Property magnates the Reuben Brothers are investing £1bn to move the dial in Mayfair. Can they succeed?

By Caroline Roux

To turn off Piccadilly and into White Horse Street in London’s Mayfair is to enter a different world. The first is a traffic artery lined with Tube station entrances, swish hotels and flashy car showrooms, where distracted tourists bump into polite couples heading to the Royal Academy of Arts. The second is a winding lane, its tiny shops — a dry-cleaner, a wine bar — quaint finds. But forgotten it is not.

On a sunny Friday in June, the latter’s slender pavement is busy with workmen communicating in all the languages of Europe, moving between a series of projects taking shape in the 1.3 acres of prestige land known as the Piccadilly Estate. This is the land of the Reuben Brothers.

The family is investing £1bn in this small, upmarket slice of London — creating apartments, a members’ club, a hotel and public realm. The project is coming to fruition at the very moment when its foreseen customers might be rather less available, thanks to the ending of non-dom status, and changes in taxation and stamp duty have hit the wealthy hard (for overseas buyers, stamp duty on property purchases can push north of 17 per cent). In the year to May 2025, the number of prime property sales above £5mn in London was 14 per cent lower than in the previous 12 months. The question “can they pull it off?” looms large.

The Reuben family, with a fortune of £26.87 billion, is Britain’s second richest, squeezed between the Hindujas at number one and Sir Len Blavatnik at number three. Iraqi Jews born in India, brothers David and Simon came to London in the 1950s and, from dealing in carpets and scrap metal and making their fortune in aluminium in the post-Soviet “wild east”, expanded into property and many other businesses besides.

The brothers, now well into their eighties, are known for watching and waiting, swooping in when the going gets tough for their competitors, with their ability to put cash on the table. It has secured them some significant gains in London, New York — and beyond. In 2015, they purchased the combined debt of the Plaza Hotel and the Dream Downtown hotel in New York, and Grosvenor House in London, after its owner Subrata Roy of Sahara Group was arrested and bail set at $1.6bn for its non-payment. It cost them $850mn. In 2020, they pounced again, this time on the Surrey Hotel, a star of the Upper East Side’s Golden Triangle, for $150mn cash ($65mn below asking price) when the owner failed to pay the rent. Investments in the US property market over the past seven years total more than $6bn.

It was in 2011 that they snapped up the Piccadilly Estate for £130mn, at a £20mn discount, from beleaguered businessman Simon Halabi. “It included the In and Out Club, 100 Piccadilly, some of the buildings behind that, and some in Shepherd Market, including the members’ club 5 Hertford Street,” says David’s youngest son Jamie, reeling off a list of landmarks. The first, known by its loud lettering out front, is soon to become a hotel and residences, and return to its original name Cambridge House. It is set to open early next year.

“My uncle has assembled the rest with patience, bit by bit,” continues Reuben. “We had the idea to establish a chic new quarter — cool, upmarket, authentic.” He pauses on the last word. “You don’t always get that around here.” He has a point — Mayfair is increasingly a district of division, where old-school elegance and charm rubs up against some fairly brash new clubs and restaurants.

Yet, according to buying agent Camilla Dell, founder of Black Brick Property Solutions, nowhere is more location, location, location than this part of town. “We would consider prime Mayfair to be Grosvenor Square, Mount Street, bits of Davies Street,” she says. “Off-patch” properties are a harder sell. And there are already a number of new-builds that have had properties on the market for a while, including 60 Curzon, on the north border of Shepherd Market, and One Mayfair, a development on Audley Square by British billionaire John Caudwell, where apartments begin at the £35mn mark.

Can the Reubens magic a newly meaningful part of Mayfair into being?

Americans are coming big time, the dollar is good. They love London and they buy in totally to the culture here.

I meet Reuben at One Carrington, a Reuben-built block of 28 apartments reached down a cobbled cul-de-sac off Shepherd Street. The red brick building, by London firm AHMM, fits politely between the existing 19th- and 20th-century buildings on what was once an NCP car park. Its generous square windows overlook a plant-filled courtyard by landscape architect Robert Myers. “The concept was for something that feels domestic, and small-scale,” says Reuben. “It’s about discreet living, not huge-scale apartments.”

Prices at One Carrington are around £3,000-£5,500 per square foot; one-bedrooms from £2.95mn up to four-bedrooms from £12.95mn. What Dell calls “around the corner” are 1 and 20 Grosvenor Square, converted into homes in the latter 2010s where prices are a heady £6,500-£7,500 per sq ft (local less-illustrious second-hand stock sits at the £2,500-£3,000 mark).

One Carrington might not have 1 Grosvenor’s supersonic allure, but it does offer membership to the Carrington Club across the road for business, fun and wellness — to be run by 5 Hertford’s Robin Birley. In Mayfair terms, these are entry-level properties, in a boutique building. “Hanover Square sold really well,” says Dell of the apartments that form part of the Mandarin Oriental, which opened there a year ago. “Because they were on for £3mn-£6mn.”

Tom Rundall, a partner at Knight Frank, which is selling the apartments at One Carrington, delicately spins the tough sales environment as he shows me around it. “London is a buying opportunity,” he says. “We’re more flexible around price than we were in 2014,” he continues, referring to the decade-old bubble. “We’ve had 30 viewings in the past week — Americans, Europeans and those from the Middle East. The sub-penthouse has sold. A two-bed has been bought by two Canadian brothers for their families to use.”

Jamie Reuben, who is 38, joined the family firm in 2018. Previously, he had started an emerging market hedge fund and some rumours point to him having had a place at Conservative HQ under Boris Johnson. (He denies this, but is a known Tory-party donor, purported to have given at least £750,000.)

Today he is dressed in a blue suit, white shirt and brilliant white trainers — all by Thom Sweeney, a men’s outfitters in Old Burlington Street in which he is an investor. “We have a racing business, Arena Racing, the largest racecourse business in the country,” he says, of other family assets. “Airports, Newcastle United football club . . . we’re not just niche real-estate developers.” He is very keen on Newcastle, both team and city — a United flag hangs in the lobby of the reopened art deco Surrey in New York.

Less playboy and more family and work-oriented than your average super-solvent thirtysomething, Reuben shifts between London, where he lives in Marylebone, and New York, where he has a place in NoHo. (His brother and sister, David Jr (45) and Jordana (46) are currently in Los Angeles developing the hell out of six acres of Century Plaza into residential and retail.) At weekends, he plays padel, the new sport of, if not kings, the high achiever.

The same year he joined the company, the family bought Mayfair’s Burlington Arcade — constructed as a safe shopping street for jewellery and fancy items in 1819, and still fulfilling a similar function. They paid £300mn, according to Trupti Shah, also 38, who looks after retail at Reuben Brothers. She has worked closely with Reuben, and together they have breathed new life into the arcade. “After Covid, we had six empty shops and then 11,” says Shah. “But the Reubens wanted me to wait for the right takers. I persuaded Borsalino — the Italian hat makers — to come in after a year-long negotiation.” It is a sign of its success that even Stephen Webster, the A-list jeweller, has moved there from Mount Street.

“I think, if I have a passion, it’s for restoring these important old buildings and streets,” says Reuben. “They are integral to the city and its history.” Another project, the conversion of Admiralty Arch, at the Trafalgar Square end of The Mall, into a Waldorf Astoria hotel, is also under way. “There will be a restaurant by Daniel Boulud on the roof,” says Reuben. “We will have views like no other.”

With masterful optimism, he talks up London’s continued viability. “Covid was tough, and post-Covid,” he says. “And the focus since has been on the cost of living. But we shouldn’t ignore the wealth traders, the foreign investors, the entrepreneurs, and all the visitors. They bring a lot culturally but also financially. We need to make them feel welcome here.”

“We’ve been quite successful in the UK over the years in offering good incentives, tax credits,” he adds. There might be a non-dom exit, but “Americans are coming big time, the dollar is good. They love [London] and they buy in totally to the culture here. All cities go through ebbs and flows.”

Shepherd Market, a stone’s throw from One Carrington, dates back to 1735. Reuben Brothers are part-financing pedestrianisation of the public realm areas with Westminster Council, upping the appeal of its few interconnected streets by adding new bijou, independent offerings to the old favourites like the L’Artiste Musclé, established in 1971 and a favourite of Apple Records as a party venue.

“We’re not going to spoil it with chains,” says Shah, who lives here. “We could do with a florist.” Cars can’t park after midday, making outdoor dining one of its assets. “I would have to talk most of my buyers into viewing One Carrington,” says Dell. “But these improvements at ground level will help.”

The Reubens don’t like publicity. David and Simon are practically invisible. At the launch of the Surrey, last October, Jamie gave a single interview. Our meeting today will be his only one in London. It is perhaps why he can’t resist the short walk to Cambridge House. The 1756 building, designed by Matthew Brettingham in the Palladian style for the Wyndham family, is Grade I listed. Its development into a 102 room hotel and seven residences has been a long affair. “It feels like we’ve been working on it for 250 years,” he says.

The restoration is detailed and extreme. It had been occupied by the Naval and Military Club until it sold to Simon Halabi in 1996. “It was a wreck, they’d been patching it up for years,” says Reuben. Twenty original marble fireplaces are currently with experts in the Thames Valley. And each has an overmantel mirror, dating back to the 1750s. “They take a year each to restore,” says site manager Paul Storey. Moulds are being made of original plasterwork. Walls are recreated in lath and plaster. And when the 24-metre-deep basement was excavated, a Thames sewer had to be diverted and then put back in place.

Reuben is entranced. “Peek up, you can see the ceiling being restored,” he says, pointing to sky-blue paintwork and delicate curls of white plaster. “As British people, we don’t always recognise how great London is, and what it’s got. I like to think that we’re making the best of it.”

Sellers stuck in denial are forced to accept the days of property price highs are over

By Alexandra Goss

Two houses were recently put on the market for £15m, one in Cornwall, the other in West Sussex. They were luxurious and sprawling, but they definitely weren’t worth that much.

“These were exceptional properties but their owners, aided and abetted by estate agents fighting for listings, had simply misread the market;’ says Philip Harvey, of the buying agency, Property Vision. His clients paid £10.5m and £9.5m respectively for them.

“We are now in a totally fragmented market, with the very best of the best remaining firm, and the overnriced and comnromisedfailing to sell!’

Price reductions are happening across the country. Hamptons estate agency says almost half of the properties that sold in April had been reduced, while separate data from the property portal Zoopla reveals that homes nationally are selling for an average of

£16,000 below the asking_nrice, equal to 3pc.

At the very top of the market, cuts of millions of pounds are not uncommon, such as with Harvey’s £5.5m discount.

“Asking prices are often quite out of sync with reality;’ says Adrian Anderson, of the high-end mortgage broker, Anderson Harris.

“Some owners are still expecting to get the prices they could have got during the ‘hot’ Covid market. Many sellers also don’t have to sell. So if someone comes along and pays what they want, they’ll take the offer. Otherwise, they’ll just stay put:’

Consumer confidence is shaky against a weak economic background, and affordability is stretched due to historically high mortgage rates. There is also a stark imbalance between supply and demand.

The property portal Rightmove says the number of homes for sale is the highest in a decade, while figures from Knight Frank estate agency show that its new UK sales instructions are currently about a fifth higher than the five-year average (excluding 2020), while the number of new prospective buyers is a fifth lower.

“Buyers are able to take their time at the moment because they have so much to choose from;’ said Andrew Groocock, of Knight Frank.

London squeeze

The most expensive region for housing is also recording more reductions.

In research for The Telegraph, Zoopla has looked at the areas with the highest percentage of homes for sale that have been reduced by at least 5pc in the past three months and found that central London’s WC postcode tops the table, with 18.6pc of properties on the market there seeing a price cut. The SW, EC, SE and W postcodes in the capital also feature in the top 10.

Discounts are biggest on the priciest homes. Of the homes in central London valued at between £Im and £10m that sold in the first three months of the year, 82pc went for less than the asking price, according to separate data from Coutts.

The bank adds that the level of discounting has reached a five-year high, with an average reduction of 9.3pc across Prime London in the first quarter of 2025, rising to 15pc in Mayfair and St James’s.

Tom Kain, of the buying agency Black Brick, says: “We have not paid full price for a property for a while. After a long period of denial, vendors have finally accepted that their properties are no longer worth what they might have sold for at the height of the pandemic:’

London houses that need updating are recording some of the biggest discounts, says Lulu Egerton, of Strutt & Parker estate agency in Chelsea. She is selling a pretty three-bedroom house on Pavilion Road that was put on sale almost a year ago with another agent at £6.95m. Egerton is now marketing it at £4.55m, a reduction of more than a third.

“This house was remodelled 10 years ago and now, because the costs and time taken for a refurbishment have spiralled, buyers would rather pay more for something that’s done up;’ Egerton says. “Unlike flats, where buyers come and go more frequently, people purchase houses for the longer term. This means properties often come to the market in a less good condition:’

Egerton adds that there is no shortage of people who want to live centrally in London.

“However, they’re saying that it’s less about buying the cheap thing than the right thing;’ she explains. “Some properties we are showing [to prospective buyers] 80, 90 or even 100 times:’

There’s a glut of flats currently for sale in expensive areas such as Chelsea, South Kensington and Notting Hill, according to Sara Ransom, of Stacks Property Search.

“There is a huge amount of property being offloaded by investors. It makes very little sense to be a private landlord in a climate where the responsibilities are becoming more onerous, maintenance costs are rising, and it’s hard to see any capital growth in the near future;’ she says.

“Non-doms are wanting to get their money out of the country too:’

Southern discomfort

Price cuts are most prevalent across southern England. Property data company, TwentyCi, says 4lpc of listings in the South East have undergone at least one price reduction, higher than the 37pc average for the UK.

According to Zoopla’s analysis, the BN postcode, covering Brighton and Hove, has recorded the second-highest levels of discounting nationally, with 13.6pc of properties on sale reduced by at least 5pc.

Also in the top 20 are the Canterbury (CT) and Rochester (ME) postcodes in Kent, and the Guildford (GU) postcode in Surrey.

Richard Donnell, of Zoopla, says: “The housing market in southern England is where house price inflation is lowest and currently stands at less than lpc a year. There is demand for homes, but buyers are price-sensitive given higher mortgage rates:’

In the east of England, Norwich properties are also being widely reduced, with 12.3pc having their price cut by at least 5pc.

Polly Hughes, of Savills estate agency, says: “Properties that are realistically priced from the outset continue to perform well, with some even generating multiple offers and achieving sales above the guide price.

“However, many properties priced optimistically in Norwich are struggling to attract viewings. Effective price reductions are in the region of 7pc to lOpc;’

‘Bargains’ aren’t always what they seem

The desire to get a good deal is even stronger in a buyers’ market, but just because something has been reduced, doesn’t mean it’s a bargain – as you could still be paying too much.

Jo Eccles, of the buying agency, Eccord, says that, in many cases, asking prices are being set deliberately high to factor in room for negotiation. “However, buyers need to be aware that, even if they secure what appears to be a good discount, they may still be overpaying substantially.”

She tells the story of a buyer who negotiated £lm off the £10m price of a house in south west London. “He’s delighted with the discount, but the property needs a lot of work and, in reality, isn’t worth more than £Sm;’ Eccles says.

“In a muddled market like this, it’s very easy to overpay. Opportunities are certainly there, but buyers need to tread carefully, do their pricing due diligence and take realistic account of refurbishment costs:’

The price must be right

If you’re selling your home, setting a realistic asking price is crucial.

Robin Chalk, of Anderson Rose estate agency in London, says: “Properties get the most exposure at launch, so it is all the more important to go to the market at a price that prompts immediate interest:’

If sellers price too high to start with and then reduce, it can take over two months longer to find a buyer, according to Colleen Babcock, of Rightmove.

“Our data also shows there has been a 32pc increase in the number of sellers who have swapped estate agent to try to find a buyer;’ Babcock explains. “This reflects the high market competition, and the frustration of some owners that their homes aren’t selling, a process made much harder by setting an over-optimistic price to begin with:’

Indeed, some estate agents are over-valuing properties by up to 25pcjust to win the sales instruction, claims Jess Simpson, of the rural agency Stoneacre Advisors.

“It takes a very long time to manage and modify sellers’ price expectations after that;’ she says. “No one wins when the property is over-valued:’

Yet this may mean facing the uncomfortable truth of selling at a loss. Average Prices in Prime central London have dropped 19pc over the last decade, Knight Frank’s figures show, due to factors such as higher taxes and successive bouts of political uncertainty.

The estate agency says average prices in the “country”, which covers a range of urban and rural markets above £750,000 outside London, are 8pc down from their peak in 2022, when mortgage rates were under 2pc and the race for space was in full swing.

“As the well-worn disclaimer goes: ‘The value of your investment may go down as well as up’;’ Harvey says. “And money spent definitely doesn’t equal a commensurate increase in value:’

A cut above the rest

Reductions can work successfully to sell a home – as demonstrated by a recent sale by Harry Chennells, of Chef-fins estate agency in Cambridge. The house was initially listed at £525,000, reduced after a month to £495,000.

“This shift sparked renewed activity and, following a round of competitive bidding, it ultimately sold for £530,000;’ Chennells says.

If your home isn’t selling, you need to make enough of a reduction to capture the attention of new buyers, says Graham Lawes, of JLL Residential.

“Of course, this will often be proportional to the value of the home, but it’s also crucial to get it down to the next price bracket on the property portals to open it up to a whole new market;’ he explains.

Putting an exact figure on what constitutes a meaningful reduction is tricky, says Paddy Pritchard-Gordon, of buying agency, Prime Purchase.

“Some properties are priced sensibly, others aren’t. Some may need to go down 20pc, others l0pc;’ he says. “However, you can’t go down 2pc or 3pc, it normally has to be 5pc to !Ope:’

Otherwise, Pritchard-Gordon explains, you end up reducing a bit, which doesn’t have any effect, and then reducing again.

“This makes you look desperate – it’s better to have one hard hit;’ he says. “The message you are putting out there by reducing the price is that you are listening to the market. It’s not a sign of desperation, you just want to sell:’

UK tax hikes are thinning out the ranks of super-wealthy homebuyers

By Damian Shepherd

When two Chinese investors bought a majority stake in a development dubbed “Mayfair’s most exclusive address” in 2015, London’s housing market was booming. Almost 10 years and an insolvency later, half the apartments have yet to be sold.

The travails of 60 Curzon are emblematic of what’s been a miserable period for the city’s prime property market, with prices down more than 20% from their peak. The downtrend is now being supercharged by the recent removal of a tax perk for so-called non-doms and an exodus of wealthy. For realtors, that’s further thinning out the rolodexes of deep-pocketed clients on whom the luxury market has long depended.

Quite simply, the market looks to be in a chronic decline, with no recovery in sight. Sellers are slashing prices, deals are taking longer — if they happen at all — and some luxury complexes are part empty. Just this month, Sotheby’s dropped the price of a Mayfair penthouse to £68 million ($91 million) from £85 million. It had originally been put on the market for about £100 million.

“London isn’t as sought after as it was a decade ago,” said Aneisha Beveridge, head of research at broker Hamptons.

Broker Savills Plc expects prices for prime central London properties to fall about 4% this year. At Black Brick Property Solutions in Mayfair, managing partner Camilla Dell predicts an even steeper drop and is picking up other signs of financial trouble.

“I can see the prime central London market ending up 8% to 10% lower by the end of this year,” she said. “I am starting to see an increase in receivership deals come across my desk.”

The latest numbers seem to support such pessimism. Deals for properties valued at £5 million or more have fallen about 15% in the past year, researcher LonRes said last week. The result is a growing glut of homes that aren’t selling, meaning it’s going to take even more severe price cuts to get buyers interested.

Price Cuts for £5 Million-Plus London Homes Are On the Rise

The damage was set in train by a slew of tax hikes targeting both luxury real estate and the city’s wealthy elite, and has been compounded by blows from Brexit to higher interest rates and sanctions on Russian money.

This year, the Labour government ended a long-standing tax regime that benefited rich non-domiciled residents. After that sparked a wave of departures, the Financial Times reported that the government is considering reversing a decision on inheritance tax.

The downward drift for high-end homes echoes the fortunes of London itself, particularly after the UK’s vote to leave the EU raised questions about the city’s place in the world and its desirability as a location for business and money.

Even if some of the most pessimistic Brexit predictions have proved off the mark, there are multiple examples of how much luxury property has been ground down in recent years, and how much harder it’s become to sell the priciest homes.

60 Curzon, which was later financed by funds managed by Apollo Global Management Inc., isn’t the only site with properties sitting empty. The Bryanston, a luxury residential tower overlooking Hyde Park, has only filled about half of its 54 units since they went on sale roughly four years ago.

“Long gone are the glory days,” said Paul Finch, head of new homes at broker Beauchamp Estates. “Margins have become extremely tight and the gap between commercial success or loss has become very narrow.”

Mega Mansion

In the first half of the 2010s, capital was flooding into London’s red-hot residential property as interest rates were slashed in the aftermath of the global financial crisis.

One moment capturing the boom was speculation in 2015 about the owner of ‘Witanhurst,’ the city’s largest private home, which newspapers estimated had a value of £300 million.

But just as readers were pouring over the details of the mega mansion and marveling at the torrent of wealth flowing into the UK capital, the market was quietly turning a corner.

London Luxury Property Isn’t As In Demand As It Once Was

First, then-Chancellor of the Exchequer George Osborne rewrote property tax rules in late 2014, effectively cutting bills for lower value properties but increasing them for top-tier homes. He followed that up with hikes on second properties.

Home values in prime central London are down almost 21% since 2014, according to Savills. Knight Frank’s sales index, a long-running gauge of the city’s top properties, peaked in August 2015. It’s down 19% since then.

London’s Property Market Has Lagged Behind Other UK Cities

A crackdown on money laundering and unexplained wealth, as well as sanctions on wealthy Russians have also thinned the ranks of overseas buyers that once dominated the top end of London’s property market.

One Russian billionaire caught up in the sanctions was Andrey Guryev, the founder of fertilizer giant PhosAgro. He’s also the owner of ‘Witanhurst’.

London’s slump reflects a broad global decline in high-end property prices. Earlier this year, Savills predicted that at least half a dozen major cities would see price drops in 2025.

“Global capital cannot move around the world as pain-free now,” said Ben Sanderson, managing director of real estate at Aviva Investors.

Prime London Homes Are Taking Longer to Sell

Quick deals are becoming rarer as buyers looks for price cuts.

In London, as the time to sell increases, deeper price reductions are on the cards.

A detached house in west London sold for £5.2 million in November, roughly 15% below its original asking price. The property was marketed at about £6 million for four months and received zero bids in that time, according to Jo Eccles, the buying agent involved in the deal.

In the same month, a double-fronted mews house in Knightsbridge — a stone’s throw from the luxury Harrods department store — had its asking price reduced to less than £13 million. As recently as 2023, it had been listed at £17 million, according to Knight Frank.

With the tax environment becoming more hostile, some wealthy arrivals have turned to rentals rather than committing to an expensive home purchase.

Charles McDowell, a broker whose decades-old London property firm has traditionally advised clients on buying multi-million pound homes, has broadened his services into lettings. He set up a unit last year following a surge in demand from London movers worried about potential policy changes under the soon-to-be-elected Labour government.

“Those people are looking to rent instead so they can get a full picture of the tax environment before putting down roots,” he said. “They’d rather take a ‘wait and see’ approach right now.”

We asked leading industry professionals to share the price and demand trends they have observed in the prime property market locations that are most popular with Investec clients.

Summary

Global political and economic uncertainty is said to have impacted demand in the prime London property market during Q1 2025. According to Savills, prices are relatively static, with a 2.6% fall in average prices recorded year-on-year. However, industry experts tell Investec that the picture is ‘incredibly nuanced’. Private banker Carlos Mendes explains: “The reduction in mortgage rates has been positive for our clients who want to preserve their personal liquidity. However, activity levels vary by property type and location, so it’s been more important than ever to understand local markets and provide tailored financial support.”

Here, property consultants describe the market dynamics in eight popular postcodes.

Hampstead (NW3)

Kim Blackman, Managing Director of Blackman Investments, says: “NW3 has always been attractive to affluent couples and families. It is an elegant, leafy suburb with Georgian houses, independent shops and cafés that is still so close to Central London. It’s also just five stops by tube to Kings Cross.

On average, house prices in Hampstead and Belsize Park have fallen by 9% over the past 12 months. However, properties with a good layout and outside space in the £1.5m – £5m range remain unaffected and demand for these homes is still strong.

My advice for buyers? Work with a trusted search agent who will not only listen to your criteria, but also deal with all the complex issues that invariably arise throughout the process and ensure your interests are protected. If you are selling your home, a property consultant can advise you on how to maximise the value of your asset. By making certain changes to your property, it can make a significant difference to the sales price achieved.”

St John’s Wood (NW8)

Jo Eccles, Founder and Managing Director of Eccord, says: “Family homes in St John’s Wood persistently outperform the market, with American buyers accounting for around 40% of our local clients.

St John’s Wood offers a greater range of architecture than other locations, with more lateral living space and some wonderful gardens on large plots. It is possible to achieve 5,000 square feet over three floors.

We’re seeing strong demand in the £10m – £15m price range from clients who are relocating for school places. Demand is also robust in the super-prime price range, and we recently acquired a £25m house in St John’s Wood for clients who wanted to be within walking distance of the American school.

In a higher interest rate environment, 80% of our clients were choosing to pay cash for a new home. However, recent rate cuts are encouraging. Certain professionals, such as private equity clients, are more inclined to borrow, to keep their personal liquidity available for other investments.

Buyers should be mindful that St John’s Wood is a very relationship-led market. More than half of the properties we acquire for clients in St John’s Wood are sold off market.”

Bayswater (W2)

Camilla Dell, Managing Director of Black Brick Property Solutions, says: “Bayswater appeals to a wide range of buyers, ranging from families to property investors. The area has seen a surge in buyer demand, driven by a £3bn regeneration of Queensway, which includes high-end apartment complexes, restaurant pavilions and landmark retail destinations that will be completed in 2026. W2 is also within striking distance of some of London’s best schools such as Wetherby, Chepstow House and Pembridge Hall.

My favourite part of W2 is The Hyde Park Estate, a small triangle area bordered by the Bayswater Road, Edgeware Road, and Sussex Gardens. The architecture consists of grand, white, stucco-fronted buildings that surround various garden squares and crescents. Residents are close to the park and Connaught Street for essential shopping.

The volume of transactions in W2 is up 14% year-on-year, and there has been a 9% increase in prices. In the last three months, houses achieved an average sales price of £6,082,667. Homes in good condition with period features and high ceilings are most sought-after, particularly in quieter streets.

That said, Bayswater hasn’t been immune from the slowdown caused by increases in stamp duty and the abolishment of the UK Resident Non-Dom rules. The average discount achieved between February and April 2025 was 9% *.”

Chelsea (SW3)

Jeremy McGivern, Founder of Mercury Homesearch, says: “We have observed a slight increase in buyer numbers in Chelsea in the last month, as interest rate cuts have increased confidence. Buyer demand is strongest for properties below £5m and buyers include parents looking to invest in property for their children, as well as individuals looking for a city pied-à-terre.

In most cases, it is properties that have recently been refurbished that are achieving premiums, while homes that have been refurbished more than six years ago are seen as being tired. We’ve seen that buyers are taking longer to make decisions too.

The golden rule is to remain patient and be selective. We sometimes find that sellers are not informed about what is happening to prices in their specific area. Consequently, you need to use specific negotiation techniques to achieve the lowest price possible. Relying on a price per square feet comparison rarely works, because logic is often not the deciding factor.”

Battersea (SW8)

Sarah Gerrett, Associate at Knight Frank in Battersea, says: “Battersea is a very green neighbourhood with an excellent selection of schools so it’s a great place for families. In addition, some professionals look to buy a pied-à-terre close to Battersea Power Station with its excellent amenities and transport links.

Our Battersea index shows that prices rose 0.6% between January and April this year. Given that we are moving out of a volatile period of political and tax changes, and mortgage rates are now starting to ease, we believe this could be the bottom of the market, so it makes sense for sellers to explore their options now.

For homeowners, it’s imperative that marketing material and the viewing experience is excellent given that buyers have a lot of choice and are used to seeing beautifully stylised properties on social media.”

Fulham (SW6)

Edward Peers, Heads of Sales at Hamptons in Parsons Green and Fulham, says: “Fulham attracts domestic buyers, as well as European buyers who are likely to live and work in London. For this reason, they are likely to move for lifestyle reasons and are less driven by economic events. Many of them tell us they are attracted to the local area because of the amount of green space and excellent schooling that it offers.

According to Land Registry data, in 2024 the average sales price for a home in Fulham was £1,186,510 and we have observed that prices have been relatively static in the first half of 2025.

There are currently around 60 houses that are on the open market for sale in Fulham above £3m. The greatest demand is for period terraced houses, with between four and six bedrooms, that are close to Parsons Green or Bishops Park.”

Notting Hill (W11)

Hannah Aykroyd, Managing Director at Aykroyd & Co., says:

“Notting Hill continues to be a firm favourite among our clients, drawn by its vibrant, ever-evolving character, iconic white, stucco architecture, and abundance of private communal gardens. This enduring appeal ensures the area remains one of the most sought-after in prime London.

Pricing across the Notting Hill market has softened by 7.6% compared to this time last year. However, transaction levels have risen by 16%, reflecting renewed activity and interest. Buyers are currently negotiating average discounts of 8.2% off initial asking prices.

The market for larger homes remains the most robust, with four-bedroom houses achieving an average of £2,536 per square foot. Demand is strongest for turnkey, exceptional family houses, which can command significantly higher premiums due to their rarity.

The recent change in interest rates has provided a degree of renewed confidence, particularly in the sub-£10m market, with notable momentum in the sub-£5m range. This has brought a wave of first-time buyers into the market, particularly for flats and smaller houses.”

Kensington (W8)

Pete Bevan, Co-head of prime central London at Savills, says: “In the last few months, our Kensington team has sold to buyers from North America, Asia Pacific, the Middle East and Europe, and several of their recent sales have been in conjunction with our new homes and international desks.

Meanwhile, activity across the family-house market has been largely driven by domestic buyers searching for a home in one of Kensington’s key addresses, who are taking a long-term view. These are people who are extremely familiar with the area and have always viewed Kensington as their preferred London location; they know the best streets, addresses and units within developments so when properties have come to market, they have chosen to make a move.

Interestingly, there has also been rising interest from people looking for pied-a-terre properties, and well-presented flats in portered buildings have sold well. We have seen some strong prices achieved for turnkey stock and in some cases, competition among buyers recognising the rarity of an asset coming to market.

Buyers are drawn to Kensington because it retains a community feel; it’s a discreet prime central London neighbourhood where people can access green space, fantastic schooling, shopping and dining. The lifestyle package coupled with the range of housing stock from period to newbuild has been a major factor in these deals taking place across all market segments.”

The property ladder is disappearing as young people save on stamp duty and moving costs by settling in their ‘for ever home’ much earlier

Marie Calligaris always thought her first property would be a flat, then she would gradually climb the property ladder. The trainee clinical scientist, 27, has just had an offer accepted on her first home with her partner, however, and it’s a four-bedroom house in Haslemere, Surrey.

Calligaris had been renting for several years in Brighton and her partner had been renting in London, where he works. Both had terrible landlords and endless problems. They decided it was time to buy, and moved in with her partner’s parents in Chichester, West Sussex, to save money. Haslemere was their target area because it’s a good halfway point for their commutes.

They considered buying a flat, but the threshold for first-time buyers paying stamp duty starts at £300,000 — at that price, they could have bought a one or two-bedroom flat in that area, but they hope to start a family in the next few years.

When her partner’s parents offered to help them financially, it was a no-brainer to look for a house. Otherwise they would have had to pay hefty stamp-duty charges each time they climbed the ladder. “A lot of the three-bedroom houses were in the same ballpark as the four-bedroom, and from a stamp duty point of view, there was no difference,” Calligaris says. “The four-bedroom house cost £575,000. We’re going to be paying just shy of £19,000 in stamp duty, and we would have had to pay the same for a smaller house.”

“The cost of moving is expensive,” she says. “You’re just shooting yourself in the foot if you need to move every two or three years because you have another child. We’d rather go straight for the house now and live in this property for ten years.”

The days of taking baby steps up the property ladder are disappearing, according to Camilla Dell, the founder of Black Brick, a buying agent. As property becomes less affordable, first-time buyers are getting older and saving longer by living with their parents or in flatshares. When they finally do buy — often with help from the Bank of Mum and Dad — they go big.

“In the old days, you might buy your studio, then sell it, then buy your one-bed, then sell, then a two or three-bed, then a family house,” Dell says. “That pattern, certainly in London, has vanished as a result of extortionately high stamp duty rates. People are moving less and trying to future-proof. First-time buyers want a house that will last them a good ten years.”

First-time buyers Jake Kelly and Emily Read have also gone straight for a house. Kelly, 30, spent seven years renting flats in east London and another year renting with Read in Hitchin, Hertfordshire. Kelly, an account executive for a tech firm, reckons he has spent about £67,000 in rent and thought it was time to stop throwing money down the drain. They’ve had an offer of £580,000 accepted for a three-bedroom semi in Guildford, Surrey.

They didn’t even consider buying a flat. “I’m sure for £580,000, you could secure a lovely flat in London, but then you’d have to go through the whole rigmarole of moving again if you get pregnant or get a dog,” Kelly says. “A lot of big life happenings are probably within the next five years, so it felt like a flat would be a short-sighted decision.”

Kelly finds moving stressful and isn’t keen to repeat the experience or the £19,000 in stamp duty they’re paying. Buying a house made financial sense. “My girlfriend and I complement each other quite well in terms of partnership — she inherited enough for a deposit and I have quite a good wage that allowed us to secure a good mortgage, so we make up for each other’s shortfalls.”

About 73 per cent of first-time buyers in Britain have bought a house in 2025, up from 62 per cent in 2020, according to Hamptons estate agents. In London, 50 per cent have bought a house, compared with 37 per cent in 2020. “Stamp duty is a big factor, with first-time buyers increasingly opting to buy larger homes to avoid having to move again in a few years when they won’t be eligible for a stamp duty exemption or discount,” says Aneisha Beveridge, the head of research at Hamptons.

First-time buyers pay no stamp duty below £300,000 and 5 per cent between £300,000 and £500,000. Above £500,000 they lose any first-time buyer discount.

Beveridge says the average age of a first-time buyer has risen to its highest level of 33.1, according to data from UK Finance, an industry body.

“We’re seeing a clear shift: more first-time buyers are skipping starter properties and going straight for family homes,” says James Evans, the chief executive of Douglas & Gordon, a London estate agency. “The fact that the average first-time buyer in London is in their mid-30s — more likely to be thinking about children and needing extra space — it’s no wonder we’re seeing people take the leap straight into their ‘forever home’.”

The disappearing rungs of the ladder are having wider effects on the property market, according to Dell. “There will be a potential oversupply of studio, one-bedroom and two-bedroom flats as they become less popular. And increasing demand for your three to four-bed terraced houses, starter homes in outer prime London areas.”

Dell says there is healthy competition for £1 million houses in outer prime London family neighbourhoods such as Fulham, West Hampstead, Clapham and Balham.

By contrast, demand for flats is dwindling. The problems with cladding post-Grenfell have undoubtedly cooled demand for flats. Matt Turner, the director of Rash & Rash estate agents in Southgate, north London, also says the profile of first-time buyers is changing in his patch. “They’re no longer buying £400,000 apartments. They’re now spending £750,000 and buying houses.”

Turner recently sold a two-bedroom flat he owned in the area for £410,000. “In 2016, we had it under offer at £430,000. I’ve sold it for £20,000 less nine years later. If I’d sold it then and bought a house for £500,000, that would probably be worth £700,000 now. Houses are really sought after, apartments are not.”

In London, the average price of a flat has grown only 2 per cent in five years, compared with 12 per cent for a terraced house, according to Hamptons. In Britain, the average price of a flat has increased 16 per cent in five years; a terraced house is up 31 per cent.

Buying as an investment was on the mind of Diogo Rodrigues and his partner, Laura Anderson, when they bought their first home: a three-bedroom house for £529,950 in Chesterford Meadows, a village development just outside Saffron Walden, Essex.

Rodrigues, a business development manager for a pharmaceutical company, and Laura, a PE teacher, lived at home with their parents until they were 26, saving money, then rented together for a year as a trial.

When it came time to buy, a house was the obvious answer. “One reason was that we wanted to maximise our return on investment,” Rodrigues says. “I’ve had older colleagues who bought flats as their first property, and had difficulty selling them and making a decent profit when they eventually outgrew it.

“Also, in five to ten years’ time, if Laura and I decide to have children or want to have pets, a house just made more sense.”

As befits an increasingly polarised society, the straight-to-house trend is a case of the haves and have-nots. Among Rodrigues and Anderson’s group of friends, the only ones who can afford to buy are couples with dual incomes — the single people are still renting or living with parents. It’s the couples who are leapfrogging up the ladder to their forever homes, often helped by parents.

Dell is concerned that fewer rungs means fewer moves, which doesn’t make for a healthy market. “Overall, volumes are massively down since George Osborne started messing around with stamp duty. That’s why it’s such a terrible tax. The housing market contributes a significant amount to the GDP. And yet the stamp duty stops the market from being fluid, as it causes people to stay in the same place longer than they should.” (Dell concedes another reason more people moved up the ladder in the early 2000s was because it was easier to get a mortgage).

Calligaris, for her part, is happy to be putting down roots. “We’re very fortunate to be able to live at home, to put money aside, and have parental help for the deposit. I realise a lot of people, like my siblings, are not in that position.

“I always thought we’d start with a flat, or a one or two-bed house and work our way up. But now that we’re in this position, I’m very thankful we’re doing it this way. I like knowing we’ll be there for the long term.”

Americans are flocking to the ‘Hamptons of England’, where the cost of buying a charming countryside property is 40 percent cheaper than purchasing stateside.

Nestled within a range of rolling hills which rise from the lush meadows of the upper River Thames to the cliffs beside the Severn Valley, the Cotswolds is a picturesque holiday destination located a scenic 90-minute train ride from London.

‘It’s terribly beautiful. The scenery is glorious,’ said local store owner and Boston native Jesse D’Ambrosi, who moved to the area five years ago.

Home to 91,000 people, the Cotswolds, which straddles six southern English counties and is governed from Gloucestershire, comprises the largest swathe of protected natural beauty in the United Kingdom.

Punctuated by quirky local businesses and honey-colored limestone cottages, its stunning green pastures have long presented an attractive escape from the capital for those wealthy enough to afford a second home.

In recent years, it’s also seen a boom in popularity from American expats, who bring a host of new demands to the area while embracing quintessential English country life.

Cotswolds Council leader Joe Harris said Yankees are now ‘all over’ the area. ‘We have an American member on our council,’ he told the Daily Mail. ‘Most people in our area know an American or have an American neighbor.’

This is reflected in the footfall at D’Ambrosi’s Fine Foods store, which sells classic American snacks it’s hard to find anywhere else in the UK.

The colorful eatery attracts a hefty 50 customers each day on average, despite being located in the market town of Stow-on-the-Wold, which sits atop an 800-foot hill.

‘As a joke I would get in some American products and put them in the window. I was shocked at how much of that product I moved,’ D’Ambrosi told the Daily Mail.

The store offers luxury Thanksgiving and Fourth of July hampers, as well as classic American snacks like bright orange Goldfish crackers and crimson jars of Lawry’s Seasoned Salt.

D’Ambrosi enjoys life in a cozy cottage with her seven-year-old daughter Rose, after previously living in Amsterdam, Paris and New York City, with her now ex-husband.

The local entrepreneur said the easy commute to London from the British country escape makes it comparable to the ritzy Long Island beaches which are a stone’s throw from Manhattan.

‘The Cotswolds is the Hamptons of England – without the sea of course,’ D’Ambrosi told the Daily Mail. ‘It’s also comparable to going upstate, though it’s a bit more rural and bucolic.’

Private members clubs have proliferated in the Cotswolds in recent years, reflecting this influx of a new kind of wealth akin to the Hamptons elite – as opposed to the traditional agricultural landowning families who have lived in the area for centuries.

English real estate experts Camilla Dell and Harry Gladwin told the Daily Mail that Americans have increasingly been looking to the UK for home purchases over the past half-decade.

‘Americans are a significant buying force for UK property,’ said Dell, the founder of Black Brick property consulting firm, where 25 percent of clients are from the US, bringing an average budget of $1million to $10million for a second home.

Dell, who herself has a holiday home in the Cotswolds, said Americans started flocking to the UK in greater numbers ‘five to six years ago’, when the dollar was comparatively strong against the pound in the aftermath of Brexit.

‘We started to see a significant uptick in American inquiries at that point,’ Dell said.

‘Since 2014, the London real estate market hasn’t really gone anywhere,’ she added.

Dell said the combination of this property market plateau, relatively higher wages in the US, and the dollar strengthening against the pound means Americans purchase homes ‘at almost a 40 percent discount’ compared with in 2014.

She added that the UK government’s abolition of non-domiciled tax status is also a draw for wealthy Americans.

Gladwin, who runs the Cotswolds division of property consulting firm The Buying Solution, said affluent American expats coming to the UK are honing in on his region in particular.

‘We’ve definitely seen a noticeable rise in interest from American buyers in the Cotswolds over the past few years,’ he said.

‘Americans are drawn by the area’s natural beauty, historic charm and strong sense of community, often built around wonderful village pubs – it’s a perfect slice of English country life.

‘Many are looking for a second home or a lifestyle shift and the appeal of achingly beautiful Cotswold stone houses, privacy and space continues to resonate strongly.’

‘When Americans think of the quintessential British countryside, the Cotswolds comes to mind,’ Dell agreed.

She said Americans love the chocolate-box cottages built with local Jurassic limestone which make every village look like a scene from The Holiday.

Dell said popular destinations include the ‘golden triangle’ of villages which are most easily accessible from London – comprising D’Ambrosi’s hometown of Stow-on-the-Wold, along with Chipping Norton and Burford.

Maryland native Sarah Kirk, 43, is among the American expat community who relocated to the ‘golden triangle’, partly because her husband is from the area.

The homemaker, who has four children aged between two and nine, shares a glimpse of her fairytale life in the Cotswolds each day with her 31,000 Instagram followers.

She said she loves ‘the slower pace of life, emphasis on seasonal living, beautiful landscapes to explore, and conservative small-town values’.

Kirk spoke with the Daily Mail over the phone from her sprawling backyard – or back garden in British – as birds could be heard chirping in the background.

‘It’s just a really beautiful part of the country where people go to look for that country living feel,’ she said.

‘My children have a lot of free rein here, a lot of places to wander. It’s a slow childhood,’ said Kirk, who previously lived in rural Virginia and South Carolina, as well as New York City and Washington DC.

‘There’s space here, not only physically but mentally, for a lot of peace. We are sheltered from some of the bigger issues that you might have in city life.’

Kirk said she has noticed the boom in private members clubs, usually frequented by Londoners she refers to as ‘the white trainers (sneakers) crowd’, who come up to the Cotswolds for a weekend retreat, which has given pockets of the area a ‘Hamptons-like’ feel.

Relatively new Cotswolds clubs include The Lakes by Yoo spa which is partnered with British supermodel Kate Moss, and Estelle Manor in Eynsham Park.

The quintessentially English Aynhoe Park was recently bought up by American furnishings company Restoration Hardware (RH), and it now sells the US-made fittings.

Dell said RH hosted an opening party at the stately home in 2023, which drew in a star-studded crowd featuring the likes of Sydney Sweeney, Zoe Saldaña, Regé-Jean Page, Ellen DeGeneres, Portia de Rossi, and supermodel Jourdan Dunn.

Local councilor Sandra Smith, who moved to the beauty spot in 1987 from Seattle, Washington, said that despite the celebrity buzz surrounding both the Hamptons and the Cotswolds, the latter is much more inclusive.

‘The Hamptons is all set up for really rich people with rich people things. It’s not like that here at all,’ the 59-year-old told the Daily Mail.

‘It can be upper class if you want it to be, but you can do it cheaply as well.’

‘There’s a big arts culture out here. It’s a little bit bohemian.’

Smith, who lives in the ‘Cotswolds capital’ of Cirencester, said she only planned on moving to the area for two years back in the eighties, but she fell in love with the ‘tiny houses and cars’ and ‘sense of community’.

‘I just really like living in Britain,’ she said. ‘The American middle-class lifestyle is a big house and a big car – but it’s a bit soulless.

‘You spend a lot of time driving around to shopping malls in the US and everything is so far apart. I love how you can do anything on foot around here.

‘Plus, my friends from America are always talking about gun crimes and shootings. Nothing like that happens here. It’s wonderfully boring and stable.’

Smith asked the Daily Mail to use a pseudonym to protect her identity due to concerns about traveling as a naturalized Brit under Donald Trump’s administration.

She said she gave up her American citizenship decades ago in exchange for a British passport.

Black Brick founder Dell added that ‘political reasons’ have ‘certainly’ been driving American buyers to the Cotswolds more recently as people are keen to escape Trump’s hardline policies on issues like immigration, and college arts and sciences funding.

Liberal Democrat council leader Harris agreed that ‘many’ recent expats he has spoken with ‘are trying to get away from the political reality in America’.

‘We like having our American cousins here, they are very welcome,’ he added. ‘There’s a strong community here.’

The Daily Mail revealed in March that the number of Americans seeking UK citizenship had reached record levels since Trump was elected for a second term.

More than 6,100 US citizens applied last year, an all-time high after figures began two decades ago and 26 per cent more than in 2023.

US clicks on British job listings were also up 2.4 percentage points year on year to 8.5 percent, the sharpest increase from any country, according to job search site Indeed.

Immigration lawyers have said Trump’s presidential bid and victory in early November helped spur the increase in American movers, with others adding the US political landscape was ‘a very serious driver’.

This was epitomized by Ellen DeGeneres, when she stormed out of Hollywood following the presidential election in November and embraced a fresh start in a £15million ($20million) Cotswolds farmhouse.

The 67-year-old former talk show host moved across the pond with her celebrity wife Portia De Rossi, 52, but it wasn’t plain sailing. Their new home was surrounded by floodwater, prompting them to move to a new mansion around the corner.

Gladwin said celebrities are commonly drawn to the area because it ‘offers a discreet haven for high-profile individuals’.

‘With its low-key villages, excellent pubs and growing number of exclusive private members’ clubs like Soho Farmhouse, Estelle Manor and The Club by Bamford, it’s become a fashionable escape for celebrities and creatives,’ he told the Daily Mail.

‘They appreciate the balance of luxury and informality, all within reach of London and with great connections to the US.’

Ron Burkle is one of the ordinarily low-profile American real estate magnates who is eyeing the Cotswolds for his next project, called the Serpentine Lodge.

However, he spoke with the Daily Mail after he came up against unprecedented opposition from locals who railed against what they called his plans to construct a ‘McMansion’ amid their cozy cottage cul-de-sac.

Burkle said he wanted to work with local people to make sure everyone was happy with his scheme – though it might take a lot of negotiation.

The area is also home to former British Prime Minister David Cameron, or Lord Cameron of Chipping Norton, David and Victoria Beckham, X-Factor judge Simon Cowell and the Bamfords.

Though celebrities and high-flying businessmen occasionally threaten the natural harmony of the area, Smith, who works in town planning, added that the Cotswolds’ unique charm stems from its status as a protected area of natural beauty since 1966.

She said it’s the most perfectly-preserved pocket of traditional English countryside.

‘Much of the Cotswolds is a conservation area, which means developers can’t change much,’ she told the Daily Mail.

‘This is how it retains its character – it’s always going to be this way.’

The £400m blossoming of Bloomsbury Hovering on the edge of prime central London, the bohemian enclave’s quiet charm and proximity to Soho and Covent Garden, is being reinvigorated by local campaigns and new investment. The brutalist Brunswick Centre, built in the 1970s, is being improved by a £24mn Lazari investment.

For the wave of Americans looking to buy in central London, those who can prise their eyes from the obvious charms of high-profile enclaves are finding a rich seam in overlooked areas that are dusting themselves down. Jacqueline Griffin and her husband, a commercial executive in higher education, moved to London last year. Originally from Colorado, they were initially “drawn to the greenery of Holland Park, and the canals around Maida Vale,” says Griffin. They struck upon the less vaunted streets of Bloomsbury serendipitously.

“We ended up walking through the area and instantly loved its Georgian architecture, and the calmness, even though it is so close to Soho and Covent Garden.” Since November the couple, who have two grown-up daughters, have rented a three-bedroom apartment on Bloomsbury Square — first laid out in the early 1660s and the one-time home of novelist Gertrude Stein and, later, architect Edwin Lutyens. “We love the bohemian and socially diverse feel,” says Griffin. “I garden with the Friends of Bloomsbury Square and have found a great sense of community.”

For buyers, Bloomsbury is a relative steal compared with its more illustrious neighbours. Last year, the average price of property sold in the area was £1,137 per square foot. Not only was this lower than 10 years ago (average prices topped £1,200 between 2015 and 2017, according to LonRes, which tracks the prime London market), it remains significantly less than the prime central London average of £1,654 per sq ft, and lower than both nearby Fitzrovia (£1,480) and Marylebone (£1,581).

“You don’t really buy in Bloomsbury for capital growth,” says Tom Kain, a partner at buying agent Black Brick Property Solutions. “You buy in Bloomsbury because it’s good value for central London.” South of King’s Cross, north of theatreland and next door to Fitzrovia, Bloomsbury has long been London’s intellectual quarter. It is dominated by the British Museum, UCL and the iconic art deco Senate House, but is also home to Soas, Birkbeck and myriad medical and publishing companies. It’s where the Russell Group of universities was formed (in Russell Square), and is still associated with the creatively progressive “Bloomsbury set” of artists and writers of the early 20th century — including Virginia Woolf, EM Forster and Vanessa Bell — who, as the American Dorothy Parker wrote, “lived in squares, painted in circles and loved in triangles”. But after being heavily bombed during the Blitz, then blighted by postwar development, Bloomsbury has not been the fashionable neighbourhood it once was.

“Some parts are studenty or touristy,” says Edward Towers of buying agent Aykroyd & Co, “but buyers love its period charm and the fact they can walk to the theatre.” A four-bedroom, fifth-floor apartment with period features on sale for £2.25mn through Chestertons A one-bedroom ground-floor apartment, £600,000 through Chestertons What they won’t find, however, are glitzy new branded apartment schemes and chichi private members’ clubs — as a result, Bloomsbury has hovered on the edge of “prime central London” in both perception and pricing. But with a local reinvention campaign under way, could this be about to change?

Bedford Estates, the district’s largest private landowner, is working alongside Imperial London Hotels, Kimpton Fitzroy London (the 1905 hotel whose dining room was replicated in The Titanic), Lazari Investments and the Central District Alliance (CDA) to reinvigorate Bloomsbury with a £400mn investment. Its plan includes both improvements to public spaces, such as the woodland planting, seating and pedestrian-friendly new layout of Princes Circus, and a slew of new hotels, including chic, boutique brands that have honed their reputations elsewhere in the capital with place-making destination bars and restaurants. The brutalist Imperial Hotel is being redeveloped; a new Zetter hotel will open in October across six Georgian town houses; and Firmdale (the brand behind The Soho and Charlotte Street Hotels) has reportedly acquired a long leasehold interest in three adjacent buildings behind Bedford Place. The historic and partially pedestrianised Lamb’s Conduit Street is full of chic independent shops.

The opening of the Elizabeth Line at Tottenham Court Road has already been a game-changer, says Alexander Jan, chair of the CDA. “The area is coming of age as a more sophisticated business district too. Office vacancy rates have fallen.” He points to newly built offices for more than 3,000 GSK staff on New Oxford Street, and McKinsey & Co on Museum Street.

In a Grade II-listed building in Bloomsbury Square, a state-of-the-art life sciences lab is being built, while Lazari has invested £24mn improving the Brunswick Centre, the shopping centre completed in 1972 that also incorporates 600 architecturally striking flats. It’s telling that wholefood brand Farmer J’s has joined Waitrose and Gail’s there, while Store Street has been smartened up and is styling itself as something of a micro-Marylebone High Street. “Residents are spending more time in the area now — they don’t have to trip across to Mayfair to go out for dinner,” says Simon Elmer, steward of Bedford Estates. “With this and festivals and events like Picnic in the Park, we are slowly lifting the profile of Bloomsbury.” Russell Square gave its name to the prestigious Russell Group of universities; Senate House is in the background.

Pianist Jonathan Papp, the artistic director and co-founder of Georg Solti Accademia in Italy and senior operatic and vocal coach at the Royal Academy of Music, has mixed feelings about the area changing too much. He moved to Bloomsbury in 2022, buying a two-bedroom penthouse overlooking the British Museum to renovate. “I can walk everywhere, including to work at the Royal Academy and Royal Opera House.” Like the Griffins, he soon gave up his car. “It feels like a place where people really live rather than just pass through — there’s a mix of young people, lawyers, musicians and students,” says Papp, 60, remarking on the queues to the Fortitude Bakehouse behind Russell Square station since it began trending on TikTok. I can walk everywhere, including to work at the Royal Academy and Royal Opera House. It feels like a place where people really live rather than just pass through Pianist Jonathan Papp One perennial hotspot, however, is Lamb’s Conduit Street, the part-pedestrianised thoroughfare lined with upmarket independent shops, the odd — small and chic — chain (Aesop, Honey & Co, La Fromagerie), and restaurants such as local institution Noble Rot. When an elegant one-bedroom flat above a shop there was recently offered for sale at £675,000 by Greater London Property, it swiftly attracted eight bids and is currently under offer for over the asking price. Interest was driven, says agent Rob Hill, by “rarity value. Many properties on this street are owned by Rugby School and don’t come up for sale.” More broadly, one-bedroom flats in the neighbourhood’s mansion blocks are priced at around £450,000-£500,000. Though Towers has just shown one in Bedford Court Mansions to an American client looking to buy in the area. The Bloomsbury Group united early 20th-century writers and intellectuals such as Virginia Woolf and Vanessa Bell.

Adrian Philpott, associate director at Winkworth, recently sold a three-bedroom flat in the classic red-brick mansion block of Ridgmount Gardens to a Lebanese couple; they bought it for their daughter, who is at the French school. Greater London Property is selling a two-bedroom flat in the smart block with on-site porterage for £700,000 (it needs an update). “We have parents who buy flats for their children at UCL, Birkbeck or Soas, then maybe let them out,” says Philpott. According to the 2021 census, only 16.6 per cent of households in the Bloomsbury-St Giles-Holborn area are occupied by three or more people, and 96.9 per cent of residents live in flats.

Family houses are thin on the ground. Kain was recently charged with finding a Georgian four- to six-bedroom town house in the area for a couple in TV production; ultimately, although they loved the area, they couldn’t find the right house, and bought in Marylebone instead — despite it costing 25 per cent more. “Such houses cost £1,500 per sq ft in Bloomsbury but £2,000 in Marylebone,” he says. For Jerome Salle, Bloomsbury has proved a rewarding base to raise his two daughters. The Frenchman and his Japanese wife relocated to London from New York for their jobs in finance and have rented a three-bedroom flat in the area since 2015. “We moved here to be close to the then-new French school, École Jeannine Manuel,” he says. “We had our doubts at first — about it being so commercial, with not so many residents — but have grown to love the area’s convenience. I travel regularly to Paris and can walk to the Eurostar station.” They also frequent Coram’s Fields — a historic seven-acre family-only park in the heart of Bloomsbury opened in 1936, which is packed with children and teens on a sunny midweek afternoon.

“The area has long been overlooked but it’s possible to find some great properties,” says Oliver Sanhaji at Middleton Advisors, who has just located a house for a couple of young lawyers who wanted to be able to walk to their offices. Currently, one of the 4,000 sq ft Georgian town houses on the popular tree-lined John Street, on the Holborn borders, is for sale at £6.5mn with Sotheby’s International Realty. The rarity of these homes makes them difficult to price, says Philpott. “A five-storey Regency town house on the market last year at £5mn sold for closer to £4mn.”

Recommended UK prime property Can Bayswater level up with the rest of prime central London? In some ways, Bloomsbury makes its own rules and is difficult to predict, like the literary characters who made its name. Despite the sizeable drop in price of the Regency town house, overall in the past year Bloomsbury did not see the decrease in the average price per sq ft felt by both Fitzrovia (-11 per cent) and Marylebone (-3.6 per cent). Those with a similarly offbeat outlook might well find their niche here.

A record 104,794 home sellers slashed their prices last month. Could the Bank of England’s base rate cut today signal future falls in mortgage rates and offer a lifeline?

By David Byers

The spring housing market is traditionally a hive of activity, with homes flanked by gardens of tulips and daffodils flying off estate agents’ shelves like hot cakes.

However, this spring has been a season of two drastically contrasting halves. After a frenetic start in March, when buyers set new records for deals done and mortgages taken out, it all went very quiet in April and sellers have been left pleading for attention since.

In early spring, before the cheaper rate of stamp duty expired on March 31, there was a flurry of activity, as buyers — particularly first-timers — desperately rushed to complete their purchases, trimming an average of £6,000 off their tax bills in London and the southeast.

As a result of this stampede, the number of house sales rose to a record of 177,370 in March, up from 109,700 in February — and more than double the 86,810 total recorded in March 2024 — according to HMRC. There was a surge in mortgage borrowing, up from £3.3 billion in February to £13 billion in March, while stamp duty receipts for a gleeful Treasury in the first quarter of this year were £2.595 billion — the third quarter in a row when they were above £2.5 billion.

After this rush, as the calendar ticked over to April Fool’s Day, the dust settled — and, for many sellers, it has been tumbleweeds all the way since as they struggle to find buyers for their homes.

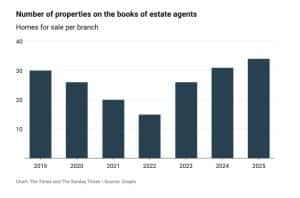

The property portal Zoopla reports that there were 15 per cent more homes for sale in April compared with the same time last year, but only 1 per cent more buyers. The average estate agency, meanwhile, has 34 homes sitting on the market — the highest number in any April since 2019.

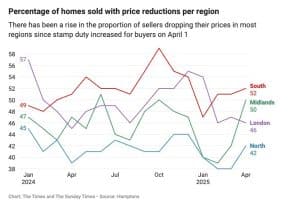

As a result of this buyer desert, many sellers are taking urgent action. Data given to The Times by TwentyCi, the analytics company, shows a record 104,794 sellers reduced the price of their properties last month, which is higher than all prior Aprils going back to 2019.

At the height of the Covid boom, when buyers were flocking to the market amid the April 2021 stamp duty holiday, only half as many — 51,376 — needed to cut their prices because there were so many more buyers around.

All of which means that this spring there will be a simple mantra for many sellers, particularly in more affluent areas, where prices (and therefore stamp duty) are higher: cut your prices or have your home languish. As Simon Gerrard, chairman of Martyn Gerrard Estate Agents, says: “The stamp duty changes have had an immediately chilling effect on the market.”

And yet it isn’t all bad news. With today’s cut in the Bank of England base rate of interest from 4.5 to 4.25 per cent, mortgage rate cuts look likely to accelerate across high street lenders in the coming weeks, potentially luring buyers back to the market and providing some desperately needed attention for those neglected sellers.

Here’s what you need to know about the strangest spring market in recent years.

The spring where only certain areas are in bloom

As March ticked into April and stamp duty rose, data provided toThe Times shows the huge extent to which the UK’s housing market cooled almost overnight. PropCast, a data platform that produces weather forecast-style heat maps for every area of the UK, shows the number of “hot” markets — where more than 35 per cent of properties listed for sale are under offer — shrank from 1,730 in March to 1,678 in the space of a month.

However, the regional variations are greater than ever. On the one hand, some areas in the southeast, southwest, east and London — where buyers are most affected by rising stamp duty and where international residents worried about higher taxes are selling up — are getting much chillier. For example, the SW10 postcode (covering West Brompton and part of Chelsea) has a paltry 11 per cent of advertised properties under offer, and Marylebone, Mayfair and Fitzrovia (W1), which has been particularly badly hit by foreign owners selling up, records only 9 per cent.

Camilla Dell, of Black Brick, a buying agent that sources properties at the most expensive end of the market for wealthy buyers, says the impact of Labour’s tax rises — and in particular the end of the non-dom scheme — is hobbling the priciest parts of London: “Buyers of prime London property are nervous about buying into a market with excessively high stamp duty rates and an exodus of wealthy people leaving our shores for more favourable tax jurisdictions.”

Areas in coastal resorts and beauty spots are also getting chillier, as rising taxes and running costs price out second-home buyers and holiday let investors. In TR8 (Mawgan Porth, Cornwall) only 25 per cent of advertised properties were under offer in April. In Windermere (LA23) it was 23 per cent.

By contrast, property markets in northern areas — where large numbers of homes remain beneath the stamp duty threshold (of £250,000 for home-movers and £425,000 for first-time buyers in England) and are popular with investors and first-timers — are still booming. For example CA1 (Carlisle) and SK3 (Stockport) both have 73 per cent of homes on the market under offer.

Reflecting this extraordinary divide, Edward Hartshorne, managing director of Blenkin & Co, an agency in York, says: “March and April saw some of the best trading months in our 33-year history.”

Selling a property in a cold area? Here’s what to do

“Many sellers have just not grasped that we are in a very challenging market, and have not adapted accordingly,” Marc Schneiderman, director of Arlington Residential, says.

Jamie Hope, managing director of Maskells, agrees: “This is a price-critical environment. We recently agreed to the sale of a good house that, at the initial asking price, saw no offers. The price was reduced and, within two weeks, three buyers competed and the house is now under offer close to the original asking price.”

There is early evidence that sellers in most areas are indeed dropping their prices meaningfully, according to Hamptons, the estate agency. It found that across Britain, nearly half (48 per cent) of homes sold in April were reduced in price, up from 45 per cent in January, February and March this year. This ranges from 52 per cent of sellers reducing prices in the south to 42 in the north.

However, the average number of homes on agents’ books is still the highest in recent years, at 34 properties per agent, according to Zoopla, which suggests more price cuts are needed.

Ultimately, sellers need to familiarise themselves with the picture in their area and act accordingly.

Light at the end of the tunnel — as mortgages become cheaper and easier to get

In the short term Gerrard believes the sluggishness in parts of the market will continue. “It’s likely that these [stamp duty] changes will act as a persistent brake on transactions,” he says. Indeed, data released last week by Nationwide showed national prices down 0.6 per cent month on month, reflecting that trend, although Halifax recorded a modest 0.3 per cent rise in figures out on Thursday.

Yet the evidence is that in areas hit the hardest by rising taxes there might be the prospect of a brighter summer ahead as borrowing becomes cheaper. The Bank of England cut interest rates today in the first of what is likely to be a series of back-to-back rate cuts that could result in them falling by as much as one percentage point over the next six months, City analysts believe.

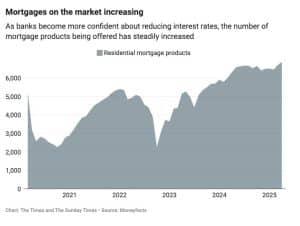

This will particularly help buyers in pricier southern areas, who are struggling to afford the loans needed to meet more expensive house prices. The number of mortgage products being offered by lenders has steadily gone up in recent weeks as rates have reduced. And lenders are being asked by the financial regulator to be more generous on affordability calculations to allow more people to borrow.

Look around, buyers: there are new-build deals to be had

However, if you’re a buyer and fear your stamp duty bill will price you out, rest assured there are people even more desperate than you — new-build developers.

Builders are suffering a double whammy, with high taxes putting off prospective buyers who were, in many cases, already deterred by the end of the Help to Buy scheme, which until 2023 used to provide loans of up to 40 per cent to first-time buyers to buy new-builds.

Now, many developers are desperately trying to compensate with lucrative incentives to cancel out tax rises. Peabody New Homes, for example, will provide up to £11,250 to buyers at its developments including Higgs Yard at Loughborough Junction, southeast London, where properties start at a pricey-looking £424,000 for a one-bedroom flat.

Another developer, Backhouse, is offering an incentive of £10,000 to buyers purchasing in their Cotswolds developments at Blunsdon, Highworth and Moreton-in-Marsh.