30th November 2020

17mins

So long, farewell…2020!

As we approach the end of 2020 – a true ‘annus horribilis’ if ever there was one – there is still some time to reflect on the ups and downs of this year, and to look ahead to better times in 2021 as Covid vaccines are hopefully rolled out across the globe. This newsletter outlines our ‘highlights’ of 2020; our major property market themes for 2021; and our best transactions of 2020.

We also contributed to the FT’s ‘Business of Luxury Summit’ panel this month, along with the Capital Rise Podcast, where you can hear Camilla Dell’s thoughts on the current market and the outlook for next year, too (links below).

FT Business of Luxury: To watch a recording of the session, please register here first: https://luxuryglobal.live.ft.com/page/1558499/vip-registration?promo=SPGUEST

Then go to: Agenda (ft.com) and click on the 12:40 session from Tuesday 24th November “The Future of London’s Property Market”.

Capital Rise: https://www.capitalrise.com/blog/prime-property-with-uma-rajah-episode-six/

‘Highlights’ of 2020

It may seem somewhat strange to point to ‘highlights’ of 2020 given the completely unprecedented and disruptive nature of events this year, but it has certainly been an extraordinary and often unexpected rollercoaster for the property market.

The cocktail of the pandemic, intermittent lockdowns and powerful fiscal stimulus have created bifurcated pricing trends by property type and region. Transactions have surged ahead of the March 2021 stamp duty deadline, driven by domestic buyers, putting strains on the creaking architecture of the UK property market.

Black Brick started the year with a view that Prime Central London price expectations were too conservative in some areas and noted a build-up of pent-up demand. In Q4 2019, we registered twice as many applicants compared with the same period last year. The average budget per applicant had also risen, from £4 million to £6.35 million.

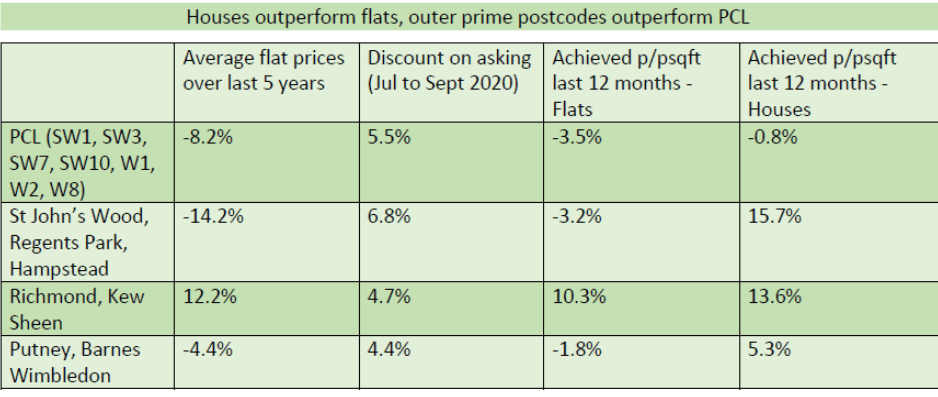

Table source data: LonRes

While the ‘Boris Bounce’ was quickly superseded by the dictates of the emergency response to the pandemic, a cocktail of plunging interest rates, a surge in Bank of England QE asset purchases, still-weak sterling and a stamp duty holiday created a very active market in 2020.

“This year, the market surprised by its resilience in extraordinary times. Buyers have had to navigate pandemic lockdowns, travel restrictions and the timing of fiscal incentives,” says Camilla Dell, Black Brick Managing Partner.

Underneath the bonnet, price trends have reflected the behavioural impact of the pandemic – more working from home and the need to secure more outside space. As a result, houses have outperformed flats in price terms, while price growth in outer London postcodes has far outstripped traditional Prime Central London. Domestic buyers led the way post lockdown and continue to be the dominant force, particularly in the £5m-£10m bracket.

Q1 2021: expect the unexpected

With good news on vaccine progress and an end in sight to tough lockdown conditions later in 2021, will we see a reversal of these trends? Or has Covid wrought persistent behavioural changes to the way we live and work?

Black Brick’s Camilla Dell and Caspar Harvard-Walls expect a bumpy outlook in Q1, with the expiry of the SDLT zero rating up to £500,000, the introduction of a 2% foreign buyers’ surcharge, speculation over changes to Capital Gains Tax in the Spring Budget and adjustment to life outside the EU.

Next year’s price trends are difficult to predict, with the only consensus in the market being that Prime Central London prices will grow over the next 5 year by around 17-18%. Black Brick sees Prime Central London golden postcodes continuing to offer the best buying opportunities while Covid-19 persists and travel restrictions remain in place. New build in secondary areas is likely to continue to be challenged.

Notes Camilla Dell, “Some reversal of the houses vs flats trend is to be expected in the wake of a vaccine and hoped-for return to ‘normality’ after Easter. At Black Brick, we have long argued that demand for central London properties would recover from the Covid shock and that central London living would retain its appeal. Meanwhile, the ‘new normal’ with some continuation of working from home trends should preserve demand for London suburban family houses.”

On Capital Gains Tax speculation, Camilla’s view is that, should it happen, “we wouldn’t expect it to be a massive revenue generator as it will simply encourage owners of properties to hold onto them until retirement, when their incomes will be lower.” Similarly, any extension of the SDLT holiday might be beneficial to the national market as a whole, but it is merely a ‘nice to have’ when it comes to the buying decision in Prime Central London.

With the return of foreign buyers likely to coincide with the new SDLT 2% surcharge for overseas purchases, we would not expect a significant downward impact on the market, although new developments specifically aimed at foreign buyers will likely see the tax absorbed into pricing – for example, Canary Wharf and Battersea Power Station.

Themes for 2021 – a greener year, in more ways than one

Turning to longer-term trends, we see four themes for 2021 and beyond: the ‘greening’ of the real estate sector; the 15-minute city; the ongoing search for outside space; and currency volatility.

The ‘greening’ of the real estate sector

Beyond Covid, climate change is already perceived as the next global threat to health and economies, with an increased willingness to spend money on preparation and mitigation already evident. With Biden in the White House and European countries already making ambitious plans in this direction, greening the economy is being rolled up in the need to ‘build back better’ following the pandemic.

The real estate sector has a huge role to play in this, with the construction and operation of buildings responsible for 40% of global carbon emissions. This should lead to a focus on sustainable buildings and reducing carbon footprints for the industry. JLL have pledged to achieve net zero carbon emissions by 2030 – they are the first agency to sign up to the World Green Building Council Net Zero Carbon Building Commitment. They also recently created a global head of sustainability services and ESG. We expect other agents to follow.

Buyers will become more sensitive to whether a building is “green” – building materials, carbon footprint, energy efficiency rating (a factor which is already important for landlords). Developers will need to look at how they can incorporate this growing trend into their schemes and ‘super-prime’ developments are likely to be marketed on this basis. “Being green will overtake being swanky,” according to Camilla Dell, Black Brick Managing Partner.

The 15-minute city

The likely continuation of working from home and the shift to online shopping points to the need for a more unique high street experience, close to home rather than the office. This dovetails with the rising trend of the ’15-minute city’ which Black Brick expects to rise to further prominence in 2021 – and will help London to become greener, too.

On 15-minute cities, Mark Sutcliffe of smarttransport.org writes : ‘Instead of sucking workers, shoppers and students into congested city centres, the 15-minute approach devolves the provision of day-to-day needs to a neighbourhood, so nobody needs to travel more than 15 minutes to earn a living, buy food, see a doctor and educate their children.”

Under lockdown, huge swatches of Central London streets have become more pedestrianised, such as Regent Street. And buyers are already seeking out leafier suburbs with character high streets. High streets outside Central London will be an important driver of the post-lockdown economic recovery, too, with 41% of all London businesses located on high streets and their immediate surrounds, and 28% of all jobs in the capital.

St John’s Wood is an obvious example of a 15-minute city within London, providing one reason why house prices have risen so drastically this year. White City is moving in this direction, with the new Television Centre development, while Richmond, Dulwich, Hampstead and Chiswick are all good examples, too.

Communal Gardens and Garden Communities

The behavioural legacies of Covid are not just going to encourage buyers to look for houses with outside space, but also properties with access to those hidden gems of Prime Central London – the communal garden square. Camilla Dell of Black Brick notes: “We’ve talked a lot about how buyers have wanted to buy houses with gardens. Another real winner from Covid has to be houses that back onto communal gardens. They offer so much and are less crowded and busy than local parks. Communal gardens offer the perfect combination of private outside space, community and low upkeep. I think these streets are somewhat bullet proof and will always hold value regardless of wider economic events.” Good examples include Lansdowne Road and Ladbroke Square in Notting Hill, Eaton Square in Belgravia, and Onslow Square in South Kensington.

The greenback: a reversal of fortunes?

Brexit has had a profound impact on the sterling exchange rate since 2016 but that may come to an end as the UK fully leaves the EU at the end of 2020. Sterling has already seen some modest upward pressure against the dollar in late 2020 and this may be set to continue.

With Brexit in the rear-view mirror, sterling appreciation against the dollar may become a more important consideration. According to Camilla Dell: “Our clients are not particularly concerned over or talking about Brexit, assuming it is already baked into London property prices. But the trajectory of the currency is relevant – weak sterling has been a nice tailwind for dollar-based buyers since 2016, with the effective discount amounting to as much as 40% at times, and this could reverse somewhat in 2021.”

However, a couple of factors could prevent too sharp a depreciation of the dollar and avoid scaring off those all-important foreign buyers. Although US fiscal expansion and continued QE may put downward pressure on the dollar, international demand for the currency and dollar assets remains strong, not least as the US economy is already enjoying a robust recovery from the Covid pandemic.

On the other side of the trade, the UK is still in fiscal expansion mode and more monetary stimulus is on the cards – including, potentially, a move towards negative interest rates in the UK. The Bank of England has asked the banking sector to prepare for the possible introduction of negative interest rates and has the tool up its sleeve should economic conditions worsen.

These factors – strong global dollar demand, US economic outperformance and market expectations of lower UK interest rates – may help to slow sterling appreciation in 2021, but the direction of travel is still likely to be up.

A year in transactions

Despite the many challenges of 2020, the Black Brick team acquired £59,077,000 of property with 19% off market and, on average, we saved our clients 7.1%. Below, we detail our best house purchase, best apartment, best off-market deal, best managed sale and best investment of 2020.

Best House: South Hill Park Gardens

Our client wanted to purchase a family home in either Primrose Hill, Hampstead or Swiss Cottage with a maximum budget of £5,000,000. With fierce competition for family homes in prime residential neighbourhoods, ensuring early access to possible options was going to be crucial.

The search started in mid-February when the residential sales market was seeing a rebound as a result of the Conservative election victory and more certainty over Brexit. Whilst a number of possible options were identified vendors were, in general, being very bullish about their asking prices which continued as we entered the lockdown period.

We remained in close contact with our network and were made aware of a beautiful, double fronted house which was due to come to market on South Hill Park Gardens – a beautiful street in Hampstead close to the Heath, shops and walking distance into the village. The house was 3000 square foot, with an asking price of £4,950,000 or £1650 per square foot and had been painstakingly refurbished by the current owners who were planning to move out of London. The house was perfect for our client and unsurprisingly there were a number of other interested parties. As a result, we paid the asking price and were able to take the house off the market to prevent any further viewings taking place or offers being solicited.

Best Apartment: Sloane Terrace Mansions

Our Swiss client was looking for a London apartment for personal use. With children at school in the UK, they wanted a family apartment to use when visiting the city. Our client was not in a rush to buy and needed advice on the market, timing their transaction, and access to the best opportunities in their favoured areas of Chelsea, Knightsbridge & Belgravia.

We sourced a grand and spacious second floor lateral apartment situated in a quiet position, but only a few steps from Sloane Square. The building consists of only 12 large apartments and the flat itself comes with a share of freehold, a rarity for the area. The property was listed through a single-office boutique estate agent we have transacted with in the past. As a result, we were the first to be made aware of it.

We negotiated strongly, taking advantage of the current lack of overseas buyers in London and achieved an impressive 12% discount (or £500,000) from the asking price for a rare asset. We made sure our client had all the necessary comparable sales data and advice, in order for them to make an informed decision prior to submitting the offer. Beyond the negotiation, we also introduced our clients to tried and tested third parties such as a specialist structural surveyor and design & build contractor.

Best Off market Deal: Clarges

Our US client wanted to purchase an apartment in Mayfair on an ‘off-plan’ basis, with a minimum of three years between exchange and completion, as well as a staged payment schedule, to allow him the time to fund the transaction. Clarges is widely regarded as one of the best boutique buildings in London with only 34 units, as well as meeting the client’s requirements for 24-hour concierge and first-class leisure facilities. The issue was that the development has been completed, precluding payment over an extended period.

Nevertheless, we structured an unusual offer to the owner, namely that our client would rent the property via a series of one-year tenancies, up to a maximum of three years. We would agree the ultimate purchase price at the outset, and our client would pay the owner each year for an option to purchase the property, at that price, at any point during those three years. If our client walked away after the rental period, he would lose the option payments; otherwise, these payments would be deducted from the final purchase price. While the negotiations were far from straightforward, we eventually agreed terms, namely that the purchase price was fixed at £10.5m to be paid within the three years.

However, the impact of Covid-19 meant that our client wanted to extend the timeframe of the deal, given the degree of economic uncertainty ahead. We went back to the seller to renegotiate to extend the term of the transaction to five years. After another extensive period of negotiation, we were able to agree revised terms. This both meant that we were able to keep the transaction together during a very testing time, while ultimately securing the best possible outcome for our client.

Best Managed Sale: Abingdon Road

Our international client had purchased a house in Kensington for family use more than 10 years ago but it was no longer required. He was keen to sell despite the fact the sales market was extremely challenging given the uncertainties over the Brexit outcome. The property had been vacant for some time and there were a long list of outstanding maintenance issues which needed to be rectified.

With our many years of experience we knew it was crucial that the house was presented in its best possible state before any viewings from potential purchasers were allowed to commence. We worked through the maintenance issues and also recommended that our client use the services of a professional staging company who then furnished the entire house with stunning furniture and art. Once this first stage had been completed we then made our network of fellow buying agents aware that the property was available off market.

We received an acceptable offer from only the second viewing at the house with a completion date set for April 2020. Unfortunately this was during the coronavirus crisis but we were able to ensure that completion happened without any delay.

Best Investment Deal: Long and Waterson

Our long-term investment client was looking to invest a total of £20 million into the London property market for a combination of rental yield and long-term capital appreciation. Our advice was to split the budget across multiple properties in order to give diversification to the portfolio and to purchase in bulk – 6 units or more in one single transaction to qualify for commercial rates of stamp duty. The properties had to meet a strict set of investment criteria – high quality new build, easy to let out or pre-let and able to achieve a gross yield of at least 4% or higher.

We identified a boutique, high quality new build located in Shoreditch, consisting of just 119 units. Long and Waterson is the first and only to date premium new development in the immediate vicinity (1/2 mile radius). Fringe City locations have benefited hugely in recent years from the broad increase in urban living in London, from the rise in popularity of East London and also from the growing importance of technology, digital and start-up businesses. The development is superbly located, a 2-minute walk from Hoxton station and 15 minutes from Liverpool Street station, benefitting from a 24-hour concierge, private gym, saunas and treatment room, extensive private gardens, a screening room and residents’ lounge.

We negotiated the purchase of 6 apartments in January 2020 for a combined purchase price of £4,750,000 achieving almost a 16% discount from the original asking price and an estimated average net return on equity of 6.6% over a projected 5-year hold period. However, right before we were due to exchange contracts, Covid-19 struck and the world changed. London went into lockdown and we sensibly decided to put the transaction on hold.

Over the course of the following weeks and months we carefully monitored market conditions and as we approached the end of lockdown and the property industry was able to return to work, we successfully re-negotiated the purchase down to £4,075,000. We de-risked the purchase by removing one of the more expensive 3-bedroom units and replacing it with a one-bedroom unit. We also managed to increase the overall discount to 20% from the original asking prices and we negotiated a one-year rental guarantee for our client to take into account the higher risk rental environment due to the pandemic. At just over £1000 per square ft. this will be a very good long-term investment for our client, in an exciting new growth area of London.

We would be delighted to hear from you to discuss your own property requirements. For a non-obligatory consultation, please contact us.