least 20 per cent to secure lending.

Which parts of the country will be safest to buy in?

In the immediate term, the impact of coronavirus and the lockdown will be “very much uniform across the country,” says Lawrence Bowles of Savills Research.

When the restrictions lift, however, “we would expect equity driven markets to recover first,” he says. In prime central London, for example, people are more likely to buy with cash rather than with a mortgage, so purchasers will be able to move more quickly.

Recovery will also be dependent on the local employment markets. According to analysis by the CEBR, 48 per cent of the UK population works across the sectors most affected by the coronavirus lockdown: manufacturing, construction, retail, hospitality and other service sectors.

But their concentrations are highest in particular regions. In Yorkshire & the Humber and Northern Ireland, 60 and 59 per cent of workers are in these industries respectively. Disruption to the job markets here is likely to have a bigger impact on the local housing markets, according to CEBR.

But some buy-to-let investors are spotting opportunities, and are getting their deals lined up for when the restrictions on purchasing are lifted. The share of buy-to-let mortgage searches on Twenty7Tec saw a small uptick last month. In the capital, prospective investors are “circling”, said Camilla Dell, managing partner at London buying agency Black Brick. “There’s a lot of cash swirling, looking to swoop in,” she said.

Savills has forecast a short-term price drop of 5-10pc. “You need only look at the rate that lenders have pulled out their mortgage offering,” said James Tucker of Twenty7Tec. Nearly a third of the mortgage deals on offer have been retracted.

For buy-to-let investors, short-term price falls mean long-term yield increases. In London and the South East, high property prices have meant low yields, leading to an exodus of buy-to-let investors to the North, seeking higher returns. But falling prices have already been boosting rental yields.

House prices in the borough of Kensington and Chelsea were 11.1pc down year-on-year in the last three months of 2019, according to estate agency Hamptons International. This meant the borough recorded the second-largest jump in rental yield of all local authorities in the country. Yields climbed 1.5 percentage points in two years, to 4.2pc.

Similarly, property prices in the City of London fell by 1.7pc, which helped boost yields by 1 percentage point over two years to 5.2pc. If price falls continue, London could open up again to domestic landlords who will be able to get higher long-term yields on their investments. This may even be enough to offset the effects of the reductions in tax relief on buy-to-let mortgages which have seriously hit investors’ pockets since their phased introduction began in 2017.

This is particularly the case because rents are unlikely to take the same hit. Rents do not move in line with house prices, said Gráinne Gilmore, head of research at Zoopla.

After the last financial crash, “the rate of decline in rents was more modest than capital value for homes,” said Ms Gilmore. “When house prices dipped into negative territory in 2011, rents were growing at the strongest pace in four years.”

When the sales market is stalling, people are more likely to hold off on purchases and stay in rentals. “When there is uncertainty, the rental market comes into its own,” added Gary Hall, head of lettings at estate agency Knight Frank. It has forecast that house prices will fall by 3pc over the course of 2020, and that London rents will stay constant. There is an opportunity for investors here, said Angus Stewart of the digital buy-to-let broker Property Master, “as long as they’re sufficiently liquid”.

Those looking to invest will find that they have new competition: short-term landlords are being squeezed by the collapse of the travel industry, and there is already an influx of these properties to the long-term lettings market. Another point of competition could be vendors who are unable to sell their homes if there is a downturn, and so may become accidental landlords.

But Mr Hall is bullish. “Last year we had eight applicants to every rental property listing,” he said. He does not anticipate that rental supply will outstrip demand.

So where will be the best places in the country to invest? Hartlepool in County Durham has the highest rental yield of any local authority in the country, according to Hamptons International, at 11.9pc. The average house price is £113,160. Meanwhile, Pendle in Lancashire has recorded the largest jump in yield growth in the last two years, up 1.6 percentage points to 10.1pc.

When it comes to investing, Mr Hall recommends new stock. “We agreed 27 tenancies last week and the majority were new-build,” he said. Tenants feel more comfortable moving into unoccupied properties, he added. Developers with cash flow problems might also be more open to negotiations on sale prices.

But perhaps the most important factor for investors in the wake of the lockdown will be local employment rates, said Aneisha Beveridge, head of research at Hamptons. These will underwrite rents during the coming months. While the biggest cities will be safer bets, the current winner is the local authority of Eden in Cumbria, which currently has an unemployment rate of 1.6pc. The average house price is £198,480, according to Hamptons.

Why London’s imminent property boom is not all that it seems

By Melissa Lawford

Typically, after the Christmas break, the housing market in London is “an absolute desert,” says Simon Barry of Harrods Estates. This year is a different story, he says. In the wake of the Tory election victory, estate agents seem instead to find themselves in an oasis.

Even the Russian buyers are coming back.

Sales of luxury homes have spiked in the capital, a market which has long been in the doldrums. In the month after the election, sales of £2 million-plus homes have jumped by 69 per cent year-on-year, according to analysis firm LonRes.

Everyone is waiting for the surge to translate into price rises. “It is happening, we can feel it happening on the ground,” says Caspar Harvard-Walls, a buying agent at Black Brick. “Straight away, sellers who would have maybe taken 5 or 10 per cent off their asking price now won’t budge.”

New listings are now being set a few percentage points higher than they would have been this time last year, he adds, so “we have to be a lot more aggressive in negotiation.” Soon, he says, “people will begin to think they have missed the bottom of the market.”

So is the London property market about to go bonkers?

The headline figures of the latest HMRC stamp duty receipt data are utterly boring. Overall, in the last three months of 2019, total sales volumes in the UK moved by less than half a per cent.

But look closer: from October to December, the number of £1 million-plus sales jumped by 12.8 per cent on the same period in 2018 to a total of 5,300. “That is the highest number of £1 million-plus residential transactions for the last quarter of a year in at least the last decade,” says Lucian Cook, research director at Savills.

The implications for the luxury sector of the London market are huge. The largest concentration of these properties is in London and the South East, says Cook, and the numbers likely reflect “the banked sales after the election”.

Rightmove reported that January was its busiest month ever, and said that agreed sales in London jumped by 26.4 per cent on last year’s total.

While the biggest jump is in the number of super-expensive prime London homes sold, the boost is not just in the glitzy heartlands. LonRes found that in January, sales of homes in “prime fringe” areas, such as Clapham and Southwark, were up by 28.4 per cent year-on-year.

But there is a major caveat: the number of homes sold might be up, but prices are still down. Prime London sales prices were 5.5 per cent lower in January than the year before, according to LonRes. This is a time to buy a bargain, and while some vendors may well be taking a punt at hiking their prices, but they are certainly not the ones who are currently making sales.

And if they do raise their asking prices, this will likely start to stall the market again. “A sustained pick-up in activity depends on sellers keeping price expectations in check,” says Cook.

Across London, “affordability will be a limit on price growth,” says Neal Hudson of research firm Residential Analysts. Demand might be up in the capital, but that does not change the purchasing power of buyers, particularly first-timers, who are limited by mortgage regulations and prices that are still sky-high compared to wages.

The election result was not necessarily the turning point that it has been hailed as. The HMRC figures suggest that the momentum currently taking over the market started over the summer, and continued through the rest of the year. Typically sales fall off after September.

Calling the recent rise in London sales a ‘bounce’ is a misnomer, says Barry. “The momentum has been building for months.” That shows that, certainly in the wider London market, the right pricing of a property matters more than political clarity.

Sellers should also note that the current pick-up in activity is nowhere near as big as it sounds. “Prime central London is recovering off a low base,” says Hudson. Both 2018 and 2017 had weak ends of the year. The numbers “in part simply reflect things being not as bad as they were,” he adds.

There are also some more hurdles on London’s horizon. Brexit trade negotiations will bring back the uncertainty the the election result temporarily pushed away, says Cook.

There is also the government’s pledged introduction of a 3 per cent surcharge on overseas buyers. This is likely to “put buyers off at the lower end,” says Hudson. It will be the foreign investors buying one- and two-bedroom buy-to-let flats who will see their yields significantly hit by the extra tax.

As for the multi-millionaires, they will simply refuse to pay the extra, says Barry. When stamp duty goes up, “it’s been vendors who pay most of it [by lowering prices],” says Barry. “We have seen the market fall from a great height since the 2014 stamp duty changes.”

London is also part of a wider story of global prime real estate. “There are signs that prime markets across the world are struggling,” says Hudson. He notes the downturns in Vancouver and New York in particular. The rule of the old guard could simply have come to an end.

“We could see a stronger market for a number of months,” says Hudson. As there is a shortage of homes on the market and a low turnover of property, it doesn’t take much for transaction growth to filter into price rises. “But that trend for rampant growth that we saw from 2010 to 2014 is unlikely to return.”

The sheer drama of driving – let alone parking – in cities, along with a bigger push to be healthy and walk or cycle instead, is seeing super-rich buyers increasingly willing to forego off-street parking spaces with their multi-million pound mansions. But access to a private jet or helicopter, on the other hand, has never been more desirable – particularly when it comes to viewing properties.

Private aircraft ownership is on the rise, driven by the US (New York is the private jet capital of the world, according to Knight Frank’s Wealth Report 2019, with nearly 67,000 flights taken in 2018 from Teterboro airport, 12 miles from Manhattan).

The number of global billionaires is on the up too, and jet owners spend about 1% of their wealth on private aircrafts, with an average of $16.4m per plane, says Knight Frank.

Travelling by private jet isn’t so much a status symbol as a matter of pure practicality, I am told by London agents who are increasingly seeing their clients buy from the skies.

“Every minute counts. Ultra high net worth clients live much faster lifestyles and private travel allows them to fit in more activity – and of course do things in comfort and style,” says Camilla Dell, director of Black Brick buying agency. It’s the norm among London clients spending £20m or so on a country estate, she adds, to travel by helicopter rather than car.

With Battersea the only place to land a helicopter in central London, a chopper only really comes in handy when viewing in the countryside. Oxfordshire-based buying agent Jess Simpson says her clients use private jets or helicopters all the time.

“It might not be obvious, as they’ll use an airport near the property, then travel to the property by helicopter or car. But it’s a great time-saver and you see so much more from the air than the road,” she says. “Many buyers in the £20m+ market search a wide geographical area, so viewing by helicopter is the only way to cover the distance.”

In the south of France, getting to know the lie of the land from the air is commonplace among UHNW buyers. “It means no queuing, no delays, no fuss,” says Tim Swannie, director of the French buying agency Home Hunts, who says a helipad is on the shopping list of most of his wealthiest clients. He is marketing a five-bed house with a helipad in St Jean de L’Esterel, with views over the Bay of Cannes, for 9.85m euros.

“One financier recently sent a friend to view six properties for him in one day, spread across the Riviera and Provence, so he chartered a helicopter,” says Swannie. When the buyer came to inspect in person, he landed his jet at Cannes private airport, saw the properties, snuck in lunch in a Provencal chateau, then was back in London by late afternoon. “The next day, he bought a villa in Cannes and a hunting domain near Aix-en-Provence,” says Swannie.

Some property owners even carry out luxury home renovations by private jet. “One couple were restoring a house on the French Riviera. They sent two planes loaded with antique furniture and art from Geneva and City Airport and we arranged the logistics in France,” says Swannie.

As flying privately becomes more desirable among the wealthiest property buyers, so too are properties that offer places to land their helicopter – or borrow a plane. South Florida saw a 35% increase in private jet travel last year, according to ISG World’s Miami Report.

In Miami, competition for UHNW buyers is fierce among the city’s super-prime, starchitect-designed schemes. One way to set yourself apart from the rest is to offer access to the skies.

At One Thousand Museum Residences, designed by the late architect Zara Hadid, developer Louis Birdman describes the need to offer an amenity that isn’t typically offered in Miami – and the answer is a private rooftop helipad.

“There are virtually no private skyscrapers in the US that have such an amenity. We have buyers from Latin America, Europe and New York where transportation by helicopter is far more common and they have chosen to buy here for the convenience,” says Birdman. Residences start at $5.8m through One Sotheby’s International Realty.

The Ritz-Carlton Residences, Miami Beach – priced from $2m for a two-bed condo to $40m+ for a 10,000 sq ft villa – offer Miami’s first navigable marine helipad on Biscayne Bay, enabling buyers to view the property by air, and residents to schedule helicopter shuttles through the concierge.

“The helipad is a three-minute ride away by day yacht – then owners can get to and from the airport in just a few minutes, or take a trip to the Keys or the Bahamas,” says Ophir Sternberg, CEO and founding partner of Lionheart Capital, the resort’s developer.

“We often see international or out of state buyers requesting helicopter tours, allowing them to view the layout of the surrounding neighbourhood and proximity to landmarks such as the airport, major highways, schools and the beach. It also allows buyers to see the project from a 360 degree vantage point,” Sternberg adds.

And at the Turnberry Ocean Club on Miami’s Sunny Isles Beach – where residences cost $3m-$35m – buyers have priority access to the private jet facility at Opa-Locka Executive Airport, including aircraft maintenance and a full-service concierge.

“It’s the only residential condominium development that provides a true private FBO (Fixed Base Operator) as an amenity to our buyers – and many people are purchasing directly from the skies via plane and helicopter sales tours,” says Bruce Weiner, Head of Fontainebleau Development. “Many of our residents would fly private regardless, so the access is an added benefit that allows them to land private, just minutes from home.”

Meanwhile, in Greece, super-rich buyers island-hop by chopper. New luxury developments with private helipads include One & Only Kea Island – where two- to five-bed residences cost from €3m-€7m – and Amanzoe in Porto Heli – whose turnkey villas on one- to five-acre plots cost from €3.2m for two bedrooms – both schemes through Sotheby’s Realty.

“We have flown clients by private jet to Athens and then taken a helicopter to Amanzoe for a 24 hour viewing experience,” comments Guy Bradshaw, director at UK Sotheby’s International.

Developers in Dubai have taken private aviation for property buyers one step further. Bradshaw reports that Omniyat, developers of The Dorchester Collection Residences in downtown Dubai, where two-bed residences start at around £3.1m, have partnered with Aston Martin to create the first people-carrying drones.

Satisfying the UHNWI’s need for speed and one-off experiences, these futuristic, self-driving machines are surely a marketing tool no super-prime scheme – with enough space to land – should be without.

A vastu-compliant north London house, £9.5m with Arlington Residential.

By Andrea Marechal Watson

Vastu, often seen as an Indian version of feng shui, dates back thousands of years. Tips for house construction include performing puja rituals on auspicious dates, preferably after consulting an astrologer.

The location and shape of the plot, light, water and internal arrangements of doors, windows and rooms are considered vital to ensuring the health and well-being of occupants.

Vastu has begun to pop up on the UK’s highly international property market. “Feng shui is a big thing for many of our clients, who will not set foot in a property unless it has had the once-over from their feng shui master,” says Penny Mosgrove of Quintessentially Estates, an estate agent. “A similar set of principles exist in vastu shastra.

“This year I was asked to find a home in Notting Hill that was vastu-compliant. There had to be various ‘main’ entrances, no bathroom near the main door, doors that were not black, a door that opened in a clockwise manner and an entrance that had not got a shoe rack near it, nor a bin.

“All mirrors needed to be on the north wall and social rooms needed to face north or at least north-east. At the centre it required a brahmasthan, which is a space for reflection without any obstructions to it.” Eventually, the right house was located and bought.

A flat in north London, £5.8m, with Arlington Residential.

There is a growing Indian community in London, active at the middle to top end of the property market. Following changes in 2015 to the Liberalised Remittance Scheme in India, which increased the capital that buyers can bring into the UK to $250,000 (£195,000) per person per year, there was a surge of buyers.

“Indian buyers are still very prevalent in London – especially when you look at the wider number of Indians that are buying, known as non-resident Indians,” says Camilla Dell, of buying agency Black Brick. “Indian resident buyers are still somewhat limited in what they can spend on an overseas property due to exchange control in India. Although the rules have become more relaxed, families are only allowed to transfer $250,000 per family member per year outside of India.

“So a family of four, after two years, would have a budget of $2 million to spend on a property. Non-resident Indian buyers are not subject to the same restrictions and so tend to have higher budgets.”

“We noticed a significant increase in Indian buyers over the last six months,” adds Simon Garcia of Quintessentially Estates. “The softening of prices and fall in the value of sterling both played a part, as many trade in dollars.”

Pimlico and Westminster accounted for around a third of all purchases by these families, both as investments and homes. Marylebone, with its boutique shops and village feel, is also popular.

Around half of Indian buyers search for vastu-compliant properties, and for those who do, it’s a deal-breaker for a sale. “This continues to be very difficult to fulfil, particularly on properties that are already built,” says Dell.

Marc Schneiderman, director of estate agency Arlington Residential, recently sold an £8 million house in St John’s Wood to an Indian family after they dismissed several other houses due to their orientation. “Their vastu adviser inspected the house and made suggestions such as removing the water fountains in the garden and repositioning furniture,” he says.

There are advantages to buying in a new development. “Last week [we] concluded a deal for a non-resident Indian client on an off-plan development,” says Dell. “The developer was open to changing the layout to meet our client’s vastu requirements.” Buying off-plan with staged payments is also easier for buyers affected by the limits of exchange control.

Many Americans would have us know that they “saved” us from the Germans in the Second World War. As we approach the 75th anniversary of the Normandy Landings, I’ll leave that heated debate for another day.

But now they might be coming to save us from something else: our sluggish property market.

Buying agent Black Brick reports that there has been a big jump in the number of Americans wanting to buying property in the most expensive areas of central London, accounting for nearly one third of its clients in the year to June.

These American buyers can now get a 40 per cent discount on what they might have paid at the top of the market. Property prices in many areas of prime central London have fallen 15 to 20 per cent, and they have the exchange rate behind them too: in July 2014, the pound was worth $1.71, but in the last two years it has traded between $1.27 and $1.43.

“Our US clients are not put off by Brexit or the threat of a Corbyn government; instead, they view the market as a good buying opportunity,” says Camilla Dell, of Black Brick.

“Our largest transaction for a US client – more than £20 million – was because he had decided to relocate to London and run his technology business from here. After Silicon Valley, London is the next best place for IT entrepreneurs. We have the infrastructure and talent to be able to support companies like this.”

Donald and Melania Trump arriving in the UK last year. He’s visiting the UK again in June CREDIT: AFP

These buyers are largely coming from New York, LA, San Francisco and Chicago, as well as a few from Houston and Dallas, according to Berkshire Hathaway HomeServices Kay & Co. They’re prepared to pay upwards of £10 million on average, looking in Marylebone, Hyde Park and King’s Cross, and for larger family houses in Mayfair, Belgravia, Hampstead, Notting Hill and St John’s Wood.

It fits in with a general picture of returning health for the high-end market, too. Knight Frank said earlier this month that the number of offers made (not just by Americans) for these pricey properties in the first three months of this year was the highest in more than 10 years. The level of new buyers was also at the highest figure since 2014, when prices were at their peak.

Transactions have increased in prime central London among homes priced under £1m, between £1m and £2m, and over £5m, according to LonRes. It’s the market for homes between £2m and £5m that is suffering the most, where the level of sales continue to fall.

So what’s changed? Political uncertainty remains, albeit in the background. Sky-high stamp duty, which decimated the market four years ago, is still a major factor. It’s a more imperceptible shift of momentum: a mixture of sellers’ increasing realism combined with buyers getting bored of waiting to see what happens with Brexit.

But it’s not all sunshine after the storm in the prime central London market: there’s been a 39 per cent fall in the number of new properties listed in the first three months of the year, compared with the same period in 2018.

That’s proving to be one of the biggest problems for the ultra-rich, as there aren’t enough suitably high-end, ultra luxurious properties to buy.

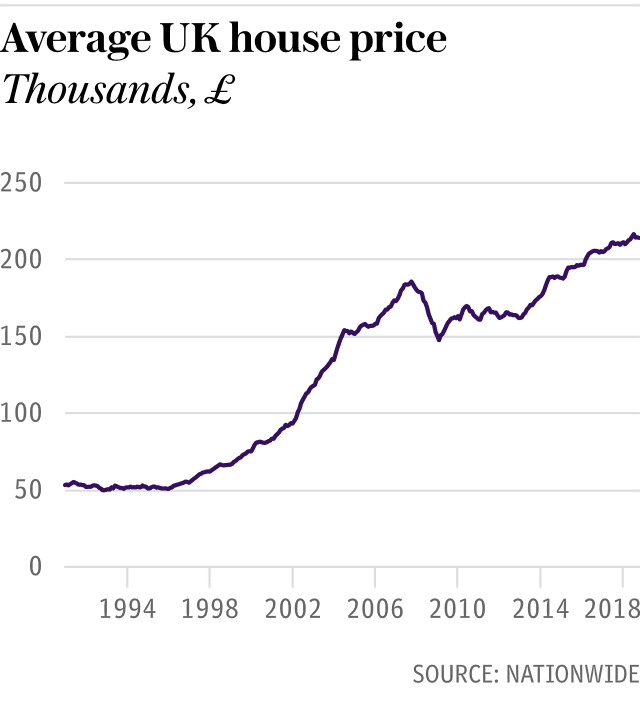

House price growth remained sluggish in February, with prices just 0.4pc higher than the same time last year, according to Nationwide’s latest house price index.

While this is an improvement on the 0.1pc growth in January, prices had been rising by around 2pc last year. The average house price is now £211,304, around £3,000 cheaper than in October.

Robert Gardner, Nationwide’s chief economist, said the subdued activity in the housing market was due to weakened consumer confidence in the face of political and economic uncertainty.

Many sellers and buyers have adopted a “wait-and-see” approach as Britain nears its exit from the European Union next month.

Mr Gardner said, “Measures of consumer confidence weakened around the turn of the year and surveyors reported a further fall in new buyer enquiries over the same period.

“While the number of properties coming onto the market also slowed, this doesn’t appear to have been enough to prevent a modest shift in the balance of demand and supply in favour of buyers in recent months.”

Jonathan Samuels, chief executive of property lender Octane Capital, said the property market was “on its knees”. He added that buyer sentiment had “shattered” despite a strong employment rate, low borrowing rates and below-target inflation.

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said that while the annual growth rate remained well below last year’s February average of 2.1pc, he “doubt[s] it will sink much lower”.

“Brexit uncertainty is prompting some potential home-buyers to delay purchases, but the pick-up in mortgage approvals in January suggests the aggregate impact has been modest so far. The wider economic picture remains supportive of house prices. The unemployment rate is at a 43-year low, wage growth has picked up and mortgage rates remain very low.”

Camilla Dell, managing partner at buying agent Black Brick, argued that Brexit was only “part of the story”. “A big reason why price growth is sluggish is because of tax. The market is struggling with extortionate levels of stamp duty and this is having an effect,” she said.

“We did notice a big pick-up in buyer enquiries in January, which does seem to suggest some pent-up demand coming through which we might see in the next round of data. There are a lot of buyers waiting in the wings who want to buy this year,” she said.

Recently published Government data shows an uptick in the rate of home ownership last year. The Ministry of Housing, Communities & Local Government said the home ownership rate in 2018 rose to 63.5pc, up from 62.6pc in 2017.

Mr Gardner said this was driven by an increase in the number of people owning their own home with a mortgage, which began to increase again last year after declining continuously since 2005.

The number of people owning their own home with a mortgage rose by 5pc over the year to 6.9 million, though this is still 20pc below the peak recorded in 2000.

Choose the right agent, buy new cushions and be available for viewings

By Annabelle Williams and David Byers

It’s only 81 days until we crack open the mince pies and mulled wine, yet it takes an average of 60 days to agree a sale on a property, from the moment it is listed. So if you are you looking to sell your home before Christmas, you better get a move on.

The British property market hardly looks encouraging for people trying to buy or sell. This week’s Nationwide index shows the average British house price rose by a sluggish 2 per cent over the past year to reach an average of £214,922. Yet the market remains full of nuances. Yorkshire and the Humber’s market, for example, rose 5.8 per cent in the third quarter of this year, while the average price in the East Midlands rose 4.8 per cent.

Even those in London, where average house prices dropped 0.7 per cent in the third quarter of 2018 — the fifth consecutive quarterly dip — have reasons to be cheerful.

According to a breakdown in property prices by postcode by Propdex, an analytics company, London’s dip is only affecting a minority of areas — 74 out of 231, mostly in west London — where prices have become too inflated and are undergoing a correction. Meanwhile, the postcode in Britain in which the most homes were sold, is in Croydon (there were 833 sales in six months), proving London’s affordable outer zones are doing fine.

However, according to research by Rightmove, a property portal, you’ll sell faster if your home is in Scotland, with Edinburgh and Glasgow experiencing an unprecedented boom. You can achieve the quickest sale anywhere in Britain in the commuter town of Livingston in west Lothian, which is a magnet for workers; it’s 40 minutes by train to both cities. Here it takes an average of 26 days for a property to be sold after appearing on Rightmove. “We’re in the centre of Scotland, with good commuter links to Edinburgh and Glasgow and we’re very affordable — you can buy an ex-local authority three-bedroom terraced house from £100,000 and a four-bedroom detached house for £300,000,” says Simon Thomas, the owner of Remax, an estate agency in Livingston. This compares favourably with Edinburgh, where flats start at £200,000.

Scottish authorities make up six of the seven fastest-selling areas, and include Glasgow (31 days) and Edinburgh (28). Other notable areas in the top 20 include booming areas of the West and East Midlands, where property prices are rising rapidly. Among these are Coventry (36 days), Rugby (36), Corby (37), Kettering (37), Redditch (38) and Bromsgrove (39). In London the fastest-moving areas are the most affordable — sales in Forest Gate in Newham, east London, are agreed after an average of 43 days — and those where middle-class families snap up properties nearest the best schools, such as Whetstone in the borough of Barnet (58 days’ selling time).

If you are struggling to sell your home, we have asked the experts for their tips on how to get your place sold.

This six-bedroom house in Buckland Newton, Dorchester, is on sale for £2.25 million with Knight Frank.

Price

Caspar Harvard-Walls, a partner at Black Brick, a buying agency, says sellers need to be “extremely realistic” about the price their property will fetch. “It’s a buyer’s market,” he says. “The most important thing you can do is ensure it is priced sensibly, otherwise you are just wasting time.” He advises sellers avoid relying on estate agent estimates — after all, they are trying to win your instruction. Think about whether your asking price reflects the market conditions. Look at sales of comparable properties online, and if those sales were a while ago, consider deducting something from the price.

Prepare for a quick sale

Thea Carroll, a senior buying consultant at the Buying Solution, a buying agency, says sellers who are serious about shifting their property before the end of the year should make arrangements to rent somewhere. Be clear with buyers that you’re prepared to move. “The worst thing you can do is be ambivalent with buyers. Give the buyer an element of security about how you will move your family out of your home, and tell them you are keen to exchange and complete before Christmas.”

Carroll says that this could also be a good bargaining chip when it comes to your property’s sale price. “Tell buyers the reason you are not being weak on pricing is because you are being flexible with your moving date,” she says.

Mark Hayward of NAEA Propertymark, a professional body for estate agents, says: “Instruct your solicitor to prepare contracts and seek answers to preliminary inquiries, so when a buyer is found there won’t be any delays. If your house has been extended, obtain copies of planning consents and building regulations.”

In Barnes, southwest London, this house with three bedrooms is on sale for £3.2 million with Marsh & Parsons.

Choose your agent carefully

How did you choose your agent? Was it based on its fee, because it is the best-known in the area, or its expertise in selling homes like yours? “We see people who are selling with completely the wrong agency. The days have gone when you could instruct an agency and wait. The seller has to become far more involved in the process,” says Harvard-Walls.

Carroll says the autumn may be time to appoint another agency. “Properties go stale in the run-up to Christmas. If an agency has had your property all summer I would ask to see their viewing numbers, and if you are only getting one or two a week, appoint another agency and negotiate a lower fee.”

Harvard-Walls advises people to ask prospective agencies to show them examples of similar homes that have been sold and choose an agency that frequently sells properties in your segment of the market.

Look at the agency’s marketing material for your property. If the photos of your home show spring flowers and sunny skies, have some autumnal photos taken.

This house in Holland Park, west London, has five bedrooms and is on sale for £8.25 million through Marsh & Parson

Presentation

“Towards the end of the year, with Hallowe’en and bonfire night, the chintz and decorations start to appear. Try to keep the family home neutral and clear of tatt,” Carroll says.

Regularly ask your agency for feedback from viewings and act on what prospective buyers are saying. Harvard-Walls says he knew of one seller who was told by prospective buyers that the garden was a selling point, but not in its present state. The seller spent £5,000 doing up the garden and shortly afterwards secured a sale.

Mhairi Coyle, a designer at Mhairi Coyle Interiors, says that sellers should wash windows, internal and external paintwork, and touch up any nicks on skirting boards and walls. Consider refreshing your interiors with modern bedspreads, curtains and hide old-fashioned sofas with throws.

Coyle says: “There are inexpensive things to choose from everywhere now. The market has changed drastically, you never used to be able to get anything stylish in cheaper shops.” She recommends people look at H&M, French Connection and Habitat for affordable furnishings.

Consider moving some furniture into storage. Coyle says: “More houses would sell if they had a couple of pieces of furniture in each room. The less stuff you have, the easier it is for people to see themselves in the space.”

Coyle also worked with a couple who bought new cupboard doors for their kitchen in a makeover aimed at selling their home. “They didn’t want to redo the kitchen, but they needed to refresh it.” She recommends companies such as Naked Doors, or Superfront if you have Ikea furniture that needs a stylish overhaul.

Be available

Harvard-Walls says he has had sellers make things tricky for people to view their home. Even if you have endured many months of viewings, try to be flexible. “You have to work with your agent to make your home available at short notice and outside working hours,” he says.

With the “improve, don’t move” mantra ringing in their ears – sometimes fuelled by a reluctance to pay the huge stamp duty bill involved in upsizing to a bigger house – many homeowners are finding a new way to extend. They’re buying next door.

In certain situations, it can make perfect sense. You love your house and the location, but you need more space, perhaps because of boomerang children or grandparents moving in, or some other millennial or multi-generational arrangement. You’ve probably already extended into the loft, out the back and maybe even underground. So should the chance arise to extend into next door too, why wouldn’t you do it?

There’s still stamp duty to pay, of course, but it will most likely be a lesser sum to buy a neighbouring property of similar size to your own than it would to upgrade to a far bigger house (even taking the three per cent surcharge for second homes into account). “There will be the costs of architects, builders and solicitors too, but it will still represent a considerable saving on the usual costs of selling a home and buying a bigger one,” says Sara Ransom of buying agent Stacks Property Search.

There may even be some financial gain in buying next door. “I encourage my clients to do so at every opportunity, where their financial position allows,” says Marc Schneiderman, of estate agency Arlington Residential. Even when the space isn’t needed immediately, he is looking long term at the investment value of having a handily located spare property to rent out, to eventually sell as a project for someone else to convert, or use some of next door’s garden to add to your own. “You may only get the opportunity once to buy next door, so when it does become available, consider it very closely,” he says.

Making a huge profit is rarely the motivating factor behind such projects, as the whole may not be worth more than the sum of its parts. Two adjoining cottages were recently available in Devon’s Culm Valley for a joint price of £695,000 through Greenslade Taylor Hunt. “If they were sold separately, would they be worth more than £350,000 each? Probably,” says Gideon Sumption of Stacks. “It rarely makes financial sense to join two properties, unless there is some marriage value to be released, such as restoring a shared drive to single ownership, or even getting rid of an unpleasant neighbour.”

Three Cotswold cottages which can be knocked together, on the market through Strutt & Parker.

For most people who carry out this kind of conversion, it’s all about the lifestyle or emotional benefits. It attracts buyers across the entire property spectrum, from small country cottages to huge central London apartments. “If it enhances your quality of life, forget about the end value and go for it, and you may well make an unintentional stamp duty saving,” says Sumption.

At the priciest end of the knock-through spectrum, there’s Trevor Square in Kensington, Harrods’ former Grade I listed depository. Nick and Christian Candy, the developers, briefly lived in the building and in 2006 turned four of the apartments into one vast, six-bedroom duplex that spans 6,400 sq ft and is now on sale for £30 million through Harrods Estates. “Buyers in this market want purpose-built lateral living with a 24/7 concierge and parking, and this ginormous property comes with four large, secure parking spaces,” says Shaun Drummond, sales director of Harrods Estates.

The huge duplex made from four apartments on Trevor Square, £30 million through Harrods Estates

In some London boroughs – Kensington and Chelsea, and Westminster are the notable ones – reducing the housing stock by knocking two into one goes against their targets to increase supply of new homes, so owners are now unlikely to be granted permission. “Even where a house has a mews behind, if it has been two separate households paying two lots of council tax, it will be a challenge to secure planning,” says Brendan Roberts, director at Aylesford International.

Apartments can lend themselves more readily to this kind of redevelopment, either by creating a duplex by knocking into the flat above or below, or by knocking into the flat next door, in a mansion block for example – provided you have the consent of the freeholder/landlord and the local council. “You would also need to amalgamate the leases, which is potentially complicated,” says Simon Tollit, co-founder and director of Tedworth Property.

In some London boroughs, reducing the housing stock by knocking two into one goes against their targets to increase supply of new homes, so owners are now unlikely to be granted permission

In the most expensive areas of London, “double laterals” are also popular, says David Lee, head of sales at Pastor Real Estate. That’s where two adjoining flats span two buildings, satisfying wealthy buyers’ tastes for large, lateral space that maximises light and eliminates staircases and corridors that waste room.

“Some excellent examples can be found in South Kensington, where a number of stucco-fronted period buildings have been brought together to form exceptionally wide residences, particularly those located on first floors, which tend to have the highest ceilings and grandest proportions,” adds Lee.

At the opposite end of the spectrum, there are rural opportunities crying out to be restored into one. Occasionally, you will find an entire row of two-up, two-down farmworkers’ cottages up for sale, says Bruce King, director at Cheffins estate agency in Cambridge. “The properties that work best in this situation are not high value so even when you factor in the buying and conversion costs, it can be cheaper than buying one property,” he says. “They don’t come up very often, so keep an eye on property auctions and private treaty sales, or ask local farmers and landowners.”

Nicholas and Jill Leader’s house in Canterbury, £599,950 with Strutt & Parker

Martin Walshe, of Cheffins, expects demand for knock-throughs to rise in central Cambridge, too, where city centre stock is an issue. He mentions a current example on the market: two neighbouring Victorian terraced houses in Romsey Town, priced at £550,000 for the three-bedroom, and £400,000 for the two-bedroom. Both are owned by the same couple, who live in one and rent out the other.

Walshe suggests knocking through the two would cost £100,000, including enclosing the driveway that links them with a modern, glass walkway. “It works best in city centre homes when the houses need complete modernisation and can be picked up at lower prices, reconfigured and then sold at a premium,” he adds.

Nicholas and Jill Leader’s house in Canterbury, £599,950 with Strutt & Parker.

One issue to avoid is creating a super-sized house whose value is out of proportion with what’s around it – as Jamie Oliver discovered. He spent millions conjoining two Primrose Hill properties into one, which failed to sell a few years ago. He then had to reinstate it as two separate houses.

It’s the “best house in the street” syndrome that no one really wants, says Camilla Dell, managing partner at Black Brick buying agency, which sources prime London property. “If you knock two houses together on a street where the average house price is £3 million, it’s unlikely a buyer with £6 million will want to buy there. They will choose a better street. The key is to consider the surrounding area and work within the confines of the market,” she says.

It can be a lot of hassle reconfiguring two properties from scratch, including getting rid of surplus staircases and kitchens

It’s also a lot of hassle reconfiguring two properties from scratch, including getting rid of surplus staircases and kitchens. But without re-designing the newly combined property, you may end up with odd and compromised space. “In London, especially, integrating two houses is usually reserved for those with deep pockets and plenty of time,” says Tollit.

Sometimes, however, knocking through is really quite simple. In Canterbury, Kent, within close range of the famous cathedral’s spires, retired teachers Nicholas and Jill Leader seized the opportunity to knock through and create their dream home when their neighbours announced they were selling up.

“We were looking for a four-bedroom house within the city walls and couldn’t find anything. We had often been to our neighbour’s house for drinks and thought about how great it would be to knock these two mirror image properties into one,” says Nicholas, 80.

Two houses in Cambridge, which can be knocked together, on the market with Cheffins.

Built in 1739, their original house had just a downstairs living room and small scullery, with a spiral staircase leading to one bedroom and a reduced-height attic. Their current two-in-one home – which is now on the market for £599,500 through Strutt & Parker – provides the four bedrooms they were looking for, and a large kitchen extension at the back, in place of the previous two small kitchens.

They spent about £60,000 on the conversion, filled 16 skips with rubbish, had to rewire the house completely and replumb, with the added complication of the property being in a conservation area. “The archaeological society was keen to jump down any hole we created,” adds Nicholas.

One pleasant surprise awaited them, however, when they knocked through; they found an 18th-century time capsule buried in a wall, containing a ha’penny and some toys, including a leather ball and hoop. “We replaced the capsule with some items including a letter saying we hoped whoever found it was as happy in the house as we have been,” says Nicholas.

“I still feel the sense of the two old houses. I climb the spiral staircase in No. 13 and walk along the corridor in No. 14. But it just feels like one adorable house now.”

London has become a popular place for the wealth to divorceCredit: Peter MacDiarmid

By Rhiannon Curry

Estate agency Black Brick has launched a specialist service to cater for divorcing couples as an increasing number of the super-rich seek to untie the knot in London.

It also advises clients on what it costs to run a home in a particular area so they can use the information as part of a claim against their spouse, and finds short-term accommodation for those going through the divorce process.

London has become increasingly popular location for those looking to instigate divorce proceedings because of the more generous terms that can be negotiated for the financially weaker spouse. Unlike in other countries, property owned before the marriage and wealth that has been inherited can be included in a potential settlement, resulting in higher payouts.

Black Brick said such is the demand from wealthy individuals looking to value properties for the purposes of a divorce that the new division is needed to provide information to courts. In 2017, around 10pc of the transactions conducted by Black Brick were for people getting divorced.

The proliferation of high-value divorces has spawned its own industry elsewhere: personal security company Umbra International has also reported a marked rise in the number of individuals, particularly women, seeking protection from bodyguards or cyber security experts before, during and after divorces.

Meanwhile, Swiss private bank Julius Baer has also begun offering a service that allows clients can borrow money in order to fund a divorce process if their cash is tied up in jointly-owned assets such as property.

She said she needed £39.3m to purchase a home in England as a result of the marriage breakdown, as well as £27.9m to buy a property abroad. She claimed she needed £5.4m a year to live on.

When the Norman Foster-designed HSBC building in Hong Kong was completed in December 1985, it was the most expensive building in the world ever to have been constructed.

While designed – much like earlier colonial-era structures on the island – with a trained feng shui geomancer, it did not anticipate the arrival, just a few years later, of the Bank of China building, with its knife-like edges, next door.

Shortly after it was built, the governor of Hong Kong died and there was a downturn in the city’s economy; it didn’t take long for fingers to be pointed at the new building. Feng shui masters were consulted and two cannon-shaped structures were mounted on the roof of HSBC’s building to dispel incoming negative energy from its neighbour.

Such is the power of the ancient practice of aligning buildings and objects, in order to attract good luck and ward off misfortune, that entire apartment buildings in Hong Kong have been built with holes through the middle. This is to allow dragons – traditional symbols of wealth and prosperity – to reach the harbour. Blocking the dragons’ path is thought to bring bad luck to residents.

While this may be a step too far for London developers, many are all too aware of its importance, and factor in a feng shui consultant if they wish to attract the lucrative Chinese market.

That means changing addresses if they feature the number four, which is considered inauspicious in China because it sounds similar to the words for “death”. Property developer Ballymore also commissioned a feng shui audit report for its Embassy Gardens project at Nine Elms in south London. The number eight is lucky, and Chinese buyers will often make offers on apartments with eight in the number or floor, explains Merlin Dormer, of buying agent Heaton & Partners.

“We also receive offers with eights in them from Chinese buyers,” adds Bertie Hare, from Strutt & Parker’s Knightsbridge office. “On the seller side, someone might decline a higher offer like £900,000 if a lower offer includes more lucky numbers, like £888,888.”

Mayfair and Marylebone-based agent Martin Kay, of Kay & Co, says that Chinese clients looking at high-end property will sometimes bring their feng shui consultant with them on viewings. “It’s nerve-racking as it can end a deal immediately if something’s not right, particularly if one of the couple is more superstitious than the other.”

In one example, an enterprising (and not superstitious) wife managed to persuade her husband to buy a flat on the edge of Regent’s Park by convincing him it was on the fifth floor rather than the fourth. “She just counted from the ground floor up instead,” says Kay.

These days in London, feng shui requirements compete with another Eastern system of beliefs, vastu shastra, which is important to some Indian buyers, says Camilla Dell, of Black Brick, a buying agent. “One of the main requirements of vastu is that the front door should face south, which, in theory, sounds relatively simple but in London it can rule out whole parts of the city where the streets simply face the wrong way.”

Earlier this year, developer One Point Six took the unusual step of designing a luxury apartment on Pont Street in Knightsbridge according to vastu shastra before putting it on the market. While this remains a niche approach, agents have to find other solutions to remedy such concerns.

For one of Dell’s clients buying in a new development, this involved purchasing two flats opposite each other as well as the corridor space in between. By linking them together they were able to create a south-facing front door and the deal went ahead.

“With off-plan developments, we can try and find a way around these problems. But with some Indian clients, it’s likely that their vastu consultant will be the first to see the floor plans,” says Dell. “If something’s not right, the property is simply ruled out before anyone has been to take a look.”

Astrological concerns have also been known to delay a sale. “I was bidding on a property for a client, and we were all ready to exchange when she called a temporary halt because the planet Mercury was moving in the wrong direction,” says Guy Meacock, of Prime Purchase.

“While the planet was in retrograde she was of the belief that she shouldn’t sign the contract. I had to tell the selling agent we’d need to wait until it started moving in the right direction, which took several weeks.”

As international buyers increasingly enter the top end of the country house market, concerns regarding feng shui are having an impact here, too, says Rupert Sweeting, head of country house sales for Knight Frank.

“Many Chinese buyers hate having a well in a house. So if a rural property has its own well in the grounds, they often won’t progress to offer stage,” he explains.

Buyers who believe in the paranormal can also affect how successful a viewing is, adds Sweeting. If there’s any hint of a problem, his advice to vendors is to get the house cleared of any such ghouls by “employing a ‘ghostbuster’ or a priest to exorcise the house”.

Salisbury-based solicitor Marcus Thorpe, of Trethowans, says it’s important to be honest about any activity in the house. “While questions about the paranormal don’t form part of the standard buyer’s questionnaire, and perhaps it’s unique to the country house sector, a good solicitor might ask the question.”

For astrologer Shelley von Strunckel, who writes horoscopes in The Sunday Times and London Evening Standard, interest in the “mystical” is increasing. “There’s a big buzz about it now and a growing interest in the more subtle elements in life.”

Concern regarding the alignment of buildings is not a new concept on British shores, as demonstrated by Stonehenge. According to von Strunckel, even the least mindful buyer of a property will be aware of the energy of a place when they walk into it – they just might not know how to articulate it.

“As an astrologer, we talk about cycles. For a long time, we’ve been in one that’s been very focused on the intellectual – what you can see and measure – to the exclusion of the internal and reflective. That’s beginning to change,” she says.

The energy of previous owners of a property can remain in the walls, she believes; in the case of a new build development, even that of the builders can be present long after they have finished.

Would-be buyers should, according to von Strunckel, stop and think about what they feel during a viewing, without being embarrassed.

Can negative energy immediately stop a sale? Not necessarily. “Regardless of any religious belief, you can always ask someone to come and clear the energy or bless the space,” says von Strunckel. “If in every other way the property works, it’s a lot easier to do that than fix physical problems like replacing small windows or bringing light into eternally dark rooms.”

Von Strunckel is hoping to leave some of her positive energy in her loft apartment in King’s Cross, north London, which is on the market for £2.85 million through Currell.

Bought nine years ago, the three-bedroom converted warehouse flat is flooded with light by its huge windows. It overlooks Battlebridge Basin and Regent’s Canal and comes with access to a 24-hour concierge.

“You get great views from here,” she says. “St Paul’s and the Shard in one direction, the London Eye in another and the arches of St Pancras to another,” explains von Strunckel. “It’s just time for me to move on. I’ll take my energy with me but hopefully some will be left for the new owners.”

Indian buyers are pouring into central London’s lethargic high-end property market after a change to how much money they can take out of their home country.

Buying agency Black Brick said that 13pc of sales it has done this year have been to Indian buyers, up from 2.6pc in 2015/16.

Separate research by Cluttons found that between August 2016 and July 2017, Indian buyers accounted for 22pc of the sales in prime central London, made up of the City of Westminster and Kensington and Chelsea, up from 5pc in 2012.

This is partly due to changes in the Reserve Bank of India’s regulations of how much money can be taken out of the country. The so-called liberal remittance scheme was adjusted in 2015, meaning that a family of four can take out $1m, while previously it was only $400,000. Camilla Dell, managing partner at Black Brick, said: “It means that a family of four, after one year, will have $1m to spend, and after two years $2m. It quickly adds up, and explains why a lot of our Indian clients are buying in the £1m to £2m range.”

Property in central London is very attractive to foreign buyers as prices have been falling due to an oversupply of luxury flats and affordability issues. Prices of these luxury homes are 15pc lower than in September 2014, according to Savills. Coupled with the fall in sterling, some international buyers can buy homes for less than they could two years ago.

Black Brick’s Indian clients are split between investors, who largely want to buy new build flats in Shoreditch and White City, and owner-occupiers looking in Mayfair.

Becky Fatemi, managing director of estate agency Rokstone, agreed: “The most popular address for Indian buyers is Mayfair – where the most sought after addresses are Grosvenor Square, South Audley Street and Hill Street. The other alternatives for them are St James’s and Belgravia.” Ms Dell added that she is currently working with a Bollywood actress to buy a London home in Marylebone, Knightsbridge or Mayfair.

According to Black Brick, other big international buyers include those from the Middle East, France, Nigeria and Russia.

By Isabelle Fraser