3rd November 2020

14mins

Race Against the Machine?

With a surge in property market transactions and increasingly cautious lenders slowing down the UK housing-buying process, buyers need to be savvier than ever in approaching this market. Using a knowledgeable buying agent can help to smooth the conveyancing process, avoid unwanted surprises and help to secure quality long-term investments, especially when dealing with idiosyncratic off-market transactions.

In this newsletter, we examine the pitfalls and opportunities of buying an ‘off-market’ property, note the challenges in predicting trends in the microcosms of Prime Central London, interrogate the savings on offer for those navigating a busy market to beat the stamp duty deadline, and highlight our acquisitions of the month.

Although England re-enters a comprehensive coronavirus lockdown on Thursday 5th November for an initial duration of four weeks, the property market will remain open this time around. While buyers are encouraged to do as much property research as possible online, viewings can take place and surveyors and valuers can conduct inspections as normal. Construction sites will also remain open. As Housing Secretary Robert Jenrick confirmed on Twitter: “…the housing market will remain open throughout this period. Everyone should continue to play their part in reducing the spread of the virus by following the current guidance.”

Unravelling the ‘off-market’ myth

Under normal market conditions, buyers might wonder how best to assess fair value when purchasing off-market. But under today’s conditions of heightened uncertainty, the challenge is even greater. How can buyers ensure they are not overpaying when a property has not been ‘tested’ on the open market?

Black Brick has substantial experience in sourcing off-market properties and seeing the transactions through to completion. In 2019, 38% of Black Brick transactions were off-market, with no down-valuations. In 2020 so far, 20% of our transactions have been away from the open market.

“There is a perception that buying off-market is special or better, but that is not always the case,” says Camilla Dell, Managing Partner at Black Brick. “In fact, lender caution and general market uncertainty may well be unravelling the idea that ‘off-market is better’. This approach can work really well if a buyer is seeking a specific street close to their children’s school, for example, but buyers need to make sure they are fully informed about the local market and realistic pricing for the property.”

Black Brick will carry out thorough due diligence on any off-market property, including the pros and cons of the property and pricing analysis. As Caspar Harvard-Walls, Partner at Black Brick, adds: “We are able to give buyers advice about whether a price is reasonable, using recent buying data to make an informed decision. Off-market buyers are often under pressure to bid before a property goes onto the open market and can benefit from an independent analytical view to make sure they are not paying a risky premium.”

The help of a buying agent can come into its own when purchasing an off-market property – not just to source the property, but to ensure the correct level of due diligence is carried out to protect the buyer’s interest and to satisfy mortgage underwriting standards.

With cautious lenders increasingly lowering LTVs and widening loan spreads, and reports of ‘down-valuing’ by surveyors proliferating, it is more important than ever that buyers are certain they have secured the right property at the right price. Not only will this help to ensure the investment value of the property for the long-term, but it can help to avoid any nasty surprises during the conveyancing process and reduce the risk of a purchase falling through – an even more costly event than usual in today’s market, with the stamp duty deadline looming into view (more on which below).

Predicting the unpredictable?

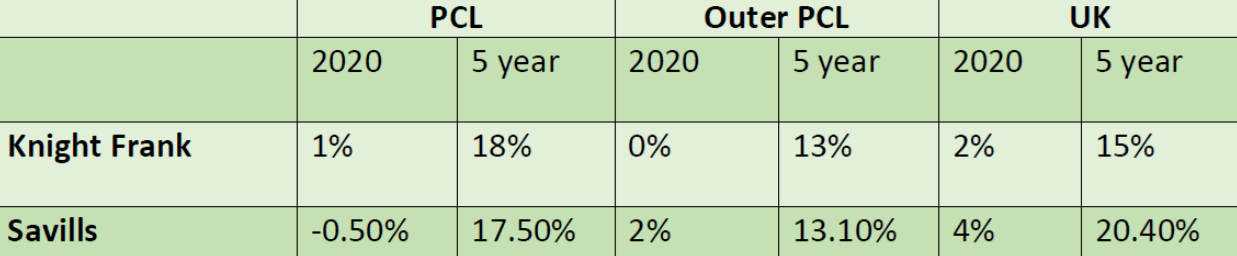

Major forecasters are racing to refine their property market predictions as an unprecedented year for the property market draws to a close and the longer-term outlook remains clouded with uncertainty. Knight Frank and Savills remain at odds as to whether Prime Central London (PCL) will be a small ‘up’ or ‘down’ year, but expectations are for around 18% capital value growth over the next five years.

The aggregate PCL picture hides significant divergences by property type and area. As Camilla Dell notes: “Predicting capital values by zone is difficult. Arguably, property type is more important – for example, flats versus properties with outside space. Forecasts should almost be drilled down by postcode and property type in this market, pricing trends are so granular. The Black Brick view is that it is incredibly difficult to predict London price trends as a whole at the moment. There is certainly a flurry of activity in the market for family houses with gardens in areas such as Richmond, Sheen and Hampstead Garden Suburb. Some of the froth will inevitably calm down as the March 31st stamp duty deadline approaches, but these sorts of properties are always in demand. While appetite for flats remains muted, we would be wary of writing off Prime Central London, not least given easy liquidity conditions and the incentive for foreign buyers to get in ahead of the introduction of a 2% surcharge on 1st April next year.”

Clogged market plumbing and a race to the finish line

The last days of October have seen a flurry of press and industry reports focussing on how clogged the plumbing of the housing market is becoming at a time of surging activity. It is times such as now when professional help and an organised approach to conveyancing can make all the difference in not only securing a desired property but also benefitting from current stamp duty incentives.

Zoopla’s Annabel Dixon writes that ‘the sales pipeline is now 50% bigger than it was this time last year. We estimate there are 418,000 homes sales progressing to completion – 140,000 more than usual at this time of year – worth a whopping £112bn’. Meanwhile, the Telegraph’s Isabelle Fraser notes lengthening times to receive mortgage approvals and book in surveys: “Legal & General Mortgage Club estimates that the average sale now takes 15 weeks from start to finish…The time it takes to get a mortgage offer has grown from a fortnight to about four to six weeks, according to broker Private Finance… Other delays are the result of a postcode lottery, as some local councils have huge backlogs to do simple searches that are necessary for deals to go through. Andrew Boast, of SAM Conveyancing, said local authority searches that would normally take one to three weeks now often take six weeks.”

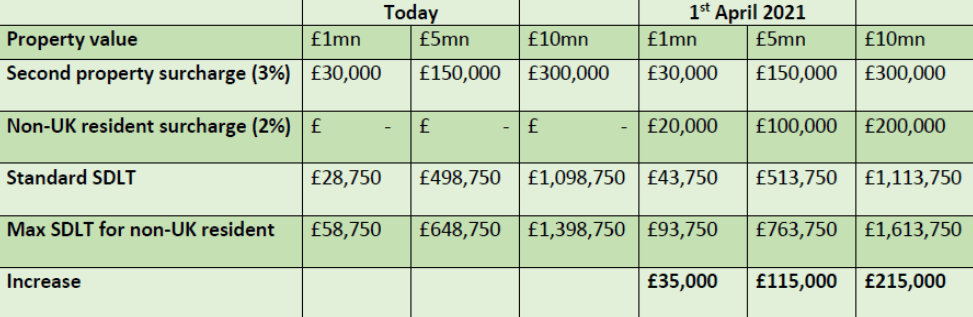

With two stamp duty deadlines looming at the end of March 2021 – the expiry of the 0% rating below £500,000 and the introduction of a non-UK resident 2% surcharge – navigating the idiosyncrasies of the UK house purchase process smoothly is more important than usual. According to Zoopla, under normal circumstances, 97% of sales agreed in October complete by March, but this figure drops to 81% in December, 54% in January and only 17% in February.

The table below shows the maximum amount of stamp duty that could need to be paid on a property, if it is a second home and the buyer is non-UK resident, and the comparison between today and the charges on 1st April. By purchasing before the stamp duty deadline, a buyer could save a maximum of £35,000 on a £1mn property, £115,000 on a £5mn property and £215,000 on a £10mn property.

Perhaps unsurprisingly, therefore, Savills have reported that the upper end of the Prime Central London market has rallied ahead of the SDLT changes: “Transactions of homes with a £5 million+ price tag were 12 per cent higher in the first three quarters of 2020 than in the same period in 2019, as this market segment recorded its strongest third quarter for five years.” But a real surge in market activity depends on travel restrictions easing and the return of foreign buyers.

According to Black Brick Managing Partner Camilla Dell: “The new surcharge which comes into effect on April 1st only affects non-resident buyers. If they can’t travel here, we are unlikely to see the “spike” in activity. However, we are seeing some buyers start to get themselves organised. We recently signed a US client who has every intention of getting his transaction done before April 1st next year. We would advise any overseas buyers to start now – December is only a 2-week month given the holiday season, leaving just 20 working weeks until the change comes in.”

After the tax change comes in, the overall effects on market pricing could be limited: “We predict price softening will be greater in developments targeted towards overseas buyers – areas such as Canary Wharf and Battersea Power Station could easily see a 2% drop. I wouldn’t be surprised to see some developers even offering to pay the levy for a certain time period. However, buyer beware – often developer incentives are factored into prices. We don’t see the surcharge having much impact on prime domestic markets such as Hampstead, St John’s Wood, Primrose Hill, Fulham, Wandsworth, Wimbledon, Richmond, Barnes and Dulwich, which are driven by mainly domestic buyers.”

Indeed, as Black Brick’s Caspar Harvard-Walls highlights: ‘In general, clients are comfortable with absorbing a one-off charge in the low single-digits that can be capitalised into the cost of running a property over many years, or swamped by foreign exchange movements. What they are more concerned about, and would like to avoid, is an annual mansion tax.’

Against the backdrop of an increasingly busy market and a ticking tax countdown, Camilla shares her recommendations to ensure a smooth conveyancing process.

Acquisition of the month 1: Ebury Square, Belgravia, SW1 – £3,322,000

With an active market and acute differentiation by property type and postcode, is there still such a thing as a ‘covid discount’ and where can buyers find it? Our two acquisitions of the month highlight the divergences in the market for flats and family houses, but show that it is still possible to find good value opportunities in even the most in-demand areas.

Our first acquisition, in Ebury Square, highlights the significant price reductions available on flats in SW1 and the ways in which we successfully navigated lockdowns and travel restrictions in this case.

We were engaged by an overseas client who was looking to purchase a two-bedroom apartment in either Belgravia or Knightsbridge as an investment. It was critical that the apartment be in good condition and benefit from air conditioning, a lift and a porter. Air conditioning is increasingly becoming a high priority for many of our clients given the summers are getting warmer, and severely limit the options available. Most apartments that have air conditioning tend to be new build, and can command up to £5,000/sq. ft in prime Central London, so finding a suitable option was going to be no easy task given we had a budget of £3,500,000.

We identified a two-bedroom apartment in 1 Ebury Square, a well-serviced modern development in Belgravia, which matched all the criteria given to us. However, when it was first launched to the market at £4,250,000 we knew it was going to be beyond our client’s budget. We monitored the property over several months, as its asking price was reduced to £3,950,000 and then finally to £3,700,000 just before lockdown. We began negotiations during lockdown and were able to agree the purchase at £378,000 (over 10%) below the asking price. We also agreed the deal “subject to viewing” allowing our client time to fly to London, isolate for 14 days and view the property prior to exchanging contracts.

Acquisition of the month 2: York Avenue, Sheen, SW14 – £3,150,000

Meanwhile, in York Avenue, Sheen, we were engaged by our British Clients to find a larger London property with more lateral space and closer to Richmond Park to walk their two dogs. Their budget was up to a maximum of £3,500,000. The market for large family houses in close proximity to parks has always been competitive but the Covid pandemic has only increased the demand for this type of property.

The search started in February when the sales market was seeing a significant rebound as a result of the Conservative Party win in the General Election and more certainty over Brexit. We identified a number of interesting options but the lockdown in March meant that the search went on hold and resumed in September – when the market was perhaps even more competitive than it had been earlier in the year.

We identified a house in Sheen which had been recently refurbished and offered not only exceptional lateral space but also was located less than a 10-minute walk from a gate into Richmond Park. The house was 3700 square foot with an asking price of £3,300,000, equivalent to £891 per square foot. We were able to agree a price of £3,150,000 (£851 per square foot). Crucially, the terms of our offer specified that no further viewings were to take place and that our clients were to be given a period of exclusivity so that they could undertake their due diligence without the threat of another buyer coming forward.

Our years of experience means that even in competitive markets we are able to ensure that, when the right property is found, our clients have the time to transact without the pressure of having other buyers compete with them.

Coutts webinar: ‘What’s next for the UK property market?’

Managing Partner Camilla Dell was delighted to have been asked to take part in a real estate webinar for Coutts Private Bank recently. The webinar was hosted by Dennis Howard, Executive Director, Middle East and Asia and moderator Katherine O’Shea, Coutts Real Estate Investment Service. Dell was joined on the panel by other heavy weight buying agents discussing what’s next for the UK property market.

For those that weren’t able to tune in, here is the link to the recording: https://vimeo.com/473394007

Password: Foundation

We would be delighted to hear from you to discuss your own property requirements. For a non-obligatory consultation, please contact us.